AI data center regulation is being rewritten simultaneously in every US power market. This is a field report from a year inside the filings — seven Independent System Operators, three federal agencies, and a dozen state utility commissions — all converging on the same five-element framework for AI data center regulation, on overlapping 12-to-24-month curves. AI data center regulation is the through-line of this entire report, and it is the lens through which every number, every tariff, every filing, and every architectural choice below should be read. Visit the Savrn AI Infrastructure homepage for more from the field.

Why AI data center regulation matters now

For most of the last decade, AI data center regulation was treated as an afterthought — a matter of zoning, of tax incentives, of utility-customer onboarding. That posture is over. AI data center regulation in 2026 is the central variable in whether a project gets built, how it gets financed, what it costs to operate. And whether it survives the next two grid-disturbance events. The rules now determine the interconnection queue. They drive cost allocation. They codify the ride-through standard. Curtailment posture is dictated by the same framework. Whether co-located generation is a competitive advantage or an outright regulatory necessity now sits inside this framework as well.

The entire architecture of the AI build-out — from the rack-level power supply to the campus-scale capital stack — is being reorganized around AI data center regulation as it is being written.

Notably, what follows is the evidence: the federal layer of AI data center regulation, the ISO-by-ISO map, the state-level cost-allocation grid, the hardware compliance gap that AI data center regulation has opened in the OCP standard. And the architectural answer that AI data center regulation now demands. Each of the seven Independent System Operators discussed below is moving on its own AI data center regulation timeline. Each of the dozen state utility commissions has its own AI data center regulation vehicle. The convergence — and the window — is real.

Prologue — A meeting nobody is covering

On a Tuesday morning in February, somewhere on the third floor of a federal office building in Washington, a small group of grid engineers sat around a conference table and tried to define a word.

The word was load.

For most of the twentieth century, that word had a settled meaning. A load was a thing that consumed electricity — a furnace, a motor, a refrigerator, an aluminum smelter. Loads behaved predictably. They drew current; they responded sluggishly to disturbances; when the voltage dropped, they limped along or fell over and a fuse popped and the lights came back on a few minutes later. Engineers built grids around the assumption that loads were dumb, slow. And forgiving.

The thing the engineers were trying to define was a new kind of load. A campus drawing as much electricity as a small city. Power supplies switching at tens of kilohertz. Inverters and rectifiers and DC buses doing things to the alternating current that no industrial customer had ever done at this scale. A “load” that. When the grid voltage sagged for a fraction of a second, would not limp — it would trip, simultaneously, across hundreds of megawatts. And cascade the disturbance back into the system as a fault of the grid’s own making.

In practice, the North American Electric Reliability Corporation has a phrase for this new thing. It is computational load. On March 18, 2026, NERC’s Standards Committee accepted a Standards Authorization Request to write the first Reliability Standard explicitly for it. The SAR document is fifty-three pages long. It refers, repeatedly, to a problem the engineers cannot solve from the grid side and that the data center industry has not yet acknowledged from its side. The problem is that the loads are bigger and faster than anything the rules were written for. And the rules were not written.

That meeting in February — and a hundred others like it across the United States in the past eighteen months — is the closest thing to a national grid policy debate the country has had since the restructuring fights of the 1990s. It is happening in seven independent system operators, fourteen state utility commissions, three federal agencies. And the standards committees of one continental reliability council. It is happening in parallel, on overlapping twelve-to-twenty-four-month deadlines, with very little coordination between the rooms and very little press coverage outside of the trade titles.

And it is happening fast enough that most of the AI infrastructure under construction in the United States today will be obsolete, by code, before it is finished.

By contrast, this is the story of how that happened, what the rules actually say. And what — for builders, financiers, advisors, regulators. And the people who get the electric bill at the end of the month — comes next.

Part I — The Demand Wall Driving AI Data Center Regulation

The trigger is not subtle. The trigger is a column of numbers that any utility planner can read.

Begin in Texas. ERCOT, the grid that covers about 90 percent of Texas load, runs a public interconnection queue. As of the December 9, 2025 board update, that queue contains more than 233 gigawatts of large-load interconnection requests, with more than 70 percent coming from data centers — most of them speculative, many of them duplicate filings by the same developers hedging across multiple sites. The all-time system peak ERCOT has ever served is 85,931 MW, set on August 20, 2024 — call it 86 GW. The queue is nearly three times the entire grid.

Of course, most of the queue will never get built. ERCOT staff know it. The developers know it. The hyperscaler tenants know it. But the modeling has to be done; the studies have to be funded; the queue itself has become a strategic asset that gets sold and traded as new arrivals try to skip the line. The cost to ERCOT and to ratepayers of processing the queue, even setting aside whatever actually gets energized, is enormous and growing.

Now move east, into PJM

Now move east, into PJM Interconnection. PJM is the largest power market in the United States, covering roughly 67 million people across thirteen states and the District of Columbia. Its 2026/2027 capacity auction cleared at the FERC-approved cap of $329.17/MW-day across the entire footprint — a record at the time of clearing (since exceeded by the 2027/28 BRA). According to the Independent Market Monitor’s analysis, the inclusion of forecast data center load in the peak load forecast produced an increase of $7,271,197,971, or 82.1 percent, in capacity market revenues (Monitoring Analytics, Analysis of the 2026/2027 RPM Base Residual Auction, Part A, October 1, 2025). Eight out of every ten dollars of capacity-cost increase across the largest power market in America came from one customer class. That number is not in dispute. It is in the IMM’s published analysis.

Now move west California, where

Now move west to California. Here CAISO is studying 4.5 gigawatts of data center demand in its current transmission planning cycle. The California Energy Commission forecasts another 1.8 GW by 2030 and 4.9 GW by 2040. CAISO is the slowest-growing demand market on this list — California has actively discouraged data center siting for years — and even there, the curve is vertical.

Crucially, now move to the Tennessee Valley Authority. Here data centers already represent 18 percent of industrial load and are projected to double by 2030. On February 11, 2026, TVA’s board voted to add 150 MW to xAI’s Memphis allowance — roughly doubling its contracted capacity. The same TVA decision cycle reversed previously planned closures of the Kingston (scheduled 2027) and Cumberland (scheduled 2028) coal plants, citing data center demand growth — a decision treated by the political opposition as a scandal and by TVA’s planners as basic arithmetic.

Now move to Duke Energy’s territory

Now move to Duke Energy’s territory in the Carolinas. Here the data center pipeline is 6 gigawatts. Duke is in the middle of two general rate cases — Duke Energy Progress filed in October 2025, Duke Energy Carolinas in January 2026 — and a Clean Transition Tariff is under evaluation that would let large customers connect to the grid while developing their own clean energy supply.

Now move to Arizona. Here Salt River Project alone serves 59 large-load customers totaling roughly 7 gigawatts of combined capacity. And Arizona Public Service has large-customer load commitments approaching 13.1 GW — against an actual 2025 system peak of approximately 8.6 GW (with APS’s own forecasts placing system peak near 11.4 GW by 2031 and 13 GW by 2038). The Arizona Corporation Commission held a Large Load Workshop on April 16, 2026, to formalize state-level rules.

Meanwhile, now move Virginia, largest

Meanwhile, now move to Virginia, the largest concentration of data centers in the world. Here the State Corporation Commission approved a new rate class — GS-5 — on November 25, 2025, with effect in 2027.

Now move to NYISO. Here 48 large-load proposals totaling roughly 12 GW had landed in the queue by December 31, 2025, up from six projects in 2022.

Now stop look what you

Now stop and look at what you have. Every regulator in the United States looked at numbers like these — different jurisdictions, different totals, identical curves — and arrived at the same conclusion at roughly the same time. The reliability margins their predecessors built into the system were calibrated for a world that no longer exists. The political math of telling residential ratepayers that their bills are going up to subsidize Amazon’s compute was politically intolerable in every state at once. This 24-month engineering horizon to build new generation, new transmission. And new substations was incompatible with the 18-month build cycles that hyperscalers were demanding.

As a result, the wall hit at the same time everywhere because the wall was the same wall.

What followed was the regulatory wave that this article documents.

Part II — The Federal Layer of AI Data Center Regulation

The federal response began earlier than the public realized and moved faster than anyone in the industry expected.

