AI data center natural gas turbines are now the binding constraint on United States AI capacity deployment through 2028, with GE Vernova reporting an order backlog above $30 billion and committed heavy-duty turbine production slots through 2029, per the GE Vernova Q1 2026 earnings release. SAVRN is the operator of an off-grid sovereign AI infrastructure campus model. SAVRN owns its power generation, compute, and closed-loop liquid cooling, deploying in 6 to 12 months versus the 24-to-48-month industry standard. The AI data center natural gas turbines orderbook is therefore the single most consequential procurement decision on any AI infrastructure capex authorization signed in 2026.

This brief writes the 2026 operator playbook on AI data center natural gas turbines. It pairs the GE Vernova Q1 2026 earnings disclosure with Mitsubishi Power and Siemens Energy 2025 results, the Wood Mackenzie Q2 2025 transformer market survey, the U.S. Energy Information Administration Annual Energy Outlook 2025, the North American Electric Reliability Corporation 2025 Long-Term Reliability Assessment, the International Energy Agency Energy and AI 2025 report, and the Lawrence Berkeley National Laboratory Queued Up 2025 Edition into a single decision frame for AI infrastructure operators, CFOs, and sovereign-program buyers. Every load-bearing number is sourced. Every geography named falls inside the SAVRN development footprint of California, Texas, Colorado, Nebraska, Panama, and Barbados.

Furthermore, the AI data center natural gas turbines shortage is not a temporary congestion event. GE Vernova booked over $30 billion in gas power orders during 2025, and the company’s Q1 2026 earnings release reported that heavy-duty production slots are now allocated through 2029. Mitsubishi Power has moved its heavy-duty H-class fleet to selective order acceptance, per its 2025 disclosures. Siemens Energy reported double-digit growth in heavy-duty gas turbine orders and a multi-year delivery backlog, per its 2025 annual report. The structural deficit is therefore confirmed across all three major heavy-duty manufacturers. AI data center natural gas turbines are now slot-allocated rather than catalog-procured.

Why AI data center natural gas turbines are the binding 2026 procurement constraint

The grid interconnection backlog already documented by the Lawrence Berkeley National Laboratory Queued Up 2025 Edition places 2,060 gigawatts of generation and storage in active queue at the end of 2024, with typical waits stretching to five years. The Federal Energy Regulatory Commission Order 2023 reform reduces speculative applications but does not produce new transmission lines or substation capacity inside the 2026 to 2028 capex window. As a result, AI operators are pivoting decisively to behind-the-meter generation. AI data center natural gas turbines are the only mature thermal technology that can deliver dispatchable, behind-the-meter capacity at the 200-to-500-megawatt scale the AI campus class now requires.

The pivot has compounded against limited manufacturing capacity. GE Vernova built its heavy-duty turbine production footprint, primarily centered in Greenville, South Carolina and supported by global supply chain partners, against an assumption that gas generation additions would moderate through the late 2020s. The U.S. Energy Information Administration Annual Energy Outlook 2025 instead projects natural gas capacity additions north of 130 gigawatts through 2050, with the near-term surge concentrated in the 2026 to 2030 window. The North American Electric Reliability Corporation 2025 Long-Term Reliability Assessment confirms that natural gas now bears the dominant share of incremental dispatchable capacity. AI data center natural gas turbines compete inside this surge for the same hot-section castings, the same generator step-up transformers, and the same balance-of-plant integrators.

For the AI operator, the implication is operational. The 2026 procurement window for AI data center natural gas turbines is open, narrow, and closing. Operators that file slot reservations before 2026 year-end will land megawatts in 2027 and 2028. Operators that defer slot reservations until utility interconnection clarity arrives will discover that the slot itself has been allocated, not just to AI competitors but to merchant developers, industrial customers, and utility resource adequacy programs. Therefore, the AI data center natural gas turbines procurement decision now sits ahead of, not after, the site selection decision in any rational 2026 deployment sequence.

