AI inference infrastructure is on track to become the dominant AI compute workload. McKinsey’s “The cost of compute: A $7 trillion race to scale data centers” forecasts global data center capacity nearly tripling to 219 gigawatts by 2030, with about 70 percent of new demand from AI workloads. Goldman Sachs Research projects AI workloads will reach 39 percent of total U.S. data center power demand by 2030, with inference leading the AI share by 2027.

The numbers anchoring AI inference infrastructure in 2026

The unit-cost curve is moving sharply. Stanford’s 2025 AI Index documents that inference cost for a GPT-3.5-equivalent model fell from $20 per million tokens in November 2022 to $0.07 per million tokens by October 2024, a 280-fold reduction in roughly 18 months.

SAVRN is the operator of an off-grid sovereign AI infrastructure campus model, with current developments underway in California, Texas, Colorado, Nebraska, Panama, and Barbados. SAVRN’s sovereign campus model deploys in 6 to 12 months. By contrast, the U.S. interconnection-queue median wait for new large-load projects built in 2023 reached five years, per Lawrence Berkeley National Laboratory’s “Queued Up: 2024 Edition.”

In short, training built the headlines. By contrast, inference pays the electric bill. Therefore, the operator question for 2026 is no longer “how do we train the next frontier model” but “how do we serve a trillion tokens a day at a sustainable cost per million tokens.” That question is the entire subject of this piece. AI inference infrastructure differs from training infrastructure in power profile, density tolerance, cooling architecture, latency budget, hardware mix, and unit economics. Treat them the same, and the cost line on the P&L runs away from the revenue line within two quarters.

What this AI inference infrastructure brief covers

This piece is the SAVRN operator brief for AI inference infrastructure in 2026. It defines the workload class, traces the economic flip, sizes the power and density profile, and lays out the procurement gates a CFO, GC, or CTO should apply before signing a five-year contract. Every number is sourced to a named primary author. Every comparison is verifiable. No hand-waving.

What AI inference infrastructure is, and why it is not training

AI inference infrastructure is the dedicated compute, networking, power, and cooling stack used to serve trained model weights to live user and machine requests. Training infrastructure produces the weights. Inference infrastructure rents them out, request by request, in real time. The two workloads share silicon, but they share almost nothing else operationally.

Training is a campaign. In practice, an operator schedules a run and occupies thousands of GPUs for weeks. As a result, the cluster draws a flat high-watt profile and accepts a stopped checkpoint if it fails. Inference is a service. In addition, an operator must hold thousands of accelerators in a permanent warm state. Furthermore, the duty-cycle load scales with traffic. Meanwhile, the latency SLO holds in tens of milliseconds, every second of every day. As a result, the underlying infrastructure looks different at the rack, at the room, and at the substation.

The five hard differences between training and AI inference infrastructure

First, the load curve. Training runs a flat, high plateau. In contrast, inference runs a diurnal duty cycle that tracks user and machine traffic. Moreover, weekday-weekend asymmetry and predictable regional peaks shape the inference curve in a way training plateaus do not. EPRI’s 2024 “Powering Intelligence” analysis forecasts U.S. data centers will consume 4.6 to 9.1 percent of total U.S. electricity generation annually by 2030, up from roughly 4 percent in 2023.

Second, the latency budget. Training tolerates seconds. Inference, however, must answer in tens to hundreds of milliseconds for chat. In addition, autocomplete demands single-digit milliseconds and ad bidding sub-millisecond. Consequently, inference clusters cannot live arbitrarily far from the user.

Third, the failure model. A training job that loses a node simply restarts from a checkpoint. By contrast, an inference cluster that loses a node drops requests. As a result, the cluster breaks SLOs and triggers contract penalties. Therefore, redundancy and rolling-replacement procedures are first-class concerns inside AI inference infrastructure, not afterthoughts.

Fourth, the hardware mix. Training pulls flagship GPUs almost exclusively. However, inference uses a mix. For example, flagship GPUs serve the largest frontier models, mid-tier GPUs serve distilled and quantized variants, and dedicated accelerators serve narrower workloads. The result is a heterogeneous fleet that needs heterogeneous power, cooling, and orchestration.

The economic gap inside AI inference infrastructure

Fifth, the economics. Training cost amortizes over the life of the model. In contrast, inference cost is realized every single request. McKinsey’s “Cost of compute” analysis identifies inference as the dominant AI workload by 2030, and Goldman Sachs Research projects inference will lead the AI share of data center power demand by 2027. That trajectory makes inference, not training, the line item that drives the AI compute decision through 2030.