On October 23, 2025, the Secretary of Energy, Chris Wright, invoked a relatively obscure provision — Section 403 of the Department of Energy Organization Act — to direct the Federal Energy Regulatory Commission to initiate a rulemaking on standardized large-load interconnection. FERC opened the corresponding rulemaking docket, RM26-4-000, on October 28, 2025. The directive was accompanied by a fourteen-point set of principles. They were unusually concrete for a federal directive. New loads should pay for the network upgrades they cause. Co-located “hybrid” loads — generation and load behind a common point of interconnection — should be permitted to file joint interconnection requests. Study times should be reduced. Grid upgrade costs should be reduced. The framing was bipartisan-coded; the substance was technocratic.

Section 403 invocation not without

The Section 403 invocation was not without controversy. Under the Federal Power Act, the states have historically held jurisdiction over retail load interconnections, regardless of size. FERC has held jurisdiction over generation interconnection and interstate transmission service. The DOE proposal, by asserting federal authority over large-load interconnections that touch interstate transmission — which, given the size of the loads at issue, is essentially all of them — was a quiet bid for federal preemption of an area that the states had thought they owned.

The National Association of Regulatory Utility

The National Association of Regulatory Utility Commissioners filed concerns. The commissioners did not love the federal incursion. They also did not have time to fight it the way they would have a decade earlier. The state commissions are themselves drowning in large-load filings. Many of them privately welcomed federal minimum standards because it relieved them of the political risk of writing those standards themselves.

Most importantly, fERC committed to act on the Section 403 proposal by the end of June 2026.

That is the most important date in American grid policy this year. By the end of June, FERC will issue an order that either (a) sets nationwide minimum technical and procedural standards for large-load interconnection, leaving cost allocation to the states; (b) declines to preempt state authority and limits its action to clarifying jurisdiction over co-located generation; or (c) some hybrid in between. The most likely outcome — the outcome the docket signals at this writing — is the hybrid. FERC sets the floor on ride-through, telemetry, curtailment capability. And study procedure; the states keep cost allocation; the co-location framework becomes federalized.

If FERC rules that way, the five-element framework that this article will return to repeatedly becomes federal law. Every project under development at that point becomes either compliant, noncompliant, or in the process of being redesigned.

FERC: the December 2025 order to PJM

Of course, fERC has not waited for June to begin acting. On December 18, 2025, in Docket EL25-49-000, the Commission found PJM’s existing tariff “unjust and unreasonable” and ordered PJM to implement transparent rules to accommodate large loads co-located with generation resources. The order was narrow on its face — it asserted FERC jurisdiction over (a) interconnection of generating facilities to interstate transmission, and (b) provision of transmission service used to serve co-located load — but its practical effect was sweeping. PJM had spent two years dragging its feet on whether co-located gen+load arrangements should pay full transmission charges or should be treated as behind-the-meter and thus exempt. FERC’s December order foreclosed the foot-dragging. PJM responded by accelerating the relevant work-streams in its Critical Issue Fast Path process. This I will return to in the ISO section.

FERC has also continued to advance

FERC has also continued to advance Order 2222. This requires regional transmission operators to allow distributed energy resources, including aggregated controllable loads, to participate in wholesale markets. This is not directly about data centers. But it is parallel pressure in the same direction. Loads that can be controlled — by aggregation or by direct dispatch — are increasingly treated as resources, not just as customers.

The Department of Energy has not waited either. On January 17, 2026, during Winter Storm Fern, DOE issued 202(c) emergency orders directing PJM, Duke Energy. And ERCOT to keep diesel generators ready and to dispatch them as needed. The orders were defensible on their face — the storm caused real reliability stress — but they were also a signal. The signal was that the federal government now expects large industrial loads with on-site generation to be dispatchable. And that the regulatory posture of treating those generators as opt-in or opt-out is over. If you have generation on site, in the federal view, you are part of the reliability solution.

NERC: the technical side

Above all, nERC, the continental reliability authority, has moved on the technical side. In February 2026, NERC convened a Large Load technical conference. The conference concluded — and the Reliability and Security Technical Committee subsequently approved — an Accelerated Large Load Action Plan. On March 12, 2026, the RSTC approved the second whitepaper from the Large Loads Working Group, titled “Assessment of Gaps in Existing Practices, Requirements. And Reliability Standards for Emerging Large Loads.” The whitepaper is technical, dense. And unequivocal. The existing FAC-002-4 standard for facility interconnection studies. This has been in force for years, is inadequate to address the dynamic behavior of large computational loads.

A week later, on March 18, the NERC Standards Committee accepted the SAR for a new Reliability Standard specifically targeting computational load (Project 2026-02 — Computational Load Alignment Phase 1, comment period through April 30, 2026). SARs in NERC parlance are not standards; they are the authorization to draft a standard. The drafting will take months. The standard, once drafted, will go through a multi-round comment-and-ballot process. But the direction is set.

The federal layer is acting. It is acting fast. And it is acting with cross-agency consistency that is rare in American regulatory practice. FERC, DOE. And NERC are not always aligned. On large loads, in 2026, they are aligned.

Likewise, a note on the jurisdictional question. Because it is the design constraint that shapes every other piece of this story. The Federal Power Act, as amended, gives FERC authority over wholesale rates and over the interstate transmission of electricity. It gives the states authority over retail rates, over siting. And over the in-state distribution system. The line between wholesale and retail has never been bright. It runs through the substation. It runs through the meter. And in the case of co-located generation paired with co-located load, it runs through the facility — the same physical site contains generation that FERC could claim jurisdiction over under one set of theories and load that the state would claim jurisdiction over under another.

The DOE Section 403 proposal is

The DOE Section 403 proposal is not an attempted federal takeover of retail load. It is a more subtle instrument: an attempted federalization of the interconnection process for facilities that touch interstate transmission. This is essentially every facility above 50 to 100 MW. The states see the move clearly. They are responding clearly. NARUC’s filings are not mere protest; they are a position-staking exercise in advance of what NARUC’s commissioners believe will be a long set of contested cases at the D.C. Circuit. The June 2026 ruling will not end this fight. It will set the boundaries for the next decade of it.

There second federal piece worth

There is a second federal piece worth mentioning. Because it does not fit neatly into the FERC-DOE-NERC trinity but matters operationally: the Department of Defense’s interest in grid resilience for the data centers that increasingly host workloads with national security implications. The DoD has not yet entered the large-load rulemaking conversation as a formal participant. It is, however, an interested observer. Several of the Pentagon’s modernization efforts depend on commercial AI infrastructure that, under a strict reading of the new ride-through and curtailment rules, becomes operationally constrained in ways that affect mission readiness.

On the contrary, expect a DoD intervention — likely through a Defense Production Act invocation or a national security exemption framework — to enter the conversation before the end of 2026. It will not displace the regulatory wave. It will create a narrow corridor of exempt or differently-regulated facilities for defense workloads. The corridor will matter to a small number of operators and will not affect the broader market trajectory.

