Behind the meter AI power is the architectural decision that finally lets owners match generation to the build cadence of a modern AI campus. The phrase describes any electricity asset sited inside a customer’s premises, ahead of the utility revenue meter, and dispatched directly to load. As a result, the operator owns the watt before the utility owns the wire. Conventional grid-connected AI data centers wait roughly 5 years for a high-voltage interconnection, per Lawrence Berkeley National Laboratory’s 2024 Queued Up interconnection report. Sovereign campuses bypass that queue entirely.

The shift is now the dominant signal in 2026 AI infrastructure planning. Goldman Sachs Research projects data center power demand will rise roughly 165% by 2030. The IEA Electricity 2026 report flags AI as the fastest-growing electricity load class in advanced economies. Meanwhile, RMI’s 2024 interconnection queue analysis shows 2,600 GW of capacity stuck in study limbo across U.S. regional transmission organizations. Therefore, every GW added behind the meter is a GW that ships years sooner than its grid-tied alternative.

The takeaway up front. Grid power optimizes for the utility. Cloud GPU rental optimizes for the cloud vendor. By contrast, on-site generation optimizes for the buyer who funds the entire stack. SAVRN designed its sovereign campus model around this decision. SAVRN is the operator of an off-grid sovereign AI infrastructure campus model, with current developments underway in California, Texas, Colorado, Nebraska, Panama, and Barbados. Also, SAVRN owns its power, compute, and closed-loop liquid cooling, and deploys in 6 to 12 months versus the 24 to 48 month industry standard. This guide walks through the policy backdrop, the technology stack, the math, and the buyer evaluation framework.

Why behind the meter AI power defines the 2026 AI campus build

The grid is no longer the fast path to electrons. Three signals confirm the shift. First, interconnection queues now hold years of latent capacity. Second, the AI rack has outgrown the building envelope of conventional halls. Third, hyperscalers have begun signing on-site and adjacent generation contracts at unprecedented scale. Therefore, on-site generation has moved from edge case to default architecture for new builds.

The grid interconnection queue forces behind the meter AI power

Interconnection wait times have stretched past five years. LBNL’s Queued Up 2024 dataset shows the median wait from request to in-service has roughly doubled over the last decade. Also, withdrawal rates approach 80% across most regional grids. So, a developer who joins a queue today faces a 5-year clock. The same developer faces a 4-in-5 chance of project failure. On-site power skips both risks.

The wait penalty compounds at scale. A 500 MW grid request often triggers studies of network upgrades worth hundreds of millions of dollars. Therefore, the queued cost frequently exceeds the load itself. Meanwhile, on-site generation puts the same capacity on a campus inside 18 to 24 months. In short, the math has reset.