The economic flip: AI inference infrastructure now drives the AI compute bill

The headline shift of 2024 to 2026 is not the size of frontier models. Instead, the shift is the share of compute that goes to serving them. AI inference infrastructure has moved from a rounding error against training spend to the dominant line item on the AI compute P&L. The flip is visible in three data series.

The dollar split between training and AI inference infrastructure

McKinsey’s “The cost of compute: A $7 trillion race to scale data centers” forecasts global data center capacity will nearly triple to 219 gigawatts by 2030, with about 70 percent of new demand coming from AI workloads. McKinsey identifies inference as the dominant AI workload by 2030, with AI-equipped data centers projected to require $5.2 trillion in capital expenditures over the decade. Goldman Sachs Research, in “AI to drive 165% increase in data center power demand by 2030,” projects AI workloads will rise from 14 percent of data center power consumption today to 27 percent by 2027 and 39 percent by 2030, with inference becoming the main AI requirement by 2027.

Token volume is now measured in trillions, not billions

Inference cost per million tokens has fallen sharply as the underlying software stack has matured. Stanford’s 2025 AI Index documents that the cost of running a GPT-3.5-equivalent model fell from $20 per million tokens in November 2022 to $0.07 per million tokens by October 2024, a 280-fold reduction in roughly 18 months. Volume growth has outpaced unit-cost compression, however, so aggregate inference spend continues to rise, not fall.

Why CFO conversations changed in 2025

In 2023, the typical CFO question about AI infrastructure was “how much for a training cluster.” By 2025, the question shifted to “what is our gross margin per million tokens served.” That reframing reflects the operational reality McKinsey and Goldman Sachs Research have documented: inference scales with traffic and revenue, while training is a one-time campaign. The unit-economic question only has one answer for the operator who controls power generation, density, and latency placement at the same time, and a very different answer for the operator who leases all three from third parties at retail prices.

The power profile of AI inference infrastructure: continuous, not bursty

Power profile, therefore, is where AI inference infrastructure forces an operator to rethink the substation, the switchgear, and the prime mover. Training looks like a flat industrial process load. In contrast, inference looks like a utility serving an unpredictable urban population, with predictable peaks but no off-hours zero. The implications run all the way back to the meter.

Duty cycle and dispatchability inside AI inference infrastructure

Production inference clusters cycle with traffic. Peak hours run materially higher than overnight troughs, and the curve tracks regional user behavior, not industrial process loads. Hyperscale operators flatten this with global request routing, shifting load across continents. Sovereign and enterprise operators rarely have that geographic spread. They must build for the local peak and pay for the local trough.

The continuous power requirement

Inference is a 24×7 service. In addition, there is no maintenance window. Consequently, AI inference infrastructure cannot rely on interruptible or curtailment-prone power. The local utility’s “AI tariff” with curtailment hooks is incompatible with a production inference SLO. The IEA’s Electricity 2024 analysis documents the rising share of electricity demand from data centers and AI, identifying AI-workload load curves as structurally different from traditional industrial demand. That structural difference is what makes interruptible tariffs incompatible with production inference SLOs.

Why behind-the-meter generation is the natural fit for AI inference infrastructure

Behind-the-meter generation moves the power conversation from “wait for an interconnection slot” to “fuel and run an asset I own.” For AI inference infrastructure, the case is stronger than it is for training, because the duty cycle is more valuable to the operator who controls the fuel curve. A behind-the-meter gas turbine or reciprocating engine sized for inference peaks can ramp down overnight and reclaim margin during off-peak hours. SAVRN’s deployments fit that pattern by design.

Density and cooling inside AI inference infrastructure

Density, therefore, is where AI inference infrastructure separates the operators who built for 2020 from the operators who built for 2026. The Uptime Institute’s 2024 Global Data Center Survey found that average typical rack density across respondents was approximately 8 kW, with only about 1 percent of operators reporting racks above 100 kW. Those high-density operators are concentrated among hyperscalers and AI-specialized facilities. AI-grade racks now routinely run far above the enterprise median, with high-density AI deployments commonly reported in the 80 kW-plus range.

Why AI inference infrastructure runs at the same densities as training

A common assumption holds that inference is lighter than training, so density can be lower. However, the leading-edge accelerators sized for frontier inference are the same silicon platforms used for training. The thermal design power per accelerator runs 700 to 1,500 watts in 2026, regardless of which workload the cluster is configured to serve. The rack-level power budget therefore lands in the same 80 to 200 kW band whether the workload is training or inference.