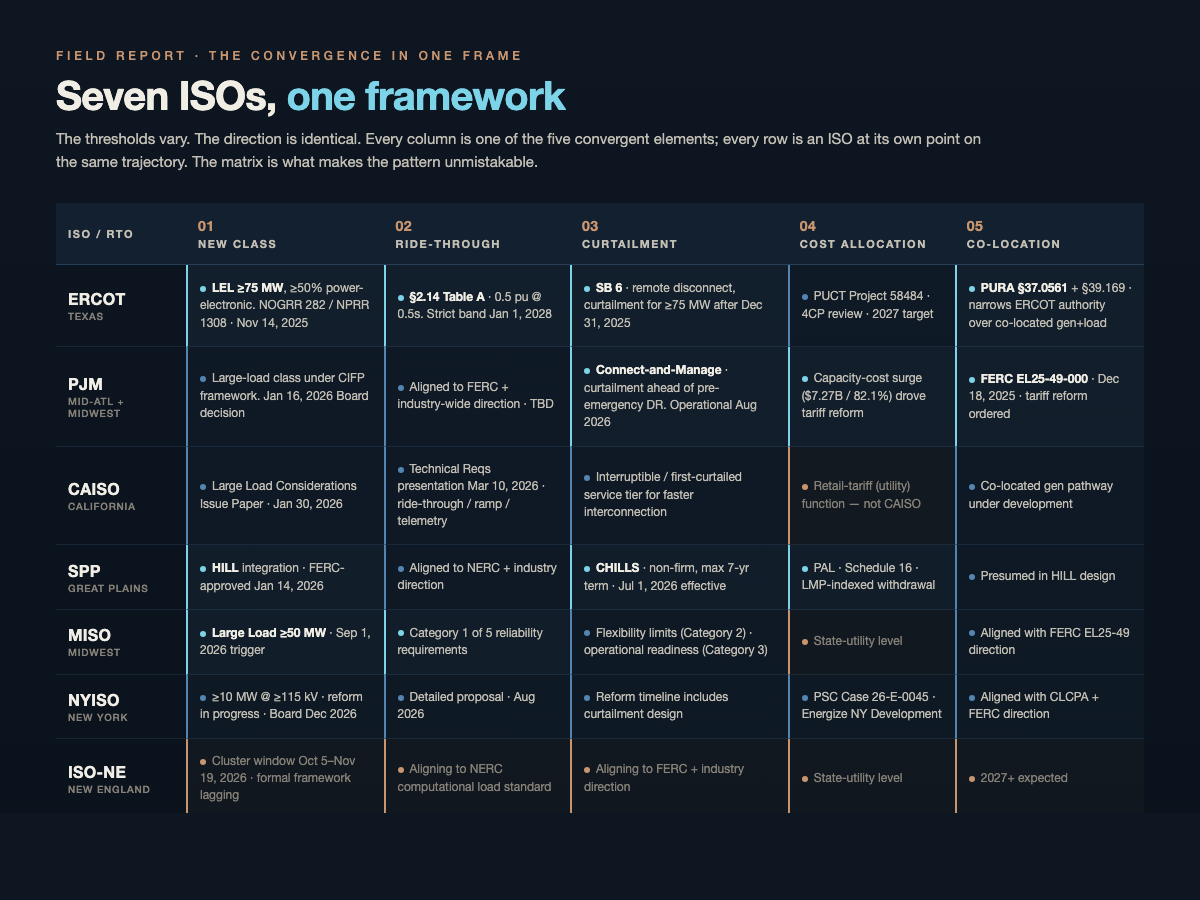

Part III — The ISOs

Below the federal layer sit the regional transmission operators and independent system operators that actually run the grids. Seven of them matter for AI infrastructure: ERCOT, PJM, CAISO, SPP, MISO, NYISO. And ISO-NE. Each is at a different point on the same trajectory. I will take them roughly in order of how far along the rulemaking is.

ERCOT — the first AI data center regulation to publish

ERCOT moved first because Texas had to. The 233 GW queue is not theoretical. It is the queue. The political pressure on the Public Utility Commission of Texas (PUCT) and on the legislature was acute. The legislature responded with Senate Bill 6, signed in 2025. This mandates remote-disconnect equipment and curtailment participation for new ≥75 MW loads after December 31, 2025. SB 6 also created PURA § 37.0561, which narrowed ERCOT’s operational authority over co-located generation+load arrangements — a structural carve-out that the architects of SB 6 understood would shift the economics in favor of behind-the-meter generation paired with controllable load.

Generally, technical implementation happening PUCT

Generally, the technical implementation of SB 6 is happening at PUCT through five parallel projects. Project 58481 is the heaviest — Large-Load Interconnection Standards. PUCT staff voted to publish proposed 16 TAC §25.194 on March 12, 2026, with a comment deadline of April 17, 2026; a final order is expected by mid-2026. Project 58479 covers net-metering arrangements. Indeed, project 58480 sets the large-load forecasting threshold at ≥10 MW. Moreover, project 58482 covers reliability and demand reductions; scoping started in January 2026 and adoption is expected later in the year. Project 58484 covers transmission cost allocation, with adoption targeted by year-end.

ERCOT itself filed NOGRR 282 +

ERCOT itself filed NOGRR 282 + NPRR 1308 on November 14, 2025. NOGRR 282 creates the Large Electronic Load (LEL) class — defined as facilities with peak demand of 75 MW or greater where 50 percent or more of that demand is power-electronic. The substantive technical requirement is a voltage ride-through bar of 0.5 per unit for 0.5 seconds. The strict band of compliance is effective January 1, 2028. There is an interim band before that. But the destination is clear.

In parallel, ERCOT contracted McKinsey to support improvement of the Large Load Interconnection process (ERCOT press release, December 12, 2025). The deliverables are expected to feed into the next round of NOGRR filings. The McKinsey engagement is a tell. ERCOT does not retain McKinsey to validate work it is confident in. The engagement signals that ERCOT staff understand the existing framework is the first iteration, not the final answer.

In short, the combination — NOGRR 282 codifying ride-through, SB 6 codifying curtailment, PUCT codifying cost allocation, McKinsey redesigning the integration model — makes ERCOT the most fully built-out large-load regulatory regime in the United States. Every other ISO is, in effect, watching what Texas did and adapting it.

PJM — the largest market reacts to AI data center regulation

PJM’s process is called the Critical Issue Fast Path, or CIFP. It is the highest-tempo stakeholder process PJM has, reserved for issues that cannot wait for normal stakeholder cadence. Large-load interconnection got CIFP’d in mid-2025 because the capacity-cost surge in the 2026/27 auction made it politically untenable to wait.

The CIFP decision was finalized on January 16, 2026. PJM published a board letter the same day. The decision had three substantive components.

Specifically, first, an Expedited Interconnection Track for large loads. The track is operational by August 2026. It compresses what used to be a multi-year cluster study into a fraction of that time, conditional on the load meeting specified technical and contractual requirements.

Second, a Connect-and-Manage framework for loads without on-site generation. The Board letter states the operative principle directly: “the incremental demand associated with such load growth would be subject to curtailment prior to the deployment of pre-emergency Demand Response.” That single sentence converts curtailment from an implicit tail risk into a contractual operating condition. Customers who can absorb interruption — and AI training workloads, run as batch jobs, absorb interruption better than almost any other industrial load class — get streamlined interconnection. Customers who need firm power pay for capacity and ride through the queue. The economic logic is clean. (Earlier 2025 drafts of the framework included a separate “Non-Capacity-Backed Load” product label; that label was dropped by October 2025 in favor of the unified Connect-and-Manage approach.)

Third, the framework permits explicit curtailment of unmet load in emergency conditions, potentially ahead of pre-emergency demand response. The implication is significant: in a true grid emergency, large loads without on-site generation are first in line to be shed, possibly before traditional demand response programs cycle.

For instance, combined with the FERC December 18, 2025 order in Docket EL25-49-000 requiring PJM to write transparent rules for co-located generation, the CIFP decision means PJM has, in the space of about ninety days, transformed itself from the most permissive large-load market in the country to one of the most structured. The operational changes hit in August. The cultural changes have already hit. Anyone who priced a PJM project on 2024 assumptions is repricing now.

CAISO — AI data center regulation treats load like generation

California has the smallest data center demand growth of the major markets. But its rulemaking is among the most technically aggressive. CAISO published the Large Load Considerations Issue Paper on January 30, 2026, with an information session on February 5. The issue paper outlines an approach that, in retrospect, was almost certain given CAISO’s history with renewables and storage interconnection.

The procedural nuance is important: CAISO has stated explicitly that the ISO does not study load interconnections — those are retail-service arrangements under the connecting utility’s tariff (PG&E, SCE, SDG&E), not under the CAISO tariff. What CAISO is doing is developing a parallel framework of technical requirements for large loads — ride-through, ramp behavior, telemetry. And dynamic modeling — to be enforced by the connecting utilities and reflected in CAISO transmission planning. The March 10, 2026 Technical Requirements presentation laid out the first concrete draft. Operating and ride-through characteristics are now modeled into transmission planning studies. The first-draft technical requirements were targeted for Q1 2026 and are being finalized.

Indeed, cAISO is also offering an interruptible / first-in-line-to-be-curtailed service tier in exchange for faster interconnection. The trade is straightforward. Take the curtailment exposure; cut years off the queue. For training workloads, the trade can pencil. For real-time inference workloads serving consumer products, it cannot.