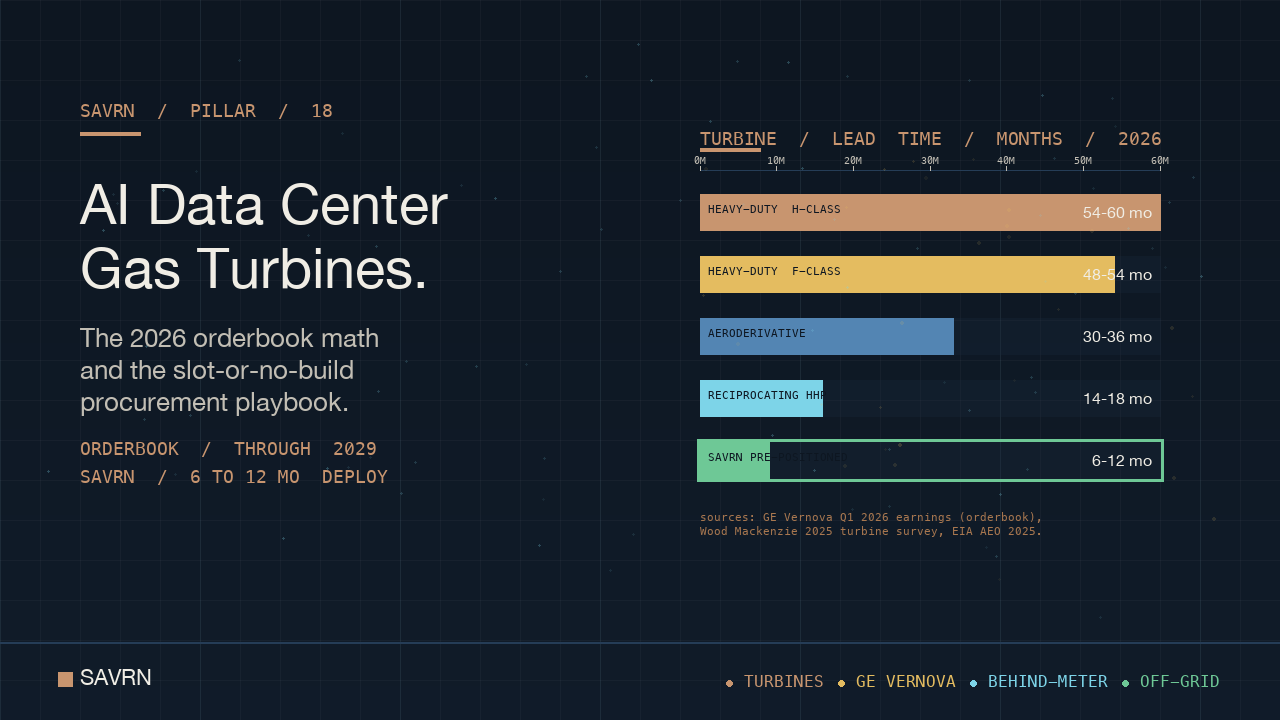

The 2026 AI data center natural gas turbines orderbook by the numbers

GE Vernova reported $30+ billion in gas power orders during 2025 and disclosed in its Q1 2026 earnings release that heavy-duty turbine production slots are booked through 2029, with selective acceptance for any 2030 and beyond delivery commitments. The company’s Power segment backlog reached the highest level in its history, with gas as the dominant component. Mitsubishi Power, the largest competitor in the heavy-duty AI data center natural gas turbines category, has moved its M501JAC and M701JAC H-class platforms to allocated production, prioritizing strategic customer commitments per its 2025 sector outlook. Siemens Energy reported double-digit growth in heavy-duty gas turbine orders and named AI data center demand as the leading source of incremental commitments, per its 2025 annual report.

Inside the smaller turbine and reciprocating engine categories, the orderbook tightening is comparably severe. GE Vernova LM6000 and LMS100 aeroderivative platforms now run 30 to 36 month lead times for non-strategic customers, per industry analyses of 2025 and 2026 OEM disclosures. Solar Turbines, a Caterpillar subsidiary, has expanded production capacity but reports multi-year backlogs on the Titan 250 and Titan 350 industrial gas turbine platforms. Cummins announced a $150 million expansion of its Fridley, Minnesota facility in February 2026 to increase QSK95 high-horsepower reciprocating engine output by 30 percent, citing data center demand. Caterpillar’s Q1 2026 results reported a $63 billion total backlog with significant data center exposure across its 3500 and 3600 series gas-fueled engines.

The cross-sectional orderbook math therefore confirms a multi-year supply deficit across every AI data center natural gas turbines class that an AI campus could plausibly deploy. Heavy-duty H-class platforms with delivery dates inside 2026 and 2027 are unavailable to any operator that has not already posted a slot reservation. F-class heavy-duty platforms run 48 to 54 month lead times. Aeroderivative platforms run 30 to 36 months. High-horsepower reciprocating engines run 14 to 18 months. The orderbook is therefore not a price-sensitive market in 2026. It is a slot-allocation market. The CFOs who recognize this distinction will land megawatts. The CFOs who do not will write capex plans against capacity that the market cannot deliver.