How behind the meter AI power compresses the deployment window

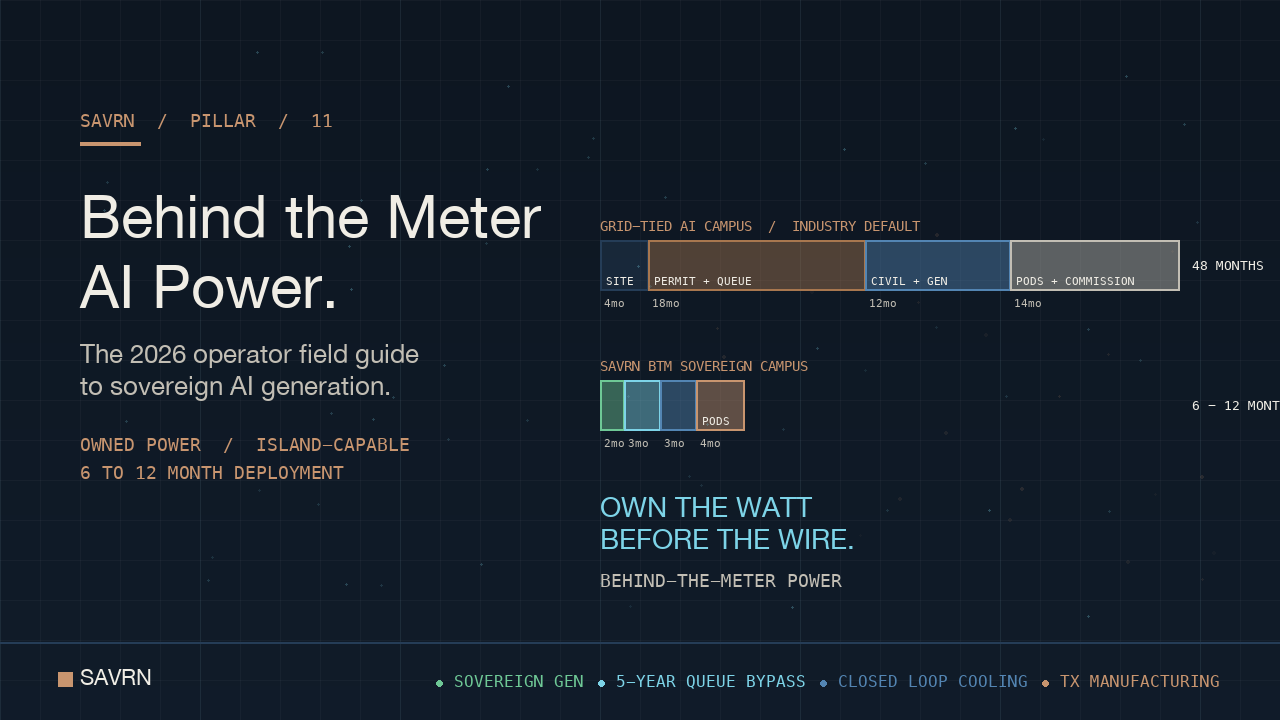

The classic AI data center build runs 24 to 48 months end to end. Permits, civil work, utility coordination, and substation upgrades drive most of that clock. By contrast, on-site power skips the utility coordination step. SAVRN compresses the timeline to 6 to 12 months by pre-identifying sites, owning the generation stack, and shipping prefabricated compute pods from SAVRN’s Intelliflex manufacturing footprint. Therefore, on-site generation is the keystone of the 6 to 12 month commitment.

Modular prefab also reshapes the construction critical path. IEEE Spectrum’s 2025 modular data center coverage shows 2 to 3 week field assembly windows for prefabricated halls compared with 12 to 16 weeks for stick-built equivalents. Notably, the savings stack with the generation savings. Hence the win versus a grid-tied campus often tops 30 months.

Why hyperscalers now chase on-site power deals

The 2024 to 2026 deal flow tells the story. Reuters reported in September 2024 that Microsoft contracted with Constellation Energy to restart Three Mile Island Unit 1, with first electrons targeted for 2028. Earlier the same year, Reuters covered Amazon Web Services’ $650 million purchase of a Talen-adjacent data center campus that draws power from the Susquehanna nuclear plant. Therefore, every major hyperscaler has now staked at least one campus on adjacent or on-site generation.

The same logic now flows down-market to enterprise AI buyers. Sovereign nations, defense primes, regulated industries, and AI-native scale-ups all face the same grid wait. So, the operator-owned campus model is no longer a niche posture. It is the default for any buyer who needs capacity inside two years.

The 2026 hyperscaler behind the meter AI power deal flow

The deal evidence is now public, dated, and verifiable through major outlets. Each contract carries an explicit decision to skip a traditional grid procurement path. Also, each deal anchors a multi-year capacity commitment that would have been impossible inside a regional grid queue. The pattern is the strongest market signal yet that BTM power has crossed from experiment to standard practice.

Microsoft, Constellation, and the Three Mile Island restart

Microsoft’s September 2024 power purchase agreement covers a restarted Three Mile Island Unit 1. The full output runs roughly 835 MW. The deal is the largest single nuclear PPA in U.S. history, per Reuters’ September 2024 reporting. Notably, the contract bundles 20 years of dispatchable nuclear output to AI workloads. Therefore, the unit functions as a long-term hedge against rising regional grid prices and queue uncertainty.

The deal also signals a shift in capital allocation. Microsoft committed to off-take pricing well above wholesale Mid-Atlantic levels. Yet the company viewed the certainty premium as worth paying. In short, predictable BTM power outranked spot-market savings.

Amazon, Talen, and the Susquehanna campus

Amazon Web Services bought the Cumulus campus in March 2024. The deal locked in 960 MW of BTM capacity from the Susquehanna nuclear plant. Reuters’ coverage shown the $650 million purchase price. Also, the contract structure routed nuclear electrons directly to data center load via a campus tie line. As a result, the setup sidestepped both transmission delivery charges and the regional grid queue.