SPP — the conditional bridge

SPP — the Southwest Power Pool, covering most of the Great Plains — got its High Impact Large Load (HILL) Integration rules approved unanimously by FERC on January 14, 2026 (effective January 15, 2026), and refiled CHILLS revisions on February 10, 2026 (Docket ER26-1323-000). The CHILLS effective date target is July 1, 2026.

SPP’s approach has two services. CHILLS — Conditional High Impact Large Load Service — is a non-firm conditional transmission service tier with a 90-day interconnection study, lower priority than firm Network Integration Transmission Service. And subject to curtailment when system conditions require. CHILLS is a “bridge” service capped at a maximum 7-year term before the customer must convert to firm service. The intent is clear: get the load on quickly, on a conditional basis, with the explicit understanding that curtailment is part of the bargain.

Still, the paired service is PAL — Price Adaptive Load (Schedule 16) — a non-firm service for loads “willing to take price adaptive load service and withdrawal based on real-time prices.” PAL customers pay LMP for withdrawals and receive no compensation when curtailing. The contractual structure is a withdrawal commitment indexed to real-time grid pricing rather than a dispatch instruction

The strict definition of a HILL in the SPP framework is a load that cannot be reliably served on a firm basis but seeks non-firm service. Curtailable by design. The framework presumes that controllability is the price of admission.

MISO — September 1, 2026

MISO — the Midcontinent ISO, covering fifteen states from Manitoba down to the Gulf — has set a hard trigger date. Beginning September 1, 2026, any load greater than 50 MW total capacity at a single site is classified as a Large Load. Existing loads above 50 MW that expand by 25 MW or more also fall into the framework.

Even so, the Large Load Working Group has built a five-category reliability requirements structure. Category one is performance and ride-through behavior. Indeed, category two is flexibility limits. Moreover, category three is operational readiness — telemetry and metering. Category four is system stability impacts. Category five is security and resilience.

MISO’s stated goals are speed to reliable power, clear interconnection reliability requirements. And sustained reliable operation. The framework is closer to CAISO’s in spirit — load-as-resource — than to SPP’s conditional-non-firm approach. The September 1 effective date is binding. Projects that would land in the MISO interconnection queue after that date should be designed assuming the framework applies.

NYISO — the December decision

New York is in the middle of a reform cycle, not at the end of one. NYISO has 48 large-load proposals totaling approximately 12 GW in its queue, up from six projects in 2022. Current interconnection studies trigger at 10 MW above 115 kV or 80 MW below 115 kV.

Moreover, the reform timeline is published. February through May 2026 is for concepts and challenges. June and July are for the straw proposal. August produces the detailed proposal and initial tariff revisions. December 2026 is the NYISO Board approval and FERC filing.

The state companion is PSC Case 26-E-0045 — “Energize NY Development” — opened February 12, 2026. The case is modernizing interconnection policy for load-intensive facilities under the Climate Leadership and Community Protection Act (CLCPA). New York’s Climate Act constrains the state’s generation mix in ways that make the data center demand surge politically and physically harder to accommodate than in Texas or Virginia. The CLCPA framework is going to drive NYISO toward something closer to the CAISO model — load procedurally treated like generation, with hard ride-through and telemetry requirements — rather than the SPP model of conditional non-firm service.

ISO-NE — the laggard, by design

New England is behind. ISO-NE has not yet published a structured large-load framework. Its approach to date has been to handle large-load proposals through Transmission Planning Studies and Needs Assessments coordinated with Participating Transmission Owners. The next cluster window opens October 5 and closes November 19, 2026.

Therefore, iSO-NE staff have signaled that the industry-wide direction — ride-through, ramp, telemetry, modeling — will be reflected in the next round of standards. The White House and FERC have signaled a preference for shifting cost burden to developers. ISO-NE will align. The question is on what timeline. The conservative answer is that a structured framework lands in 2027.

The seven ISOs do not look identical. But they look more alike than a comparison from 2024 would have predicted. And they will look more alike still by 2027.

A note on WECC and the non-ISO West

The Western Interconnection — broadly, everything from the Rocky Mountains to the Pacific, plus Baja California — is not organized as a single ISO outside of CAISO. The Western Electricity Coordinating Council (WECC) is the regional reliability entity. But it does not run a market. Most of the West operates through bilateral contracts and balancing authorities — Bonneville Power Administration in the Pacific Northwest, NV Energy in Nevada, PacifiCorp across multiple states, Salt River Project in Arizona, Public Service Company of Colorado, Tucson Electric Power. And dozens of smaller entities. The Western Energy Imbalance Market (WEIM) and the emerging Markets+ structure provide some real-time coordination. But the West’s regulatory landscape for large loads is balkanized in ways the Eastern Interconnection is not.

Notably, this balkanization cuts two ways. On one hand, it slows the convergence — a developer in Nevada or Colorado is dealing with a state PUC and a balancing authority rather than an ISO with a centralized rulemaking process. On the other hand, the absence of a single rulemaking forum has not prevented the West from moving in the same direction. WECC has begun convening a parallel large-load reliability working group through its Reliability Subcommittee. The output is expected to feed into NERC’s computational load standard rather than into a separate WECC-only standard. The state PUCs in Nevada, Colorado. And Utah have all opened or are opening generic dockets on data center interconnection in 2026. This combination is the same five-element framework, arriving on a slightly slower timeline and with more variance across jurisdictions.

For developers building anywhere in the Western Interconnection, the practical consequence is that the AI data center regulation map is less crisp than it is in ERCOT or PJM. But the architectural conclusion is the same. Build to the convergent AI data center regulation framework. The bilateral nature of Western contracting actually makes the architecture easier to commercialize. Because you negotiate directly with the balancing authority and the utility rather than navigating a centralized tariff. The downside is that you have to negotiate every site. Such upside is that the negotiation has structural levers.

Part IV — The states

Below the ISOs, in the legal architecture of American electricity, sit the state commissions. They write the retail tariffs. They approve cost allocation. Some protect residential ratepayers. And in 2026, they are all writing data center rules.

Texas — AI data center regulation under SB 6 and the PUCT projects

In practice, texas has the most fully built-out state framework. The vehicle is Senate Bill 6, signed by Governor Abbott on June 20, 2025, with implementation at the PUCT through the five projects already discussed and codified through proposed 16 TAC §25.194. The defining feature of the Texas approach is that it is operationally integrated with ERCOT. SB 6 creates PURA § 37.0561, which constrains ERCOT’s operational authority over co-located gen+load (limiting curtailment authority for facilities where co-located generation can serve ≥50 percent of the large-load demand and is non-exporting), and PURA § 39.169 governing net-metering arrangements between large loads and co-located standalone generators.

The combination effectively legislates a co-location-friendly posture into Texas law. The TDSP-level curtailment protocols required under SB 6 (for new ≥75 MW loads after December 31, 2025) sit on top of ERCOT’s NOGRR 282 ride-through requirements. Such two layers compose. A facility that complies with the ERCOT technical bar and the PUCT curtailment bar is, in the eyes of Texas regulators, in compliance. A facility that complies with one but not the other is not.

Virginia GS-5 — AI data center regulation by minimum-bill rate class

Virginia is the largest single concentration of data centers in the world. The State Corporation Commission approved the GS-5 rate class on November 25, 2025 (Case PUR-2025-00058), with provisions applying to new GS-5 contracts on or after January 1, 2027. GS-5 is a retail rate class. It is triggered by a utility customer above 25 MW with a monthly load factor above 75 percent. The trigger catches data centers cleanly and misses traditional industrial customers. This run at lower load factors.

By contrast, the substantive requirements are aggressive. GS-5 requires customers to pay a minimum bill equal to 85 percent of contracted distribution and transmission demand, plus collateral and guarantee obligations equal to up to 60 percent of the minimum charges, on a fourteen-year minimum contract, regardless of buildout. Minimum charges and collateral requirements stack on top.

Virginia’s mechanism is not curtailment-focused; PJM does the curtailment. Virginia’s mechanism is stranded-cost protection for residential ratepayers. The political logic is straightforward. Dominion Energy is building generation and transmission specifically to serve the Loudoun and Prince William data center clusters. If those data centers do not materialize at the promised scale — and the SCC has watched the queue inflation — residential ratepayers absorb the stranded cost. GS-5 puts that risk on the data center customer through the minimum-bill structure.