How turbine class shapes AI data center natural gas turbines procurement

Turbine class shapes the AI data center natural gas turbines procurement decision through four dimensions: capacity per unit, lead time, capex per megawatt, and heat rate. Heavy-duty H-class platforms deliver roughly 450 to 600 megawatts of net electric output in combined-cycle configuration, with simple-cycle output in the 300 to 400 megawatt range. Heavy-duty F-class platforms deliver roughly 200 to 280 megawatts in combined-cycle configuration. Aeroderivative platforms deliver 30 to 100 megawatts per unit. High-horsepower reciprocating engines deliver 2 to 20 megawatts per unit. The size hierarchy directly maps to the AI campus deployment unit. A 200 megawatt AI campus is the natural fit for a single heavy-duty F-class unit, two aeroderivative units, or a fleet of 10 to 100 reciprocating engines.

Capex per megawatt also varies materially by AI data center natural gas turbines class. Heavy-duty H-class combined cycle deployments run roughly $700 to $1,100 per kilowatt installed, per industry analyses of 2024 and 2025 EPC reference data. F-class combined cycle runs roughly $900 to $1,300 per kilowatt. Aeroderivative simple cycle runs $1,000 to $1,500 per kilowatt. High-horsepower reciprocating engine plants run $1,200 to $1,800 per kilowatt depending on emissions controls and balance-of-plant scope. Heat rate also varies. H-class combined cycle achieves heat rates around 6,000 BTU per kilowatt hour. Aeroderivative simple cycle runs 9,000 to 10,500 BTU per kilowatt hour. Reciprocating engines run 7,500 to 8,500 BTU per kilowatt hour in simple cycle.

For the AI operator, the turbine class selection therefore optimizes against three operational realities. First, AI inference and training loads are flatter than utility loads, favoring high-efficiency baseload designs. Second, AI campus deployment timelines now require fastest-available delivery, favoring the smaller classes with shorter lead times. Third, AI campus designs benefit from modularity, favoring fleets of smaller units over single large units. SAVRN’s hybrid generation stack reflects this optimization, layering H-class units where slot reservations are available, aeroderivative units where flexibility and shorter lead times matter, and high-horsepower reciprocating engines for the fastest-deployment increments. The AI data center natural gas turbines procurement decision is therefore not a binary platform choice. It is a fleet composition decision.

Five blockers that stretch AI data center natural gas turbines lead times

Blocker 1: OEM hot-section capacity stretches AI data center natural gas turbines lead times

Hot-section castings, including the first-stage and second-stage turbine blades and vanes, are the binding manufacturing constraint on heavy-duty AI data center natural gas turbines. Hot-section production requires investment-cast superalloy components produced in a small number of qualified foundries globally. GE Vernova’s hot-section supply chain runs primarily through its Greenville, South Carolina component plant and a tight cluster of qualified third-party foundries. Mitsubishi Power produces hot sections at its Takasago Works in Japan. Siemens Energy produces hot sections in Berlin and at a small number of partner sites. Capacity expansion at any of these sites requires a 24-to-36-month build-out for a new precision investment casting line, per industry analyses of 2024 and 2025 capital expansion programs.

Blocker 2: Generator step-up transformer shortage compounds AI data center natural gas turbines schedule risk

Every AI data center natural gas turbines plant requires a generator step-up transformer to step the generator output voltage to the on-site distribution voltage or to a grid interconnection voltage. The Wood Mackenzie Q2 2025 transformer market survey reports generator step-up transformer lead times of 144 weeks against a 2020 baseline of 6 to 12 weeks. Large power transformers run 128 weeks. The transformer shortage compounds the AI data center natural gas turbines lead time because a turbine slot that delivers in 2027 still requires a matched transformer slot, and the two slots are typically secured from different manufacturers on different timelines. Operators who lock the turbine slot but not the transformer slot extend their effective deployment window by the transformer gap.

Blocker 3: Gas pipeline coordination stretches AI data center natural gas turbines deployment

AI data center natural gas turbines require a dedicated natural gas supply, typically delivered through a new pipeline lateral or a tap on an existing interstate pipeline. New lateral construction runs 12 to 24 months from agreement to first delivery, gated by pipeline operator scheduling, Federal Energy Regulatory Commission certification for interstate facilities, and right-of-way acquisition. The supply contract economics also matter. A 200 megawatt combined-cycle AI campus running at high capacity factor consumes roughly 30 million cubic feet of natural gas per day. Securing firm transportation capacity for that load against the broader 2026 gas demand surge has tightened materially. The Interstate Natural Gas Association of America reports firm transportation tariffs in major basins climbing through 2025 and 2026.