The deal also drew Federal Energy Regulatory Commission scrutiny over wholesale market rules. FERC’s November 2024 order declined to approve the original interconnection service agreement amendment. Therefore, the regulatory wrinkle now feeds directly into how every subsequent campus structures its behind-the-meter design. So, FERC review is now part of the standard playbook.

Meta, Google, and the next wave of behind-the-meter deals

Meta announced exploratory nuclear sourcing in late 2024. Google signed a small modular reactor agreement with Kairos Power for first-of-kind units later in the decade, per Google’s October 2024 announcement. Meanwhile, Oracle disclosed plans for a 1 GW behind-the-meter footprint set by gas turbines. Therefore, the corporate roster behind on-site AI generation now extends past every major U.S. hyperscaler.

The next wave will mostly skip nuclear, however. Reactor restarts and SMRs cannot deliver inside 18 to 36 months. Most AI campuses need that window. Instead, the dominant near-term mix relies on fast-deploying gas, solar plus storage, and fuel cells. As a result, the practical 2026 to 2028 generation stack looks very different from the headline nuclear deals.

The generation stack behind the meter AI power operators choose

Generation choice depends on three constraints. First, rollout speed must match the AI build cadence. Second, dispatchability must match the workload’s duty cycle. Third, fuel and emissions posture must clear local permitting. Therefore, every BTM AI power architecture sits at a defensible point on the speed-dispatch-emissions triangle. The four dominant 2026 options each occupy a different corner.

Natural gas reciprocating engines and aero-derivative turbines

Natural gas remains the workhorse for fast-deploy capacity. Reciprocating engines from Caterpillar, Wartsila, and Rolls-Royce mtu ship in 12 to 18 months. Lead times stay in that band even at 100 MW class orders. Aero-derivative turbines extend the same logic. The 30 to 100 MW class fits the same fast-deploy posture. Also, modular packaging lets operators add capacity in 5 to 30 MW increments. Hence the dominant 2026 to 2028 BTM build leans heavily on gas.

Permitting and emissions posture are the binding constraints. EPA New Source Review and state Title V air permits typically run 9 to 18 months. EPA’s Title V program docs outlines the obligations. Therefore, owners pre-screen sites for air-quality classification before locking generation choices. In short, the gas option works wherever air permits clear.

Solar plus long-duration storage

Solar plus battery storage remains the lowest-permitting option in most jurisdictions. Also, levelized costs continue to fall. Lazard’s 2024 Levelized Cost of Energy report places utility-scale solar plus storage in the $30 to $80 per MWh range. However, the 24-hour AI duty cycle requires deeper storage than a typical grid-services pack. As a result, solar plus storage usually pairs with a firm complement.

The duty-cycle gap explains why most pure-renewable AI campuses also reserve gas or fuel cell capacity. Notably, the design decision is not a hedge. It is an architectural acknowledgment that AI workloads run hard at 3 a.m. The setup becomes a hybrid that maximizes the renewable share within the firm-power envelope.

Small modular reactors and the late-decade outlook

Small modular reactors anchor the late-decade outlook for BTM power. NuScale, X-energy, Kairos Power, and TerraPower each have NRC-progressed designs. The Nuclear Regulatory Commission’s SMR program page tracks ongoing reviews. However, first commercial deployments target 2029 to 2032 windows. Therefore, SMRs do not solve the 2026 to 2028 capacity problem. They reshape the post-2030 fleet.

The 2030+ fleet will likely blend SMRs with gas backup and renewables. Also, a multi-decade campus typically over-builds early generation and migrates the mix as new technology arrives. As a result, an owner must design the campus to accept new asset classes without redoing the foundational tie-in.

Fuel cells, hydrogen, and hybrid topologies

Solid oxide and proton exchange membrane fuel cells run on natural gas or hydrogen. Bloom Energy and Plug Power have both shipped multi-MW data center deployments. Also, fuel cells deliver high availability with low NOx output. Hence, sites with strict air-quality constraints often default to fuel cells over gas reciprocating engines. However, fuel cell capex remains higher than turbine alternatives.

Hybrid topologies blend two or three of these technologies. A typical mid-decade campus runs gas as the firm spine, solar plus storage for daytime offset, and fuel cells for low-emission backup. Therefore, the resulting all-in cost lands inside the band most enterprise buyers can model. In short, the hybrid strategy is the practical winner for the 2026 to 2028 cohort.