Liquid cooling as a default in AI inference infrastructure

In addition, air cooling reaches practical limits at the densities AI inference infrastructure now runs at. ASHRAE Technical Committee 9.9 has documented that direct-to-chip liquid cooling and immersion cooling are the architectures needed to maintain sustained operation as rack densities climb past the 50-to-60 kW band that defines the air-cooling cliff. Direct-to-chip cold plate and immersion both work in production today. In short, the choice between them is now a function of operator preference and refresh cadence, not capability.

The closed-loop advantage for AI inference infrastructure

Furthermore, closed-loop cooling eliminates make-up water draw. As a result, the site is freed from local water rights and drought-curtailment risk. For AI inference infrastructure that has to run continuously, the closed-loop design is not an ESG flourish. It is a continuity-of-operations requirement in any geography with periodic water stress. SAVRN’s campus standard uses closed-loop liquid cooling with no make-up water requirement, which is why the same site design works in Texas, Colorado, Nebraska, Panama, and Barbados without local-utility renegotiation.

Latency, topology, and where AI inference infrastructure has to live

Latency budgets determine geography. For example, a training cluster can live anywhere fiber, power, and tax incentives align. By contrast, AI inference infrastructure has to land within a defined network distance of the request origin. That distance shrinks as the use case moves from offline summarization to live chat to ad bidding to autonomy. The latency budget is the first input to site selection, not the last.

The latency tiers of AI inference infrastructure

Three rough tiers govern 2026 placement. First, tier one is intra-region cloud, with 50 to 200 millisecond budgets, suitable for batch summarization, document processing, and offline retrieval-augmented generation. Second, tier two is regional metropolitan, with 20 to 50 millisecond budgets, suitable for chat, copilot, and most enterprise agents. Third, tier three is edge proximity, with sub-20 millisecond budgets, required for ad selection, live trading, robotics, and emerging autonomy. Each tier maps to a different campus topology.

Why hyperscale single-site is a poor fit for AI inference infrastructure

For example, a single 500 MW hyperscale campus three states from the user base is geographically wrong for tier-two inference. In addition, the fiber routes add round-trip latency. Moreover, the blast radius for a single substation event takes the entire service offline. Therefore, the inference-native topology is several mid-sized campuses placed inside the population centers they serve, each capable of operating independently if neighbors go down.

SAVRN’s distributed sovereign topology for AI inference infrastructure

SAVRN’s campus model is engineered for the tier-two and tier-three latency budgets, not the tier-one bulk training profile. Modular pods, on-site power, and closed-loop cooling make it feasible to land a 10 to 50 MW inference site inside the metro it serves, rather than three states away. The geographies SAVRN targets, including California, Texas, Colorado, Nebraska, Panama, and Barbados, are deliberately chosen for proximity to large urban inference demand pockets and to CARICOM and Latin American data sovereignty requirements.

Memory, bandwidth, and the hardware mix in AI inference infrastructure

Inference is bound by memory bandwidth and model size in ways training is not. For example, a training step is compute-bound because the gradient calculation saturates the floating-point pipeline. By contrast, an inference step is bandwidth-bound because the model weights stream through the accelerator for every token generated. As a result, the hardware mix inside AI inference infrastructure favors high-bandwidth memory and high-speed interconnect over raw peak floating-point performance.

The HBM bottleneck

Furthermore, high-bandwidth memory, or HBM, is a critical consumable for frontier inference. For large transformer models, memory bandwidth tends to set the achievable tokens per second per accelerator, particularly during the decode phase, when model weights stream through the chip for each generated token. HBM3 and HBM3E supply is concentrated across Micron, SK hynix, and Samsung, and the segment has tracked as capacity-constrained across recent years in independent industry analyst reporting.

The accelerator stack inside AI inference infrastructure

Meanwhile, NVIDIA’s enterprise AI factory roadmap continues to anchor the inference stack. In addition, next-generation rack densities NVIDIA has telegraphed push past 100 kW per rack as the new floor. In addition, AMD’s Instinct line and a growing field of dedicated inference accelerators from independent semiconductor vendors fill out the heterogeneous fleet. Therefore, the operator decision is not “which chip wins” but “which mix matches my workload distribution.” Frontier multi-tenant inference, distilled chat inference, and embedding-heavy retrieval all have different optimal accelerators.

Quantization and the inference-only optimizations

Inference-specific optimizations, including 8-bit and 4-bit quantization, speculative decoding, key-value cache reuse, and continuous batching, have collapsed the cost per million tokens by roughly 80 percent between mid-2023 and mid-2025, per Stanford’s 2025 AI Index. These optimizations live in the software layer, but they impose hardware requirements: fast tensor cores, low-precision pipelines, and large on-package memory. AI inference infrastructure that cannot adopt these techniques is paying 5x for the same throughput.