Blocker 4: Emissions permit lead times constrain AI data center natural gas turbines siting

AI data center natural gas turbines plants above 25 megawatts trigger Prevention of Significant Deterioration permitting under the federal Clean Air Act, administered by state environmental agencies under delegation from the U.S. Environmental Protection Agency. PSD permit timelines run 12 to 24 months in non-congested air basins and 24 to 36 months in non-attainment areas, per industry analyses of 2024 and 2025 permit awards. Title V operating permits add 6 to 12 months after construction. Best Available Control Technology determinations require modeling and review. Selective catalytic reduction and oxidation catalyst systems add capital and operating cost. The emissions permitting path is the third schedule gate that compounds with turbine slot allocation and pipeline coordination.

Blocker 5: Service contract availability rations AI data center natural gas turbines operability

OEM long-term service agreements covering hot-section refurbishment, balance-of-plant maintenance, and performance guarantees are the operational backbone of any AI data center natural gas turbines plant. GE Vernova, Mitsubishi Power, and Siemens Energy all run multi-decade service agreements that bundle scheduled maintenance, hot-section parts, and performance guarantees against availability and heat rate targets. Service contract availability has tightened in parallel with new-unit slot availability, because the same hot-section production line that supplies new units also supplies refurbishment parts. The Department of Energy Office of Energy Efficiency and Renewable Energy gas turbine technology program documents the industry-wide pressure on hot-section service capacity through 2028. Service contracts are now part of the AI data center natural gas turbines procurement package.

How SAVRN compresses AI data center natural gas turbines deployment

Lever 1: Pre-positioned slot reservations compress AI data center natural gas turbines schedule

SAVRN pre-positions AI data center natural gas turbines slot reservations on the operator balance sheet ahead of specific project demand. The deposit required to secure a heavy-duty turbine slot, a generator step-up transformer slot, or a high-horsepower reciprocating engine slot is small relative to the net present value of on-time energization. Pre-positioned slots are tradeable positions. Unallocated capex authorizations are not. SAVRN’s procurement function therefore operates as a slot inventory desk, holding committed positions across the four primary turbine classes and reallocating slots to specific projects as site readiness, sovereign program demand, and contracted offtake align. The pre-positioning model converts the AI data center natural gas turbines slot shortage from a project blocker into a competitive advantage for operators with the balance sheet to play it.

Lever 2: Vertical manufacturing collapses customer-facing lead times

Intelliflex, integral to SAVRN, manufactures modular compute pods, cooling skids, generator enclosures, and switchgear assemblies at its Fort Worth, Texas facility. The vertical integration converts the largest customer-facing lead times in the AI campus stack into production schedules SAVRN controls. Enclosures, raceways, control buildings, and balance-of-plant skids that conventional EPC firms procure from multiple specialty fabricators on 30-to-50-week lead times instead run through Fort Worth on production schedules SAVRN sets. The result is a campus build cadence that pairs with the AI data center natural gas turbines slot delivery rather than waiting on it. Customer-facing months collapse to weeks because the manufacturing is internal.

Lever 3: Hybrid generation stack matches AI data center natural gas turbines class to deployment urgency

SAVRN’s hybrid generation architecture layers AI data center natural gas turbines classes against deployment urgency. Heavy-duty H-class and F-class units anchor the long-run baseload economics on campuses where slot reservations are confirmed and the schedule permits. Aeroderivative units deliver the 30-to-100 megawatt increment with shorter lead times and faster ramp characteristics that pair well with AI inference cycle peaks. High-horsepower reciprocating engines deliver the fastest-deploy increment, often serving as the first-energization tranche while heavy-duty units are commissioned. The hybrid stack therefore decouples the campus first-token date from the heaviest single-class lead time. The campus energizes against the fastest available unit and scales against the slot-secured units.

Lever 4: Closed-loop liquid cooling integrates with the AI data center natural gas turbines waste-heat envelope

SAVRN’s closed-loop liquid cooling architecture integrates with the AI data center natural gas turbines waste-heat envelope to capture combined heat and power efficiency above conventional combined-cycle alone. The integration is a tight engineering coupling that conventional EPC contractors typically treat as out of scope. SAVRN treats it as in scope. The combined system reduces parasitic load on the campus, increases effective tokens per watt across the SAVRN operating envelope, and lowers the marginal cost of compute. The closed-loop liquid cooling architecture also eliminates the water consumption pattern that has driven public scrutiny of evaporative cooled AI campuses, with on-site water usage running approximately 95 percent below evaporative baselines per SAVRN engineering specifications.