A 200 MW data center signing GS-5 is committing to roughly $300 million per year in demand-charge floor for fourteen years. That is a $4.2 billion balance-sheet commitment that does not flex with the buildout schedule, with hyperscaler tenant churn, or with whatever happens to AI economics in the late 2020s. For a single-purpose AI facility, GS-5 is close to uninsurable.

Ohio — AEP’s commit-or-pay tariff

Crucially, ohio’s framework is the AEP Ohio data center tariff, adopted by PUCO on July 9, 2025. The tariff requires data centers to commit to a minimum monthly billing demand of at least 85 percent of the customer’s highest previously established monthly billing demand, on a 12-year framework (4-year ramp-up plus 8-year fixed term).

Amazon, Google, Meta, Microsoft. And the Ohio Manufacturers’ Association sought rehearing. PUCO denied. (OMA has appealed to the Ohio Supreme Court.) The rejection is consequential. The companies most positioned to push back on commit-or-pay tariffs across the country failed in their first attempt to do so. In a February 2026 PUCO filing, AEP Ohio described the rule as “weeding out uncommitted data center load” — phantom queue reduction, working as designed. Ohio HB 706 (introduced March 2026) would extend the framework statewide.

Arizona — SRP, APS, and the ACC framework

Arizona has two parallel approaches. Salt River Project — a public power utility — implemented its Large Customer Integration Process (LCIP) and its E-67 commercial-industrial price plan. New customers above 20 MW must pay infrastructure costs upfront. Minimum billing is the greater of actual demand or 80 percent of forecasted load. SRP serves 59 large-load customers with about 7 GW of combined capacity.

Meanwhile, arizona Public Service operates in the regulated investor-owned utility space. APS’s large-customer peak is approximately 13.1 GW. The Arizona Corporation Commission held its Large Load Workshop on April 16, 2026, to begin the formal rulemaking. The workshop signaled the direction: longer contract terms, minimum-bill structures, power factor requirements, termination and collateral requirements. And direct cost assignment for generation and T&D.

Arizona is on track to land somewhere between Virginia (GS-5-style minimum bills) and SPP (curtailment + non-firm service tiers) by the end of 2026.

Tennessee — TVA’s federal-power model

TVA is a federal power marketing administration. This gives it a different regulatory posture from the investor-owned utilities. The thresholds are clear. Above 5 MW, TVA review is required. Above 100 MW, TVA board approval is required. The board approval requirement is functionally a check valve on the largest projects.

Data center load is 18 percent of TVA industrial demand in 2025 and projected to double by 2030. TVA’s board voted February 11, 2026 to add 150 MW to xAI’s Memphis allowance — roughly doubling it — and reversed previously planned closures of both the Kingston and Cumberland coal plants in the same decision cycle, citing data center demand growth. The combination of board-level project approval and the public scrutiny that comes with TVA’s federal status makes Tennessee a different kind of jurisdiction to develop in. The political process is the technical process.

Georgia — the rate-payer protection model

Georgia’s PSC approved Georgia Power’s roughly 10 GW (9,885 MW) gas expansion to meet data center load. The capital plan is approximately $16 billion. The concession the PSC extracted from Georgia Power and from the data center customers is a residential rate-payer protection. Such base rate is frozen through 2028 (per the July 31, 2025 PSC order). Large-load customers must allocate cost in the next base rate case sufficient to apply “downward pressure of at least $8.50 per month to the typical residential customer using an average of 1,000 kWh per month for the years 2029, 2030 and 2031” (Georgia Power data center fact sheet, verbatim).

Georgia’s framework also allows risk-based billing for loads above 100 MW. And load-flexibility programs are in development. The model is closer to Virginia’s — protect residential ratepayers from the cost of the buildout — than to Ohio’s. This is more focused on weeding out queue inflation.

North and South Carolina — the Duke Clean Transition Tariff

Duke Energy’s Carolinas territory has a 6 GW data center pipeline. Data centers are less than 1 percent of peak demand today and are projected to be roughly 10 percent by 2030. Two general rate cases are open — Duke Energy Progress filed in October 2025 and Duke Energy Carolinas filed November 20, 2025 — and large-load tariff updates are expected in both.

The Clean Transition Tariff is the unique piece. The CTT has been announced via MoU with Amazon, Google, Microsoft and Nucor but has not yet been filed as a tariff with the relevant Carolinas commissions. As contemplated, it would let data centers connect to the grid while developing their own clean energy supply. The legal structure is novel. The CTT essentially creates a transitional class — not quite behind-the-meter, not quite full retail — in which the customer is on the grid while their dedicated supply is being built out. If approved, the CTT becomes a template for other Southeastern utilities.

Oregon and Washington — the Pacific Northwest pivot

The Pacific Northwest had been one of the most data-center-friendly regions in the United States, with cheap hydropower and aggressive tax breaks. That posture is reversing.

Oregon

An amendment to the governor’s omnibus enterprise-zone legislation (SB 4084 / HB 4084 — the bill moved between chambers during the 2026 session) temporarily excluded data centers for at least one year from the expanded 10-year tax exemption. Governor Kotek’s office indicated support for the exclusion. New legislation is being drafted to require a separate rate structure for data centers with long-term contracts, including cost separation from other ratepayers. The shift is partly a fiscal calculation — the tax breaks were being challenged as fiscally unsustainable — and partly a political calculation about who pays for the infrastructure.

Washington

ESSB 6231 — signed by Governor Ferguson — repeals the sales and use tax exemption on replacement and refurbished data center equipment, effective July 1, 2026. Earlier drafts proposed a half-cent-per-kWh annual fee that would have generated roughly $30 million per year; that fee was cut via amendment. The Washington Clean Energy Transformation Act’s 100-percent-emissions-free electricity mandate by 2045 remains in force; the data center demand surge is shaping legislative debate about how the 2045 path is built, not whether it remains the target.

The Pacific Northwest is no longer a tax-arbitrage geography for data centers. It will still be a viable build geography for projects with strong economics on the merits. It is no longer the easy path it was in 2020.

Tribal land and public power — the underexplored corridors

One category of jurisdiction that does not show up in the headline rulemakings deserves a brief mention: tribal land and public power. Federally recognized tribes possess sovereign authority over their lands, including authority to set electricity siting and interconnection rules. A small but increasing number of AI data center projects are being structured on tribal land. The regulatory dynamics are different in ways that are not always to the developer’s disadvantage. Tribes have direct economic incentives, often-faster permitting timelines. And the ability to structure interconnection on terms that would not be available off-reservation. The federal jurisdictional question is in some ways simplified — tribal sovereignty creates a different relationship with federal agencies than state regulation does — and in some ways complicated. Because federal trust obligations and the National Environmental Policy Act still apply.

Public power utilities — TVA at

Public power utilities — TVA at the federal level. But also municipally owned utilities and rural electric cooperatives — are a parallel underexplored corridor. They are not subject to the same retail-rate regulation by state PUCs that investor-owned utilities are. They make their own decisions, on their own timelines, with their own boards. SRP in Arizona is a public power utility. So is the Los Angeles Department of Water and Power. So are the municipal utilities in Austin, San Antonio, Memphis, Seattle, and dozens of mid-sized cities. The collective load of US public power is roughly 15 percent of total US electricity demand. The willingness of public power entities to host large data center loads varies enormously. But the speed at which a willing public power utility can move dwarfs the speed of the IOU-PUC process.

Neither tribal land nor public power changes the convergent framework. The reliability physics is the same; ride-through is ride-through; curtailment is curtailment. What they change is the speed of negotiation and, in some cases, the ability to structure economically on terms that the standard PUC process does not permit.

Part V — The Hardware Compliance Gap in AI Data Center Regulation

Now we come to the most technical part of the story, and the most consequential.