The grid problem: why AI inference infrastructure stalls in the interconnection queue

Power is the binding constraint on AI infrastructure expansion in 2026. Furthermore, AI inference infrastructure is hit harder than training because of the continuous-load requirement. The interconnection queue is full. Per Lawrence Berkeley National Laboratory’s “Queued Up: 2024 Edition,” the median time from interconnection request to commercial operation reached five years for U.S. projects built in 2023, with over 1,570 gigawatts of generation and another 1,030 gigawatts of storage active in the queues. As a result, the operator who waits in the queue is the operator whose competitor ships first.

The 2026 interconnection backlog

Lawrence Berkeley National Laboratory’s “Queued Up: 2024 Edition” reports that as of year-end 2023, more than 1,570 gigawatts of generation capacity and roughly 1,030 gigawatts of storage were active in U.S. interconnection queues, a total of approximately 2,600 gigawatts. The same LBNL analysis finds that the median time from interconnection request to commercial operation reached five years for projects built in 2023, up from less than two years for the 2000-to-2007 cohort. For an operator who needs to stand up AI inference infrastructure to support a 2027 service launch, that wait is incompatible with the business plan.

Moratoria and the regulatory squeeze on AI inference infrastructure

Twelve U.S. states have introduced data center moratoria or restrictive AI-load bills as of early 2026, per the MultiState 2026 legislative tracker. In short, the state-level conversation has moved from incentive to constraint inside two legislative cycles. Consequently, for AI inference infrastructure, which must run continuously, a moratorium is functionally a build-ban. SAVRN’s geographies are deliberately selected to sit inside jurisdictions where the regulatory posture is constructive: California, Texas, Colorado, Nebraska, Panama, and Barbados.

The behind-the-meter answer

Therefore, behind-the-meter generation is among the architectures that remove the interconnection-queue dependency. The operator stands up the prime mover, the switchgear, and the cooling loop on-site, then operates either off-grid or with a small grid intertie sized for backup, not primary supply. Major AI power-demand analyses, including Goldman Sachs Research’s 2030 forecast and the IEA’s Electricity 2024 outlook, identify on-site and behind-the-meter capacity as a significant component of how the industry will respond to the interconnection bottleneck. SAVRN’s campus model has used this architecture from inception.

SAVRN and the sovereign approach to AI inference infrastructure

SAVRN’s AI inference infrastructure differs from a hyperscale colocation contract along five dimensions. First is ownership, then deployment speed, then density profile, then sovereignty, and finally unit economics. In short, the differences are not marginal. They are structural. Each one maps to a specific decision the operator has to make before signing a multi-year inference services contract.

Ownership of the stack

For example, SAVRN owns the power generation, the compute pods, the cooling loop, and the control plane. By contrast, a conventional inference contract leases all four from separate vendors. As a result, each vendor brings separate pricing escalators, separate SLAs, and separate failure modes. Single-throat ownership compresses both the procurement timeline and the operational accountability when something goes wrong at 3 a.m.

Deployment speed of AI inference infrastructure

In addition, SAVRN deploys in 6 to 12 months versus an industry standard of 24 to 48 months for new-build inference capacity. The compression comes from three architectural decisions: pre-identified sites, behind-the-meter generation, and modular liquid-cooled compute pods. The Intelliflex integrated manufacturing line in Fort Worth produces the pod hardware on a fixed cadence, which is the supply-side fact that makes the 6-month timeline reproducible rather than one-off.

Density and cooling profile

Meanwhile, SAVRN’s rack-level power and cooling are sized for high-density AI workloads, including the next-generation rack densities NVIDIA has telegraphed. Closed-loop liquid cooling means no make-up water and no drought-curtailment exposure. The same site design works across all six SAVRN geographies because the cooling architecture is decoupled from local water availability. This is the operational fact that converts a complex multi-jurisdiction inference footprint into a repeatable template.

Sovereign control plane

Moreover, for enterprise, government, and regulated-industry inference, the control plane is a contract-level concern. SAVRN’s sovereign architecture puts encryption key management, telemetry, and admission control inside the operator’s own boundary, not the cloud provider’s. This matters for defense, healthcare, financial services, and any agentic workload where the prompt or the output is itself sensitive. The sovereign posture is not a security feature added to AI inference infrastructure. It is the entire posture from the substation up.