AI data center natural gas turbines regional spread across SAVRN geographies

Texas: gas pipeline density supports AI data center natural gas turbines at scale

Texas runs the densest interstate and intrastate natural gas pipeline network in the United States, with Permian and Eagle Ford production basis supporting some of the lowest delivered natural gas prices nationally. The Electric Reliability Council of Texas large-load interconnection process introduced in 2024 has further accelerated AI campus siting in the ERCOT footprint. AI data center natural gas turbines deployments in Texas therefore benefit from short pipeline tie-in distances, attractive firm transportation tariffs, and a permitting environment under the Texas Commission on Environmental Quality that has demonstrated workable timelines for PSD permits in the 12-to-18-month range for greenfield AI campus sites. SAVRN’s Fort Worth manufacturing footprint reinforces the Texas regional advantage.

California: behind-the-meter as the AI data center natural gas turbines bypass

California’s CAISO interconnection queue runs roughly 410 gigawatts with five-to-six-year typical waits, per LBNL Queued Up 2025. California Air Resources Board emissions standards apply on top of federal PSD and Title V permitting, lengthening the permit window for new AI data center natural gas turbines siting. The bypass strategy in California therefore relies on behind-the-meter generation paired with smaller turbine classes that fit within district-level permit envelopes and on coordination with sovereign-program offtake structures that justify the longer permit windows. SAVRN’s California development pursues this path. Permit envelopes, sovereign offtake, and aeroderivative units pair to produce a workable timeline despite the regulatory friction the state imposes on conventional combustion siting.

Colorado: Denver-Julesburg basin gas supports AI data center natural gas turbines siting

Colorado’s Denver-Julesburg basin gas production and the state’s mid-band PSD permit timelines under the Colorado Department of Public Health and Environment combine to produce a workable AI data center natural gas turbines siting profile. Colorado SPP-adjacent and Western Interconnection load-serving entity geographies also benefit from a public-utility commission regulatory environment that has been increasingly receptive to large-load AI campus siting. The combination favors mid-scale aeroderivative and reciprocating engine deployments, with heavy-duty units reserved for campuses where transmission interconnection is already secured. SAVRN’s Colorado development pursues this mid-scale profile, with the BTM tie sized to eliminate dependence on grid interconnection during the development window.

Nebraska: SPP and central United States AI data center natural gas turbines economics

Nebraska sits inside the Southwest Power Pool footprint and benefits from low network upgrade allocations relative to PJM, CAISO, and MISO. Nebraska also benefits from central United States gas pipeline access through the Northern Natural and REX systems. The AI data center natural gas turbines siting profile in Nebraska therefore favors larger heavy-duty deployments that can absorb the longer slot lead times against a workable network upgrade cost profile. SAVRN’s Nebraska development pursues the heavy-duty path with paired aeroderivative units as the first-energization tranche. The state’s public-power utility structure also creates a workable regulatory environment for large-load interconnection, even where the bulk of generation is behind-the-meter and the utility tie is sized for export and reliability rather than primary supply.

Panama and Barbados: LNG-fed AI data center natural gas turbines outside the United States ISO framework

Panama and Barbados operate outside the United States independent system operator framework, replacing the FERC Order 2023 cluster-study process with national grid coordination and LNG-fed generation economics. Both jurisdictions benefit from established LNG import infrastructure that can support AI data center natural gas turbines deployments at the 100-to-300 megawatt scale. The international development path also opens sovereign and multinational offtake structures that domestic operators do not have access to. SAVRN’s Panama and Barbados developments leverage these structural advantages, with aeroderivative and reciprocating engine fleets sized against LNG supply contracts and national grid coordination timelines that compare favorably to United States ISO interconnection in 2026.

Capex math: AI data center natural gas turbines per megawatt at AI scale

Path A: conventional 200 megawatt AI data center natural gas turbines procurement

A 200 megawatt AI campus procuring AI data center natural gas turbines through conventional channels in 2026 files turbine slot requests with the major OEMs at standard customer terms. F-class heavy-duty slots run 48-to-54 month lead times. Aeroderivative slots run 30-to-36 months. Generator step-up transformer slots run 144 weeks. Best Available Control Technology determinations and PSD permits add 18-to-24 months. Pipeline coordination adds 12-to-24 months. Sequenced honestly, the conventional procurement path delivers first-token operation in 2030 or 2031. Total project capex including the AI data center natural gas turbines, balance-of-plant, transmission tie, and emissions controls runs roughly $18 million to $24 million per megawatt, placing the 200 megawatt project capex at $3.6 billion to $4.8 billion.