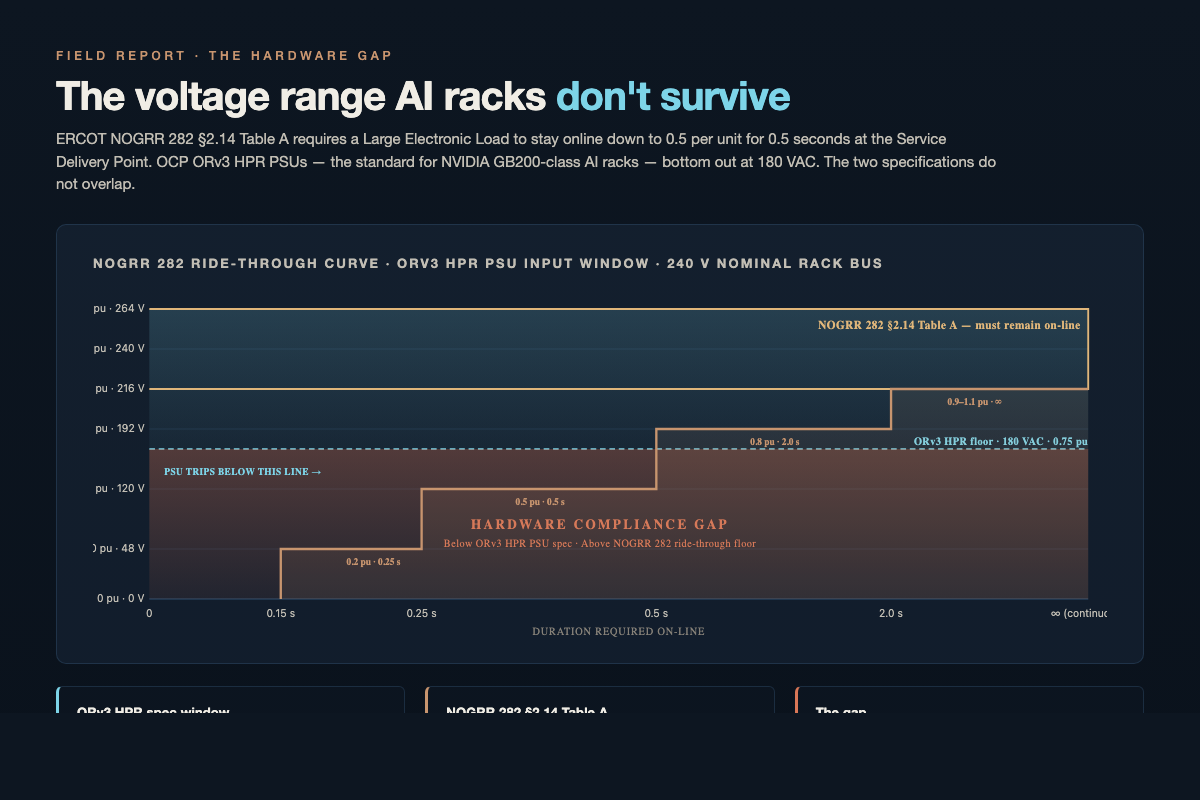

The dominant hardware platform in hyperscale AI data center construction is the Open Compute Project — OCP. OCP’s current rack-and-power architecture is ORv3. The variant that matters for AI deployment is the ORv3 HPR (High Power Rack) 5.5 kW PSU shelf — the Meta-contributed design used in NVIDIA GB200 NVL72 and Blackwell-class racks, built by Advanced Energy, Delta. And Lite-On. The published input voltage window of the ORv3 HPR PSU is 180 to 305 volts AC. Below 180 VAC, the PSUs are not rated to operate. They will trip. Whatever the IT-layer load is doing — training a model, serving inference, running validation — it stops. Whatever the rack-level orchestration is doing — checkpointing, gradient synchronization, KV-cache management — it stops. (The earlier 3 kW ORv3 PSU runs a narrower 200–277 VAC window. Neither variant brackets the NOGRR 282 ride-through floor.)

Voltage ride-through requirement codified ERCOT

The voltage ride-through requirement codified in ERCOT NOGRR 282 §2.14 Table A — and being drafted in MISO, ISO-NE, at NERC. And as technical requirements at CAISO — requires the load to remain online during voltage excursions to 0.5 per unit for 0.5 seconds, measured at the Service Delivery Point (transmission-side, typically 138 kV or 345 kV). What reaches the IT rack depends on the customer-owned transformers, MV bus design, UPS topology, and any series compensation between the SDP and the rack. A naïve LEL with no upstream conditioning would see the per-unit sag propagate downstream — and 0.5 pu on a 240 V nominal rack bus is 120 VAC, well below the ORv3 HPR 180 VAC floor. The deeper bands in NOGRR 282 (0.25 s at 0.2–0.5 pu; 0.15 s below 0.2 pu) are deeper still.

Why no IT-layer patch wo

This is the hardware compliance gap. It is universal across every market that codifies ride-through. It is not a gap that is patchable in firmware; the PSUs do not have the capacitive headroom to ride through voltage sags below their input window without the upstream voltage being conditioned to keep the PSU input above its lower bound.

OCP’s own standard Battery Backup Unit (BBU) shelf spec rev 1.4 provides a partial rack-level mitigation — when AC sags, the BBU holds the 48V busbar above 46V for a defined window of seconds. But the BBU architecture was sized for occasional ride-through events, not the repeated-disturbance regime that the NOGRR 282 full curve and the NERC computational load standard contemplate. At >100 MW campus scale, BBU shelves multiply Li-ion fire load, cycle continuously on every grid disturbance, and create a cost and footprint profile that breaks the economics. An independent October 2025 research paper (arXiv 2510.03867, Enhancing Data Center Low-Voltage Ride-Through) reaches the same conclusion from a wholly different starting point: the fix must come from internal distribution-network voltage control plus utility-scale BESS, not from the PSU.

There are, in practice, two architectural responses.

The first is to replace or substantially modify the PSUs in every rack across every site, or to stack rack-level BBU shelves heavily enough to convert occasional ride-through into routine cycling. Both are functionally impossible at hyperscale economics. The supply chain is built around OCP-conforming hardware. The PSU vendors are not redesigning around 0.5 pu ride-through. This capex of a swap is unrecoverable. The validation lift on a custom PSU specification is enormous. Hyperscalers buy hardware from the OCP ecosystem precisely because the standardization compresses cost and time to deployment.

The second is to solve the problem upstream of the PSU at the facility infrastructure layer, with a hybrid architecture composed of three coordinated elements:

- Rotational mass and conditioned power feeding the IT load — Dynamic UPS, or DRUPS: a flywheel, an engine, and a synchronous machine on a common shaft. The synchronous machine sits between the utility supply and the IT load. When the utility voltage sags, the rotational inertia keeps the IT-side voltage within spec for the milliseconds-to-seconds window needed to ride through a transient or engage the engine for sustained operation.

- Medium-voltage Battery Energy Storage — sized for real-power ride-through on the seconds-to-minutes timeframe, paired with the synchronous machine to extend the ride-through window beyond what rotational mass alone provides. Siemens, ABB, and HITEC all publish MV BESS reference designs specifically for industrial bus ride-through.

- Low-voltage capacitor banks (or STATCOMs) on the IT bus — for cycle-by-cycle reactive support during the deepest portions of a voltage sag. NEPSI, Southern States, and ABB sell MV metal-enclosed capacitor banks specifically for sag mitigation on industrial buses; STATCOMs handle the same reactive duty with faster response and continuous compensation.

The three-element hybrid is the standard mission-critical architecture in hospitals, broadcast facilities, financial trading floors, and military command centers — environments where IT-layer power quality cannot fail. Applying it to AI infrastructure at the gigawatt scale is a step-change in deployment, but it is not a step-change in technology readiness. The vendors exist. The integration patterns are well understood. This capital cost is meaningfully higher than static UPS alone. But the rejection of the architecture in mainstream data center construction has been a function of price competition, not of technical inadequacy.

The hardware compliance gap will be closed one of two ways across the United States in the next two to four years. Either the IT-layer hardware will adapt — slowly, expensively, and incompletely — or the facility-layer infrastructure will absorb the new requirement through the hybrid above. Most of the projects under construction today have made the wrong bet. The bet they have made is that the regulator will back down or that the standard will be relaxed. Neither is going to happen, because the reliability case for ride-through is not a discretionary policy choice. It is a physics constraint on a grid serving hundreds of gigawatts of new computational load.