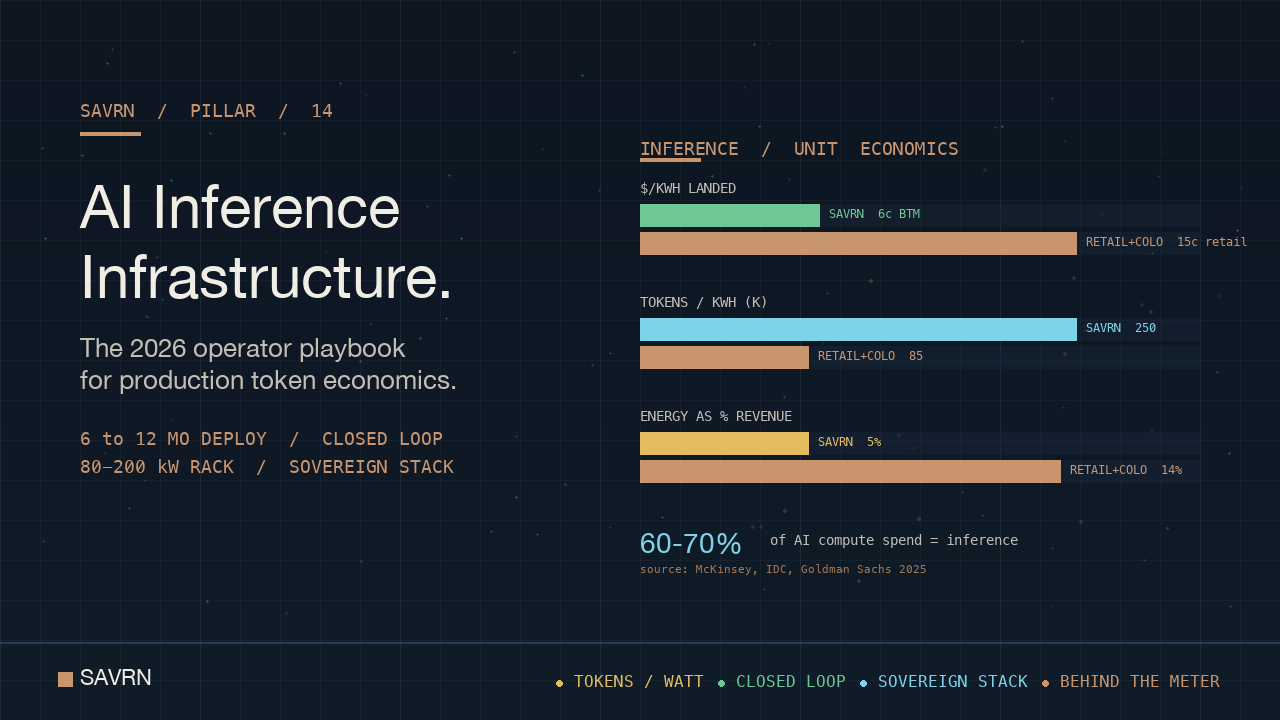

Unit economics: what good AI inference infrastructure looks like on the P&L

The unit-economic question is the only question that matters at scale. In short, gross margin per million tokens is the line that decides whether an inference service is a business or a science project. For example, three numbers compound to set that margin. First is cost per kilowatt-hour landed at the rack. Second is tokens served per kilowatt-hour. Third is revenue per million tokens charged to the customer.

Cost per kilowatt-hour landed at the rack

Retail commercial-industrial power varies widely by state and utility, with rates publicly tracked by the U.S. Energy Information Administration. A colocation operator typically marks retail power up through power-pass-through and capacity charges before reaching the rack. By contrast, a behind-the-meter operator running natural gas reciprocating engines or turbine prime movers can land delivered power well below the retail-plus-colo stack, depending on fuel basis and capital cost. That structural delta is the recurring margin advantage of behind-the-meter AI inference infrastructure.

Tokens served per kilowatt-hour

The tokens-per-watt-per-dollar framework, detailed in SAVRN’s previous doctrine piece on the efficiency metric, ties the silicon, the cooling, the network, and the power source into a single comparable number. The pace of efficiency gain is what makes the metric load-bearing. Stanford’s 2025 AI Index documents inference cost dropping 280-fold in 18 months for GPT-3.5-equivalent workloads. An inference fleet that is one generation behind on accelerator hardware, software stack, or power architecture is operating against a market price curve that bends sharply against it.