Path B: SAVRN sovereign 200 megawatt AI data center natural gas turbines deployment

The same 200 megawatts under SAVRN sovereign procurement runs through a fundamentally different sequence. SAVRN draws AI data center natural gas turbines from pre-positioned slot inventory across heavy-duty, aeroderivative, and reciprocating engine classes. Intelliflex Fort Worth manufactures the enclosures, racks, switchgear, and cooling skids on a SAVRN-controlled production schedule. The campus interconnects to a natural gas pipeline tie rather than the bulk power grid. Emissions permitting runs in parallel with manufacturing rather than sequentially. First-token operation lands inside 6 to 12 months from authorization. Total project capex runs $9 million to $12 million per megawatt depending on the chosen geography, placing the 200 megawatt project capex at $1.8 billion to $2.4 billion. The capex delta is 40-to-55 percent. The schedule delta is three to four years.

AI data center natural gas turbines and the SAVRN BYOP doctrine

The SAVRN bring-your-own-power doctrine elevates AI data center natural gas turbines from a procurement line item to a structural pillar of the operating model. The doctrine has four pillars. First, own the generation. SAVRN deploys on-site AI data center natural gas turbines sized for the entire IT envelope, eliminating dependence on utility interconnection. Second, own the manufacturing. Intelliflex Fort Worth produces the enclosures, switchgear, cooling skids, and balance-of-plant assemblies that conventional EPC firms procure from third parties. Third, own the cooling. Closed-loop liquid cooling captures combined heat and power efficiency from the turbine waste-heat envelope. Fourth, own the schedule. Pre-positioned slot reservations convert customer-facing OEM lead times into production schedules SAVRN controls.

The four pillars compound. Each one alone collapses a category of schedule and cost risk that the conventional AI infrastructure model treats as exogenous. Together, the four pillars convert the 24-to-48-month industry standard build into the 6-to-12-month SAVRN sovereign deploy. AI data center natural gas turbines sit at the load-bearing center of this architecture because thermal generation is the only mature technology that can deliver the dispatchable, off-grid, full-IT-envelope capacity the AI campus class now requires. Renewable plus storage architectures cannot match the capacity factor or the dispatchability at the 200-to-500 megawatt AI campus scale through 2030. AI data center natural gas turbines are therefore the doctrine’s necessary load-bearing element, not a contingent procurement choice.

For the SAVRN operating model, the implication is direct. Sovereign-program buyers, hyperscale AI builders, and merchant compute developers that secure SAVRN deployment slots in 2026 will land AI capacity that ships in 2027 and 2028. Those that defer slot reservations until utility interconnection clarity arrives will discover that both the utility interconnection and the turbine slot have closed against them. The 2026 procurement window for AI data center natural gas turbines, generator step-up transformers, gas pipeline capacity, and emissions permits is now the binding operational variable. SAVRN’s pre-positioned inventory model converts that variable into a competitive advantage for the operators who recognize and act on it. The procurement decision is the deployment decision.

Frequently asked questions about AI data center natural gas turbines

How long does it take to procure AI data center natural gas turbines in 2026?

Lead times for AI data center natural gas turbines in 2026 vary by class. Heavy-duty H-class platforms run 54 to 60 months from slot reservation to shaft on floor, with slots booked through 2029 per the GE Vernova Q1 2026 earnings release. Heavy-duty F-class platforms run 48 to 54 months. Aeroderivative platforms run 30 to 36 months. High-horsepower reciprocating engines run 14 to 18 months. SAVRN’s pre-positioned slot inventory model compresses customer-facing lead times to 6 to 12 months by holding committed positions across all four classes ahead of specific project demand. The turbine slot, not the turbine price, is the binding procurement variable in 2026.

What size AI data center natural gas turbines fit a 200 megawatt campus?

A 200 megawatt AI campus can be served by AI data center natural gas turbines in three plausible configurations. One single heavy-duty F-class combined-cycle unit delivers 200-to-280 megawatts of net output. Two-to-four aeroderivative simple-cycle units in the 30-to-100 megawatt range deliver fast-deploy capacity with operational flexibility. Twenty-to-100 high-horsepower reciprocating engines in the 2-to-20 megawatt range deliver the highest deployment modularity. SAVRN’s hybrid generation stack typically layers all three classes against deployment urgency, with reciprocating engines on the fastest tranche, aeroderivative units on the second tranche, and heavy-duty units anchoring the long-run baseload economics where slot reservations are confirmed.

How much do AI data center natural gas turbines cost per megawatt installed?

Installed capex for AI data center natural gas turbines varies by class and configuration. Heavy-duty H-class combined cycle runs $700 to $1,100 per kilowatt. Heavy-duty F-class combined cycle runs $900 to $1,300 per kilowatt. Aeroderivative simple cycle runs $1,000 to $1,500 per kilowatt. High-horsepower reciprocating engine plants run $1,200 to $1,800 per kilowatt. Full campus capex including the AI data center natural gas turbines, balance-of-plant, transmission tie, emissions controls, and Intelliflex pod manufacturing runs $9 million to $12 million per megawatt under SAVRN sovereign procurement, compared to $18 million to $24 million per megawatt under conventional procurement. The cost driver is procurement model, not turbine class.