How behind the meter AI power math actually works

The financial case for on-site generation rests on three numbers. First, the levelized cost of energy from the chosen asset. Second, the avoided cost from skipping transmission and distribution charges. Third, the value of certainty against grid queue and price volatility. Therefore, every BTM proposal must price all three terms. A model that ignores any one term will misprice the build.

Levelized cost versus blended grid rate

Levelized cost of energy compares apples to apples across generation classes. Lazard’s 2024 LCOE places utility-scale solar plus storage at $30 to $80 per MWh. Gas combined cycle lands at $45 to $110 per MWh. SMRs top out at $89 to $230 per MWh. By contrast, retail industrial grid power often tops $80 per MWh. Transmission and distribution riders push the bill higher. Therefore, on-site generation often beats the all-in grid rate before counting queue avoidance.

The blended rate also includes ancillary services and capacity charges. Notably, regional grids routinely pass these costs through to large industrial loads. As a result, an AI campus on a regional industrial tariff can pay 30% more than the headline retail rate. The BTM power architecture removes most of those passthroughs.

Capacity factor, dispatchability, and reserve margin

AI duty cycles run hot. Training jobs sustain 80% to 95% utilization for weeks. Inference loads cycle daily with sharp peaks. Therefore, the generation asset must match the workload, not the average load. Also, reserve margin must cover unplanned outages without compromising training continuity. In short, the 24-hour design point dictates the asset choice.

Reserve margins on AI campuses now run 15% to 25% above peak. Hence the ratio between nameplate generation capacity and IT critical load typically lands at 1.4 to 1.6 to 1. The hyperscaler-backed sovereign campuses and SAVRN’s modular pods follow this ratio.

Heat rejection and the cooling overhead penalty

Cooling is the second-largest power consumer after the IT load. Air cooling fails above 60 kW per rack, per multiple Uptime Institute Global Data Center Survey 2024 readings. AI rack densities now reach 120 kW and beyond. Therefore, liquid cooling is no longer an option but a structural requirement. The closed-loop liquid architecture also removes the make-up water question that constrains many grid-tied builds.

Cooling efficiency feeds back into the watt term. A campus with rack-level liquid cooling sized for high-density AI workloads runs lower facility-side overhead than a hybrid air-liquid build. As a result, every kilowatt of the sovereign campus model generation delivers more useful tokens. The token-to-watt arithmetic favors the integrated stack.

Permitting and air-quality limits on behind the meter AI power

Permitting governs the practical menu of options at any given site. National Environmental Policy Act review applies to most federal-nexus projects. Also, EPA New Source Review covers any new air emissions source above thresholds. State Title V permits then layer on. Therefore, an early-stage site evaluation must rank candidate parcels by permitting velocity, not just land cost.

NEPA, EPA Title V, and state air permits

NEPA review applies whenever a federal permit, federal land, or federal funding touches the project. Most pure-private AI campuses avoid the NEPA trigger. EPA New Source Review and state Title V air permits do not. The EPA’s Title V program guide walks through the obligations. Also, the Title V clock typically runs 9 to 18 months for major-source applications. As a result, the air permit becomes the long pole in the BTM tent.

State agencies handle most of the workload. Texas TCEQ, California CARB, and Colorado APCD each maintain distinct minor-source thresholds. Hence, a multi-state operator must run parallel permit tracks rather than reusing a single template. In short, the permit lift scales with the number of generation classes the campus deploys.

Interconnection (parallel) versus island-mode operation

BTM assets can run parallel to the grid or in island mode. Parallel operation provides backup, peak shaving, and demand response revenue. Island mode removes utility coordination entirely. SAVRN’s sovereign campus model defaults to island-capable architecture, with optional parallel tie-ins where it adds value. Therefore, the campus retains full operational autonomy while preserving the option for utility interaction.

Island mode also simplifies the FERC interaction. Parallel BTM facilities now face heightened FERC scrutiny in the wake of the Amazon-Talen amended ISA decision. By contrast, true island operation falls under state retail jurisdiction. As a result, the regulatory load shrinks to one set of state agencies plus EPA.

Community engagement, noise, and visual impact

Local community sentiment shapes practical permitting outcomes. Reciprocating engines run loud and produce visible plumes. Solar arrays cover acres. SMRs invite their own siting debates. Therefore, an operator who skips early community engagement typically loses six to twelve months on appeals. Hence the better practice is open disclosure, third-party noise modeling, and a shown community benefit posture before applications go in.