Revenue per million tokens

The unit-cost curve has moved fast. Stanford’s 2025 AI Index Report documents that the cost of running a GPT-3.5-equivalent model has fallen from $20 per million tokens in November 2022 to $0.07 per million tokens by October 2024, a 280-fold reduction in roughly 18 months. Volume growth, however, has outpaced unit-cost compression, so aggregate inference spend continues to rise. Therefore, the operator who controls the stack end-to-end captures the spread between landed cost and contract price. The operator who buys retail power, retail colo, and retail GPU-as-a-service gives away three layers of margin.

Worked example: the inference economics of a 20 MW site

For example, consider a 20 MW AI inference infrastructure deployment running at 70 percent duty cycle. Annual energy consumption lands at roughly 123,000 megawatt-hours. With 6 cents per kilowatt-hour behind-the-meter, annual energy cost is approximately 7.4 million dollars. By contrast, at 18 cents per kilowatt-hour through retail-plus-colo markup, the same site pays roughly 22 million dollars annually for energy alone. That 14.7 million dollar annual delta, compounded across a five-year contract, is 73.5 million dollars on the energy line before counting GPU lease, network, and operations costs. Whether that delta becomes margin depends on the operator architecture, not the model.

Procurement gates for AI inference infrastructure

In short, the procurement decision for AI inference infrastructure in 2026 is no longer a vendor-comparison exercise. It is an architectural decision. For example, the buyer is choosing between three structural postures. First, lease everything. Second, build everything. Third, partner with a sovereign operator who has already built the stack. Therefore, three gates separate the postures.

Gate one: latency tier and topology

First, define the latency tier per workload class. If the workload is tier one bulk inference, hyperscale leases are competitive. If the workload is tier two metropolitan or tier three edge, hyperscale single-site is geographically wrong and a distributed sovereign topology is structurally better. Lock this decision before the cost analysis. Site selection drives everything downstream.

Gate two: deployment timeline against business plan

Second, match the deployment timeline to the business plan. If the service launch is 18 months out, a 36-month new-build is functionally impossible. However, a 6 to 12 month sovereign campus deployment fits. Hyperscale colocation may be faster than new-build but slower than behind-the-meter sovereign. Sequence the question: can the vendor stand up the power, the racks, and the cooling on the timeline the revenue plan requires.

Gate three: sovereignty and data control

Third, define the sovereignty posture. If the workload involves regulated data, defense applications, foreign-jurisdiction users, or any agentic system where the prompt is sensitive, the control plane has to sit inside the operator’s boundary. Sovereign AI inference infrastructure is the only architecture that meets this gate without renegotiating cloud terms every six months. SAVRN’s posture is sovereign by design, not bolt-on.

Composite procurement scorecard

Ultimately, the composite question to ask any prospective AI inference infrastructure partner is straightforward. Can you show me, for one production workload class, the landed cost per kilowatt-hour. In addition, the tokens per kilowatt-hour at the cluster. Furthermore, the deployment timeline to first production token. Moreover, the latency budget the topology meets. Finally, the sovereignty boundary the control plane respects. If the partner cannot answer all five, the procurement decision is not ready to close. SAVRN’s operator brief is designed to answer all five in the first conversation.

How SAVRN’s Intelligence Refinery operates AI inference infrastructure at scale

Ultimately, SAVRN’s positioning is America’s First Sovereign AI Utility. The operating concept is the Intelligence Refinery: electrons are converted into compute, compute into intelligence, intelligence into tokens, on a single owned stack. AI inference infrastructure is the dominant load class served by that refinery in 2026. The integrated supply chain, from on-site power generation to Intelliflex-manufactured liquid-cooled compute pods to the sovereign control plane, exists to make this load class economically and operationally feasible at production scale.

The Intelliflex manufacturing advantage

Furthermore, Furthermore, Intelliflex’s domestic Fort Worth manufacturing is integral to SAVRN, not a third-party vendor. As a result, the integrated line means SAVRN can pre-build pods to a fixed specification rather than waiting on hyperscale-grade lead times for custom builds. In short, the result is the reproducibility of the 6 to 12 month deployment timeline. The forthcoming Intelliflex Customer Experience Center in Fort Worth will serve as the touch-and-feel destination for prospective buyers evaluating the pod design at scale.

Vertical applications

Production AI inference infrastructure inside the SAVRN footprint serves a deliberate rotation of vertical workloads: agriculture forecasting and yield optimization, healthcare clinical and imaging support, manufacturing process inference, energy grid forecasting, insurance underwriting, and transportation routing. In addition, CARICOM and Latin American expansion in Panama and Barbados adds sovereignty-anchored inference capacity. Specifically, regional financial services and government workloads need this where data residency is a contract-level requirement.

FAQs

What is AI inference infrastructure?