There is one more piece of the engineering math worth surfacing. Because it explains why static UPS with a battery string is not the answer most data center designers default to. A static UPS — battery-backed — can theoretically ride through a voltage sag if the battery is healthy, the inverter is sized correctly, and the transition logic is fast. In practice, at hyperscale, none of those conditions reliably hold. Battery strings degrade. Inverters introduce harmonic distortion that can itself trip downstream PSUs. Transition logic fails in the small percentage of disturbance scenarios that turn out to matter most.

The literature on battery-string failure modes in mission-critical applications is not encouraging. The reason DRUPS exists as a category — the reason it has been the standard in hospitals and broadcast for decades — is that the rotational mass of a flywheel paired with the inertia of a synchronous machine produces ride-through behavior that conventional static UPS configurations can approximate but not match. This MV BESS layer in the SAVRN-class hybrid architecture is sized and located differently from a static UPS battery string — it sits at medium voltage on the facility bus, not at low voltage in series with the IT load — so the failure modes that plague static UPS at the rack do not propagate the same way.

For computational loads at the scale that ERCOT, MISO, CAISO, and NERC are now writing rules for, the engineering judgment that has held for half a century in mission-critical environments is the engineering judgment the data center industry is going to inherit. The capital cost premium for the hybrid architecture over static UPS — historically the reason data centers chose batteries alone — collapses when the alternative is a curtailment penalty under PJM Connect-and-Manage or a failed interconnection study under NOGRR 282. The economics flip. This architecture flips with them.

Part VI — The co-location consensus

Across the federal layer, the ISO layer, and the state layer, a single architectural pattern has emerged as the AI data center regulation winner. That pattern is co-located generation and load.

FERC’s December 2025 order to PJM. DOE’s October 2025 Section 403 directive with its fourteen principles, several of which explicitly enable joint co-located interconnection requests. Texas SB 6’s PURA § 37.0561, narrowing ERCOT’s operational authority over co-located arrangements. PJM’s CIFP decision creating tariff space for co-located gen+load. Duke Energy’s Clean Transition Tariff, providing a transitional rate structure for customers developing their own clean supply. SPP’s CHILLS service, presuming the load is operationally curtailable in part because most CHILLS-eligible projects pair load with on-site generation.

The convergence is not a coincidence and it is not an accident. It is the answer to a problem the regulators have all been working on independently.

The problem is that grid-only supply for hundreds of GW of new computational load is impossible to build on the timeline that the demand requires. New transmission takes 8 to 12 years. New generation in some regions takes 4 to 7 years. The data center developers want to be operational in 18 to 24 months. The math does not work without on-site generation at scale.

But on-site generation by itself is also insufficient. A data center with on-site generation but uncontrollable load is still a problem for the grid in disturbance scenarios. The regulators want co-located generation paired with controllable load. That combination — generation behind the point of interconnection, plus a load that can be ramped down or curtailed in seconds — is the architecture that solves the demand problem and the reliability problem simultaneously.

The economic logic for the developer follows the regulatory logic. A facility with on-site generation can negotiate better interconnection terms (faster, with less upstream upgrade cost). A facility with controllable load can earn ancillary services revenue and can avoid minimum-bill exposure. Such facility with both gets the regulatory speed-to-power and the financial flexibility that single-purpose data centers cannot.

This is, not coincidentally, the architecture I built my company around. It is also the architecture that a growing number of competitors are now scrambling to retrofit toward, because the AI data center regulation direction is unambiguous. The retrofit cost is enormous. The greenfield cost premium for designing co-located from the start is real but bounded — perhaps 15 to 25 percent on capital, with payback windows of 3 to 5 years from the avoided cost of curtailment penalties, the captured ancillary services revenue. And the avoided minimum-bill exposure.

The companies that designed for this from the start will have the next two years to themselves. The companies that retrofit will have the four years after that. This companies that did not read the filings will have whatever the curtailment penalty leaves them.

Part VII — What Happens Next in AI Data Center Regulation

Forecasting in regulatory environments is harder than forecasting in markets, because the variable that moves is human judgment under political constraint, not aggregated buying behavior. But the scaffolding for the next twenty-four months is already in place, and the major decision points are scheduled.

End of June 2026. FERC rules on the DOE Section 403 proposal. The most likely outcome is the hybrid: federal minimum technical standards for ride-through, telemetry, and curtailment capability; state authority preserved over cost allocation; co-location framework federalized. If FERC rules that way, every project in development with conventional architecture has a six-to-twelve-month window to either redesign or decide to absorb the regulatory risk.

July 1, 2026. SPP CHILLS effective date. SPP becomes the second major US power market with a structured large-load framework operational at scale. Watch for early enrollment numbers; they will tell us how the developer community is responding to conditional non-firm service.

August 2026. PJM Expedited Interconnection Track operational. Watch for which projects file first; the early filings will indicate which developers have architectures ready to meet the technical and contractual bar.

September 1, 2026. MISO Large Load framework trigger date. After this date, every load above 50 MW in MISO territory is subject to the new AI data center regulation framework.

October-November 2026. ISO-NE cluster window. Watch for whether ISO-NE publishes new technical requirements aligned with the convergent framework or sticks with the current Transmission Planning Studies approach.

December 2026. NYISO Board approves the new tariff and files at FERC. Watch for the FERC review timeline; an expedited review puts NYISO on a 2027 effective date, which would align New York with the federal trajectory.

End of 2026. PUCT Project 58484 — Texas transmission cost allocation. The final piece of the SB 6 implementation puzzle.

2027. Virginia GS-5 effective. AEP Ohio tariff matures past the four-year ramp-up. Arizona ACC framework operational. The cost-allocation wave hits in earnest.

2028. ERCOT NOGRR 282 strict band effective. By this point, every major US power market has either an operational large-load framework or a published one with a near-term effective date.

The window for being ahead of this — for having built to the framework before the framework was law — closes somewhere in 2027. After that, every project will be designed to the new envelope. The structural advantage compresses. The economics flatten across the industry. This companies that read the filings early will have built positions; the companies that did not will be retrofitting.

The retrofit cost is hard to estimate precisely because every site is different. A reasonable bracket, based on conversations with EPCs, PSU vendors. And DRUPS integrators, is in the range of $0.8 million to $1.6 million per megawatt of installed IT capacity for retrofitting a conventionally-designed AI facility to a co-located, DRUPS-protected, controllable-load architecture. For a 200 MW facility, that is a $160 million to $320 million retrofit bill. For most existing developers, that is the difference between a project that pencils and a project that does not.

The other path — accepting curtailment penalties under PJM NCBL, SPP CHILLS, or the equivalent — is bounded but not small. The penalty structure varies by market. But the order of magnitude of the curtailment-exposure NPV for a non-compliant facility is in the single-digit-percent of gross facility revenue, accruing year over year, with the embedded option for the regulator to tighten the band as system stress grows. That option value is the part of the analysis that most underwriters are not yet pricing.

The capital markets implication

The capital markets are about twelve months behind the regulators on this. That is not unusual; capital markets are usually behind the regulators on technical rule changes. But the gap is unusually consequential here because of the deal-vintage problem.

Consider the cohort of AI data center deals that closed in 2024 and the first half of 2025. They closed on architectures that were state-of-the-art at the time of close — utility-supplied power, static UPS, OCP-conforming racks, no controllable load layer, no on-site generation. They closed at valuations that priced grid power at conventional industrial-customer rates, with no curtailment exposure, no minimum-bill commitment, no fourteen-year demand floor. The underwriting did not contemplate the AI data center regulation wave that was about to hit. Because the regulatory wave was not yet visible in the way the capital markets pay attention to.

That cohort now faces a re-rating. Not all at once. And not necessarily through a public marker, but progressively as each project encounters its first interconnection study under the new rules, its first PUC filing, its first capacity-cost assessment under the new tariffs. The re-rating will appear first as project delays — interconnection studies that take longer than the original schedule, additional engineering scope that did not exist in the original budget, contractual modifications to satisfy minimum-bill requirements. It will appear second as financing-side adjustments — covenant breaches, debt service coverage compressions, equity infusions to bridge construction-period overruns. It will appear third, eventually, as full re-syndications or asset sales at marks that price in the regulatory exposure that was not visible at the original close.