The closed-loop, near-zero-water-use posture eases one major friction point. SAVRN’s verified water analysis shows how closed-loop liquid cooling removes the water-takings argument that has stalled multiple grid-tied projects. Therefore, the sovereign campus model campuses with closed-loop cooling avoid one of the most reliable opposition vectors.

Behind the meter AI power versus grid AI power: decision framework

The decision is not binary in every case. Some buyers retain grid as a true backup. Others choose grid-set builds with diesel or gas backup only. Still others go fully sovereign. The right answer depends on workload duration, sovereignty requirement, capacity scale, and time-to-revenue pressure. Therefore, the framework below maps each buyer profile to the architecture that minimizes total program risk.

When grid AI power still wins

Grid power still wins for short-horizon, sub-50 MW deployments inside utility territories with available capacity. Also, regulated industries that need a state-utility relationship for compliance reasons may prefer grid anchoring. As a result, the grid path remains the right choice for a meaningful share of mid-sized enterprise buyds. However, that share shrinks every year as AI workloads scale and queues lengthen.

Grid power also wins where electrons are already plentiful and cheap. Several U.S. regions still offer industrial rates below $40 per MWh with 24-month interconnection windows. Notably, those pockets shrink each quarter. Hence the grid-only path is a tactical choice, not a strategic one.

When behind the meter AI power wins decisively

BTM wins decisively for any build above 100 MW with a sub-24-month timeline. Also, sovereignty requirements (defense, classified, regulated AI workloads) tip the decision the same way. Add the 5-year LBNL queue median, and the choice frequently makes itself. In short, capacity, speed, and sovereignty all push the same direction once the build crosses the hyperscale threshold.

The economic case strengthens as scale grows. SAVRN’s build versus buy AI stack analysis shows the crossover. By contrast, owners who lease cloud GPU hours at high utilization pay several multiples of the SAVRN levelized cost. Therefore, the same workload run behind the meter delivers a by design lower cost per token.

The hybrid case: BTM with grid backup

Hybrid setups split the difference. The BTM asset carries the bulk of the load. Meanwhile, a grid tie provides a low-cost backstop for unplanned outages or peak shaving. Also, the setup unlocks ancillary revenue from demand response programs. As a result, the hybrid model fits well-aged grid territories with stable utility relationships. However, the hybrid carries its own permitting load.

Hybrid economics depend on the utility tariff structure. Some tariffs penalize demand when on-site generation reduces consumption. Others reward grid services. Therefore, the operator must model both the technical and tariff outcomes before committing. In short, the hybrid path is operationally elegant but contractually complex.

How SAVRN operationalizes behind the meter AI power

SAVRN’s sovereign AI infrastructure thesis treats on-site power as the foundation, not an add-on. The campus design starts with the generation asset, sizes the compute footprint to match, and deploys both inside the same 6 to 12 month window. Therefore, the sovereign campus model is the load-bearing wall of the SAVRN doctrine. Every other architectural decision flows from that anchor.

Sovereign campus architecture and the integrated stack

The SAVRN campus runs an integrated stack: generation, distribution, IT load, cooling, and waste-heat capture. Each layer is owned, sized, and dispatched together. Also, the closed-loop liquid cooling system removes the make-up water draw that constrains conventional builds. SAVRN’s sovereign AI infrastructure pillar walks through the full stack. Hence the BTM generation choice is one of seven coordinated decisions, not a standalone procurement.

The integration produces architectural advantages no fragmented build can match. Notably, the dispatch layer routes electrons inside the campus boundary at distribution voltage, with no regulated transmission charges. Therefore, the all-in cost per delivered megawatt-hour drops sharply against a grid-anchored equivalent. In short, the integrated stack is more than a brand. It is a financial structure.

Intelliflex pod manufacturing in Fort Worth

SAVRN owns the pod manufacturing footprint. Intelliflex pods ship from a domestic Fort Worth manufacturing line, with the Customer Experience Center as a recently launched destination for buyer evaluation. Also, integrated manufacturing collapses the supply chain risk that has stretched conventional data center timelines. As a result, the campus rollout cadence stays inside the 6 to 12 month commitment regardless of the global build pipeline.