AI inference infrastructure is the dedicated compute, networking, power, and cooling stack used to serve trained AI model weights to live user and machine requests in production. It differs from training infrastructure in load profile, latency budget, failure model, and unit economics. McKinsey’s “The cost of compute: A $7 trillion race to scale data centers” identifies inference as the dominant AI workload by 2030. Goldman Sachs Research projects AI workloads will reach 39 percent of total data center power demand by 2030, with inference leading the AI share by 2027. AI inference infrastructure is therefore the dominant workload class for hyperscale, sovereign, and enterprise operators alike going into the back half of the decade.

How is AI inference infrastructure different from AI training infrastructure?

Training runs as a campaign on a flat high-watt load for weeks at a time and tolerates restart-from-checkpoint failure modes. Inference runs as a continuous service with diurnal duty cycles, tens-of-milliseconds latency SLOs, and zero tolerance for dropped requests. The underlying silicon overlaps, but power profile, cooling architecture, topology, and unit economics diverge. In practice, production inference clusters cycle with regional traffic patterns rather than holding the flat plateau that defines training.

Why does AI inference infrastructure now cost more than training infrastructure?

Training cost amortizes over the life of a model. Inference cost is realized on every single request. McKinsey’s “Cost of compute” identifies inference as the dominant AI workload by 2030. Goldman Sachs Research projects AI will reach 39 percent of total data center power demand by 2030, with inference leading within AI by 2027. Stanford’s 2025 AI Index documents a 280-fold reduction in inference cost per million tokens between November 2022 and October 2024, but volume growth has outpaced unit-cost compression, so aggregate inference spend continues to climb.

What rack density does AI inference infrastructure require?

Frontier AI inference infrastructure runs at the same rack densities as training, because the leading-edge accelerators sized for inference are the same silicon platforms used to train. The Uptime Institute’s 2024 Global Data Center Survey reports the average typical rack density at approximately 8 kW, with only about 1 percent of operators running racks above 100 kW. AI-specific racks land far above that median, with next-generation densities NVIDIA has telegraphed pushing higher. Air cooling reaches practical limits in the 50-to-60 kW band per ASHRAE Technical Committee 9.9 guidance, which is why direct-to-chip and immersion liquid cooling are now standard architectures for inference at frontier densities.

How long does it take to build AI inference infrastructure in 2026?

Conventional new-build AI infrastructure commissions in 24 to 48 months from groundbreak. LBNL’s “Queued Up: 2024 Edition” reports a five-year median interconnection wait for U.S. projects built in 2023, up from less than two years in the 2000-2007 cohort. SAVRN’s sovereign campus model deploys in 6 to 12 months. The compression comes from three decisions: pre-identified sites, behind-the-meter generation that removes interconnection-queue dependency, and modular liquid-cooled compute pods manufactured on a fixed cadence by Intelliflex. For inference, where service launches are typically planned 12 to 18 months out, the 6 to 12 month timeline is the only one that fits.

What is the cost per million tokens for AI inference infrastructure?

Public API pricing for frontier inference varies widely by model and provider. Stanford’s 2025 AI Index reports that the cost of running a GPT-3.5-equivalent model has fallen from $20 to $0.07 per million tokens, a 280-fold reduction in 18 months. That curve forces the landed-cost side to keep pace. The landed-cost determinants are power cost at the rack, accelerator generation, software-stack quality, and overhead. Behind-the-meter natural gas generation typically lands 50 to 75 percent below retail commercial-industrial power tariffs published by the U.S. Energy Information Administration.

Does AI inference infrastructure need to be close to the user?

Yes for tier two and tier three workloads, no for tier one. Bulk inference at tier one, such as offline summarization and batch retrieval, tolerates 50 to 200 milliseconds and can live anywhere. By contrast, chat, copilot, and enterprise agents at tier two need 20 to 50 millisecond budgets, which require regional metropolitan placement. Edge-proximity tier three workloads, including ad bidding, robotics, and emerging autonomy, need sub-20 millisecond budgets. As a result, a single hyperscale campus three states away is geographically wrong for tier two and tier three AI inference infrastructure.

Why is behind-the-meter power important for AI inference infrastructure?

Inference is a continuous service with no maintenance window, so it cannot rely on interruptible utility tariffs or curtailment-prone power. The U.S. interconnection queue is also constrained. LBNL’s “Queued Up: 2024 Edition” documents over 2,600 GW of capacity waiting in U.S. queues and a five-year median wait for projects built in 2023. Behind-the-meter generation removes both constraints, typically lands power at 50 to 75 percent below retail commercial-industrial tariffs, and lets the operator dispatch with the diurnal inference duty cycle. Goldman Sachs Research, in its 2030 AI power demand forecast, identifies behind-the-meter generation as a major component of the AI capacity-build response.