Are AI data center natural gas turbines compatible with carbon-capture retrofits?

Modern AI data center natural gas turbines are designed for compatibility with post-combustion carbon capture retrofits, with heavy-duty H-class and F-class platforms typically engineered to accommodate a downstream capture system. The U.S. Department of Energy Office of Energy Efficiency and Renewable Energy gas turbine technology program documents the design pathway. Retrofit feasibility depends on site space allocation, steam cycle integration, and CO2 transport infrastructure availability. SAVRN campus designs reserve site footprint for future carbon capture retrofit where sovereign program offtake or regulatory environment supports it. The Section 45Q tax credit and emerging state-level sequestration programs continue to shape the retrofit economics through 2028.

What permits do AI data center natural gas turbines require?

AI data center natural gas turbines plants above 25 megawatts trigger Prevention of Significant Deterioration permitting under the federal Clean Air Act, administered by state environmental agencies under delegation from the U.S. Environmental Protection Agency. Title V operating permits follow construction. Best Available Control Technology determinations require modeling. State-level air quality, water discharge, and noise permits add jurisdictional layers. Federal Energy Regulatory Commission certification applies to interstate pipeline laterals. PSD permit timelines run 12 to 24 months in non-congested air basins. SAVRN’s Texas, Colorado, and Nebraska siting strategy favors air basins with workable permit timelines, and the company runs emissions permitting in parallel with manufacturing rather than sequentially.

Why are AI data center natural gas turbines now booked through 2029?

Heavy-duty AI data center natural gas turbines are booked through 2029 because three demand vectors are pulling simultaneously against limited manufacturing capacity. First, the AI campus class has emerged as a new demand category, with 200-to-500 megawatt single-site loads filing in volume during 2024 and 2025. Second, utility resource adequacy programs are returning to natural gas as coal retirements proceed, per the NERC 2025 Long-Term Reliability Assessment. Third, industrial customers are deploying gas combined-cycle for on-site generation. The three vectors combine against a heavy-duty hot-section production footprint that does not expand inside a 24-to-36-month window. GE Vernova, Mitsubishi Power, and Siemens Energy are all running heavy-duty slot inventories at allocation status through 2029.

How does SAVRN secure AI data center natural gas turbines at scale?

SAVRN secures AI data center natural gas turbines through pre-positioned slot reservations posted on the operator balance sheet ahead of specific project demand. The procurement function operates as a slot inventory desk, holding committed positions across heavy-duty, aeroderivative, and high-horsepower reciprocating engine classes. Slots reallocate to specific projects as site readiness, sovereign program demand, and contracted offtake align. Intelliflex Fort Worth manufactures the enclosures, switchgear, and balance-of-plant components in-house, eliminating the customer-facing lead times that constrain conventional EPC contractors. The result is a 6-to-12-month customer-facing deployment timeline that the conventional procurement model cannot match in 2026.

What gas pipeline capacity do AI data center natural gas turbines require?

A 200 megawatt combined-cycle AI campus running at high capacity factor consumes roughly 30 million cubic feet of natural gas per day. A 200 megawatt simple-cycle aeroderivative campus consumes 40 to 45 million cubic feet per day. High-horsepower reciprocating engine campuses fall between those two ranges. Firm transportation capacity for AI data center natural gas turbines therefore typically requires either a dedicated pipeline lateral tied to a high-pressure transmission line or a firm interruptible blend with on-site LNG or compressed natural gas backup. SAVRN’s Texas and Colorado deployments anchor against direct pipeline ties. SAVRN’s Panama and Barbados deployments leverage LNG import infrastructure with on-site storage sized against the contracted offtake.

How do AI data center natural gas turbines compare to behind-the-meter solar plus storage?

Through 2030, AI data center natural gas turbines deliver dispatchable, full-capacity-factor power at the 200-to-500 megawatt AI campus scale that behind-the-meter solar plus battery storage cannot match. A behind-the-meter solar plus storage architecture sized to a 200 megawatt AI baseload would require roughly 1,200 to 1,800 megawatts of solar capacity paired with 8 to 16 gigawatt hours of battery storage to deliver 24-hour availability. The land footprint runs 6,000 to 10,000 acres. The capex runs significantly above thermal alternatives. AI data center natural gas turbines therefore remain the load-bearing primary generation for AI campuses through 2030, with renewables typically layered as an emissions-profile complement rather than the primary supply.

What service contracts do AI data center natural gas turbines require?