I am being deliberately careful in how I characterize this because I do not want to overstate the immediate effect. There is no Lehman moment in AI data center finance. The cohort exposure is real but spread across many sponsors, many lenders, many vintages. The hyperscaler tenants — the entities ultimately taking the offtake — are the most creditworthy customers in the global economy, and they will keep their commitments. What changes is the project-level economics, the developer’s equity return, and the ability of the asset to be refinanced or sold at the marks the original underwriting assumed.

For the next vintage of capital — the deals that will close in the second half of 2026 and through 2027 — the pricing should already reflect the new framework. The deals being structured now in the offices I am closest to are pricing it. The diligence questions are different. This appraisals are different. The covenants are different. The operating assumptions are different.

The companies that priced ahead of the wave will look prescient. The companies that did not will look exposed. This difference between the two cohorts will become legible to the public markets sometime in 2027.

Coda — the people in the rooms

The engineers who are writing these standards are mostly not famous. They are not well-paid by the standards of the industries they regulate. They are not, individually, household names. The most consequential names in this story are people like Michael Brown, who runs the NERC Standards Committee processes and shepherded the computational load SAR through. People like the staff at PJM who built the CIFP framework. The CAISO planners who wrote the Large Load Considerations Issue Paper. The PUCT staff who drafted the SB 6 implementation projects. This Virginia SCC commissioners who approved GS-5 over heavy industry lobbying. The Arizona ACC staff who organized the April Large Load Workshop.

These are not adversaries of the industry. Many of them came out of the industry. But they are operating under a constraint that the industry has not fully internalized: the constraint that the grid is not optional, that residential ratepayers vote. And that the political tolerance for “the data centers will just figure it out” has run out.

The grid is being asked to accommodate a customer class whose growth curve is unprecedented in the history of American electricity. It is not being asked nicely. The customer class showed up with 233 GW of queue and a take-it-or-leave-it timeline. The grid is responding the only way it can — by writing rules.

Those rules are converging across the country because the underlying physics is the same in every market. Voltage sag does not respect state lines. A capacity shortage in PJM does not become a different problem when it crosses into MISO. The 5-element framework — new class, ride-through, curtailment, cost allocation, co-location — is not a coordinated federal-state plot. It is what every honest grid engineer arrives at when they sit down with the load forecast and the reliability data and try to write a rule that lets the system work.

I have been in some of those rooms. I have read most of those filings. Honestly I have built a company around the bet that the convergence would happen and that the architecture compliant with all five elements would be the structural winner. The bet is no longer speculative. The filings are public. This dates are on the calendar. The convergence is documented.

The only question left, for builders and financiers and advisors and regulators reading this, is whether you read the filings in time to act on them.

That question is not rhetorical. It has an answer. The answer is in the 233 GW queue, in the $7.2 billion capacity-cost surge, in the 4.5 GW of CAISO study load, in the 12 GW of NYISO proposals, in the 6 GW of Duke Carolinas pipeline, in the 7 GW SRP fleet, in the 13 GW APS peak, in the 18 percent and doubling of TVA industrial load. It is in the November 14, 2025 filing of NOGRR 282. It is in the December 2025 FERC order to PJM.

And is in the January 16, 2026 PJM CIFP decision. It is in the January 30, 2026 CAISO issue paper. It is in the February 10, 2026 SPP refiling. And is in the March 11 and 18, 2026 NERC actions. It is in the April 16, 2026 Arizona workshop. It is in every state docket and every ISO board letter and every federal directive issued in the last fourteen months.

The quiet rewrite is happening. It is happening fast. It is happening in every market in the country at the same time. The architecture that survives it is the architecture that took the filings seriously when they were still drafts.

A final thought, for the people who will be reading this in 2028 trying to understand how their underwriting got away from them. You did not miss this because the information was hidden. You missed it because the information was distributed across forty-seven dockets in fourteen jurisdictions and nobody paid you to read all of them. The work of integrating those filings into a coherent picture was never going to be done by your investment committee on a deal-by-deal basis. It had to be done by somebody whose business depended on getting the picture right.

The companies that did that work — and there are not many of them — are the ones whose names you will read about in the 2028 retrospectives. The companies that did not are the ones whose names you will read in the workout press releases. This difference between the two cohorts was visible in 2026. It was visible in plain sight. It was visible in the filings. The only thing that varied between operators was whether they read them.

Chad Everett Harris is the co-founder of Savrn. He builds the infrastruture for the token economy. Sources for every regulatory citation in this article live in the public dockets at FERC, NERC, the seven ISOs, and the relevant state commissions; the consolidated reference list is available on request.

What AI data center regulation means going forward

By the end of 2027, AI data center regulation will look meaningfully like a single national framework with state-level cost-allocation variation. Companies that designed for this regime before it existed in codified form will hold a structural advantage that competitors retrofitting toward compliance cannot replicate quickly. The capital markets will reprice projects against the new rules as each tranche of effective dates lands. The framework is no longer a forecasting variable. It is the new floor.

For builders, financiers, advisors, and operators reading this, the question is not whether AI data center regulation is real. It is. The question is whether you read the filings in time to act on them — and whether the architecture you are deploying is compliant with AI data center regulation as written, not as you wish it were.

Notes on sources

This article draws on the US Large-Load Regulatory Landscape — Deep Research working paper (Savrn Platform Materials, May 10, 2026, v1.0), which compiles primary citations from:

- FERC — December 2025 order to PJM on co-located generation; pending June 2026 ruling on DOE Section 403 proposal.

- DOE — Secretary Wright’s October 23, 2025 invocation of Section 403 authority and the accompanying fourteen principles; January 2026 Winter Storm Fern 202(c) emergency orders to PJM, Duke, and ERCOT.

- NERC — February 2026 Large Load technical conference; March 11, 2026 RSTC approval of LLWG whitepaper #2; March 18, 2026 Standards Committee acceptance of the computational load SAR; FAC-002-4 in-force standard.

- ERCOT — NOGRR 282 + NPRR 1308 filings of November 14, 2025; ongoing McKinsey-led Large Load Integration redesign.

- PJM — January 16, 2026 Critical Issue Fast Path Decision board letter.

- CAISO — January 30, 2026 Large Load Considerations Issue Paper; February 5, 2026 information session.

- SPP — January 2026 FERC approval of HILL Integration; February 10, 2026 refiling of CHILLS and PAL; July 1, 2026 target effective date.

- MISO — Large Load Working Group framework; September 1, 2026 trigger date.

- NYISO — reform timeline running through December 2026 board approval; PSC Case 26-E-0045 (“Energize NY Development”) opened February 12, 2026.

- ISO-NE — October-November 2026 cluster window.

- Texas — Senate Bill 6 (2025); PUCT Projects 58479, 58480, 58481, 58482, 58484; March 12, 2026 publication of the 58481 draft.

- Virginia — SCC GS-5 rate class approved November 25, 2025, effective 2027.

- Ohio — AEP Ohio data center tariff (PUCO-approved 2025); 2026 Ohio House extension bill.

- Arizona — SRP LCIP and E-67 (2025); ACC Large Load Workshop, April 16, 2026.

- Tennessee — TVA contract review thresholds; February 2026 xAI Memphis allowance doubling.

- Georgia — Georgia PSC approval of Georgia Power’s 10 GW gas expansion; large-load billing and rate-payer protection structure.

- Carolinas — Duke Energy Progress and Duke Energy Carolinas general rate cases; Clean Transition Tariff under evaluation.

- Oregon and Washington — HB 4084 (OR); SB 6231 (WA).

The convergent five-element framework — (1) new regulatory class, (2) voltage and frequency ride-through, (3) mandatory or conditional curtailment, (4) cost allocation via minimum-bill or take-or-pay tariffs, (5) co-located generation and load encouraged or required — is the analytical synthesis derived from reading these filings in parallel.

Every claim in this report has a primary source on the public record.

If you challenge any specific number, date, tariff, or technical claim in this article, the trail is documented. FERC dockets, ISO board letters, state PUC orders, OCP datasheets, and the Independent Market Monitor’s published analysis — every URL is one click away.

→ View the full sources & citations