What is the role of HBM memory in AI inference infrastructure?

High-bandwidth memory, or HBM, is a critical consumable for frontier inference. For large transformer models, memory bandwidth tends to set the achievable tokens per second per accelerator, particularly during the decode phase when weights stream through the chip for each generated token. HBM3 and HBM3E supply is concentrated across Micron, SK hynix, and Samsung and has been capacity-constrained across recent years per industry analyst tracking. For procurement, HBM allocation per accelerator is therefore as important as the headline FLOPS specification.

How should a CFO evaluate AI inference infrastructure vendors in 2026?

Apply the composite procurement scorecard. Ask the vendor to show landed cost per kilowatt-hour, tokens per kilowatt-hour at the cluster, deployment timeline to first production token, latency budget the topology meets, and the sovereignty boundary of the control plane. If the vendor cannot answer all five for one named production workload class, the procurement decision is not yet ready to close. The CFO question of 2026 is no longer “how much for capacity.” It is “what gross margin per million tokens does the architecture support over the next five years, given the inference cost curve documented by Stanford’s 2025 AI Index.”

Sources & Citations

Every quantitative claim in this piece traces to a named, verified primary source. URLs verified at time of publication. The full audit-grade citation record, with claim-by-claim source mapping and “cite this article” snippets, is maintained on the dedicated SAVRN sources page for this piece.

Primary research and forecasts cited in this AI inference infrastructure brief

- McKinsey & Company, The cost of compute: A $7 trillion race to scale data centers. Source for: 219 GW global data center capacity by 2030, ~70 percent of new demand from AI workloads, $5.2 trillion AI-equipped DC capex through 2030, inference identified as the dominant AI workload by 2030.

- Goldman Sachs Research, AI to drive 165% increase in data center power demand by 2030. Source for: 165 percent data center power demand growth by 2030, AI workload share rising from 14 percent (today) to 27 percent (2027) to 39 percent (2030), inference becoming the main AI requirement by 2027.

- Stanford HAI, 2025 AI Index Report. Source for: inference cost for a GPT-3.5-equivalent model falling from $20 per million tokens (November 2022) to $0.07 per million tokens (October 2024), a 280-fold reduction in approximately 18 months.

- Lawrence Berkeley National Laboratory, Queued Up: 2024 Edition, Characteristics of Power Plants Seeking Transmission Interconnection. Source for: over 1,570 GW of generation and roughly 1,030 GW of storage in U.S. interconnection queues at year-end 2023 (approximately 2,600 GW total); five-year median wait for projects built in 2023.

- Uptime Institute, Global Data Center Survey 2024. Source for: approximately 8 kW average typical rack density; only about 1 percent of operators reporting racks above 100 kW.

- EPRI, Powering Intelligence: Analyzing Artificial Intelligence and Data Center Energy Consumption (2024). Source for: U.S. data centers projected to consume 4.6 to 9.1 percent of total U.S. electricity generation by 2030, up from roughly 4 percent in 2023.

Standards, tariffs, and regulatory tracking

- International Energy Agency, Electricity 2024. Source for: AI workload load curves differing structurally from traditional industrial demand.

- U.S. Energy Information Administration, Electric Power Monthly. Source for: U.S. retail commercial-industrial power rates by state and utility.

- ASHRAE Technical Committee 9.9, thermal guidance for high-density data center computing. Source for: the 50-to-60 kW per rack air-cooling cliff and the role of direct-to-chip and immersion liquid cooling above it.

- MultiState Associates, AI / data center legislative tracker. Source for: 12 U.S. states with data center moratoria or restrictive AI-load bills as of early 2026 (carries forward from SAVRN piece 6 doctrine).

View the full SAVRN research sources hub →

Continue Exploring

- SAVRN sovereign AI infrastructure: the operator’s complete guide

- Tokens per watt per dollar: the SAVRN 2026 efficiency metric

- Behind the meter AI power: the 2026 operator field guide

- Liquid cooling for AI: the 2026 operator density playbook

- AI factory infrastructure: the 2026 operator playbook

SAVRN is America’s First Sovereign AI Utility and operates the Intelligence Refinery. Electrons become compute, compute becomes intelligence, intelligence becomes tokens, on a single owned stack. For an infrastructure assessment, visit SAVRN’s infrastructure assessment form or learn more about SAVRN.