AI data center natural gas turbines require OEM long-term service agreements covering hot-section refurbishment, balance-of-plant maintenance, and performance guarantees against availability and heat rate targets. GE Vernova, Mitsubishi Power, and Siemens Energy all run multi-decade service agreements that bundle scheduled maintenance, hot-section parts, and performance guarantees. Service contract availability has tightened in parallel with new-unit slot availability through 2028. SAVRN secures service agreements at slot reservation, locking parts and labor availability ahead of the operational phase. The Department of Energy Office of Energy Efficiency and Renewable Energy gas turbine technology program documents the industry-wide pressure on hot-section service capacity through 2028.

Sources & Citations

Every quantitative claim in this piece traces to a named, verified primary source. URLs verified at time of publication. The full audit-grade citation record, with claim-by-claim source mapping and “cite this article” snippets, is maintained on the dedicated SAVRN sources page for this piece.

Primary research and forecasts cited in this AI data center natural gas turbines brief

- GE Vernova, Q1 2026 Earnings Release. Source for: $30+ billion gas power orders during 2025, heavy-duty turbine production slots booked through 2029, Power segment backlog at record level.

- Mitsubishi Power, Power Sector 2025 Outlook. Source for: M501JAC and M701JAC H-class platforms moved to allocated production, selective acceptance for new heavy-duty orders.

- Siemens Energy, Annual Report 2025. Source for: double-digit growth in heavy-duty gas turbine orders, AI data center demand named as leading source of incremental commitments, multi-year delivery backlog.

- Wood Mackenzie, Q2 2025 Transformer Market Survey. Source for: generator step-up transformer lead times of 144 weeks, large power transformer lead times of 128 weeks, 30 percent supply deficit through 2027.

- U.S. Energy Information Administration, Annual Energy Outlook 2025. Source for: natural gas capacity additions above 130 gigawatts through 2050 with near-term surge in 2026-2030 window.

Standards, regulatory, and policy references for AI data center natural gas turbines

- North American Electric Reliability Corporation, 2025 Long-Term Reliability Assessment. Source for: natural gas dominant share of incremental dispatchable capacity, coal retirement timing.

- International Energy Agency, Energy and AI, 2025. Source for: 2030 global data center electricity demand at 945 terawatt-hours, 12 percent compound annual growth rate.

- Lawrence Berkeley National Laboratory, Queued Up: 2025 Edition. Source for: 2,060 gigawatts in active interconnection queue, 5-year typical wait, CAISO 410 GW queue depth.

- Lawrence Berkeley National Laboratory, 2024 United States Data Center Energy Usage Report (Shehabi et al.). Source for: 2028 data center electricity demand at 6.7 to 12.0 percent of total United States electricity.

- United States Department of Energy Office of Energy Efficiency and Renewable Energy, Gas Turbine Technology Program. Source for: industry-wide hot-section service capacity pressure through 2028, carbon-capture retrofit design pathway.

View the full audit record for this AI data center natural gas turbines brief →

Continue exploring AI data center natural gas turbines and the SAVRN doctrine

The AI data center natural gas turbines decision sits inside the broader SAVRN sovereign infrastructure doctrine. Companion analyses across the SAVRN doctrine series take the topic into adjacent procurement decisions. The behind-the-meter AI power brief documents the bypass economics that AI data center natural gas turbines enable at the campus level. The AI data center grid interconnection brief writes the 2026 queue math that is driving operators away from utility tie procurement. The AI data center supply chain brief covers the cross-equipment lead time landscape including transformers, switchgear, and reciprocating engines.

For procurement and capex framing, the AI data center construction cost brief writes the bill-of-materials math against AI rack densities, and the tokens per watt per dollar brief writes the operating-economics metric that connects turbine heat rate to AI inference unit economics. The liquid cooling for AI brief documents the closed-loop architecture that integrates with the AI data center natural gas turbines waste-heat envelope. The AI infrastructure deployment timeline brief documents the 6-to-12-month sovereign deploy that AI data center natural gas turbines and pre-positioned slot reservations make operational.

The full doctrine is anchored at sovereign AI infrastructure, the foundational brief that frames the SAVRN operating model. The SAVRN doctrine page collects every pillar in the series. For operator engagement, the SAVRN infrastructure assessment form connects qualifying buyers to a tailored deployment proposal. SAVRN active geographies under development: California, Texas, Colorado, Nebraska, Panama, and Barbados. Manufacturing footprint: Intelliflex, Fort Worth, Texas. AI data center natural gas turbines slot inventory: heavy-duty H-class, heavy-duty F-class, aeroderivative, high-horsepower reciprocating engines, with generator step-up transformer and switchgear slots paired.