The domestic manufacturing posture also matters for sovereignty buyers. Defense, regulated industries, and sovereign nation buyers all face supply chain disclosure requirements. Hence the Fort Worth manufacturing footprint pre-clears the supply chain question that often stalls procurement reviews. The integration with on-site power generation closes the sovereignty loop.

The 6 to 12 month deployment window

The 6 to 12 month rollout window is the most concrete differentiator SAVRN operates against. Phase one runs site finalization, generation planning, and air-permit pre-application during weeks 1 to 8. The civil work and generation set installation then run weeks 9 to 20. Modular pod start-up fills weeks 21 to 32. First token follows by week 48 at the latest. Therefore, the timeline is not a marketing claim. It is a phase-by-phase operating plan.

The full timeline detail lives in SAVRN’s deployment timeline pillar. Notably, every phase depends on the BTM generation choice locked at the start. Hence, on-site power is the first decision and the most consequential one. The remaining 47 weeks execute against that anchor.

Buyer checklist for evaluating behind the meter AI power proposals

The evaluation checklist below maps the buyer’s diligence against the architectural choices. Each line item carries a verifiable artifact the proposer should produce on request. Therefore, a thin or vague answer on any line is a real signal of program risk. Also, the items also frame the renegotiation surface for any deal that proceeds. In short, the checklist functions as a procurement gate, not a marketing exercise.

- Generation technology and OEM: identify the make, model, and class of every generation asset, with delivery windows and warranty backstops named.

- Permit status: confirm air-quality classification, NSR pre-screen, and Title V application timeline. A vague answer here is the single biggest schedule risk.

- Fuel supply and contract: name the fuel supplier, contract tenor, and hedging posture. Spot-only exposure is a flag.

- Dispatch architecture: parallel, island, or hybrid. Document the FERC posture if any tie-in exists.

- Reserve margin: confirm a 15% to 25% reserve above peak. Anything tighter is a continuity risk.

- Cooling integration: ensure rack-level cooling is sized for high-density AI workloads. Verify closed-loop status to remove water draw.

- Heat-rejection capture: ask whether waste heat is captured for reuse or vented. Capture is now a standard 2026 expectation.

- Sovereignty posture: confirm domestic manufacturing of pods, generation assets, and supply chain disclosure scope.

- Deployment timeline: insist on a phase-by-phase week-numbered plan, not a year-quarter range.

- Operations team and runbooks: confirm 24/7 staffing model and named runbook coverage for major fault classes.

Buyers who score every proposal against the same ten items quickly separate the operator-grade builds from the marketing decks. Also, the checklist forces the proposer to surface real engineering content, not slogans. As a result, the diligence cycle compresses from months to weeks. Hence, the checklist is also a time saver.

Frequently asked questions about behind the meter AI power

What is behind the meter AI power in plain terms?

The phrase describes generation sited on the customer side of the utility revenue meter, dispatched directly to AI compute load. The owner generates the electrons, owns the wire, and skips most transmission and distribution charges. Also, the model bypasses the multi-year regional grid interconnection queue shown by LBNL and RMI. As a result, the architecture is now the default for sovereign AI campuses and most new hyperscale builds above 100 MW.

How does behind the meter AI power compare to grid power on cost?

The comparison depends on geography and generation choice. Lazard’s 2024 LCOE places utility-scale solar plus storage at $30 to $80 per MWh and gas combined cycle at $45 to $110 per MWh. Retail industrial grid rates frequently exceed $80 per MWh once transmission and distribution riders are stacked. So, on-site power often beats the all-in grid rate. The win lands before the buyer counts queue avoidance and FERC-tariff exposure. The crossover favors BTM most strongly above 100 MW deployments.

How long does behind the meter AI power take to deploy?

Rollout runs 12 to 24 months for most gas, fuel cell, and solar-plus-storage setups, depending on permit posture. SMR-anchored campuses target 2029 to 2032 first commercial operation. SAVRN compresses the full campus rollout to 6 to 12 months by pre-identifying sites, owning the generation stack, and shipping prefabricated Intelliflex pods from a domestic manufacturing line. Therefore, the SAVRN window improves on the industry default by a factor of three to four.

Which generation technologies are most common for behind the meter AI power in 2026?

Natural gas reciprocating engines and aero-derivative turbines dominate the 2026 to 2028 cohort. Solar plus long-duration storage covers a growing share. Permit speed favors renewables in many states. Fuel cells fill the low-emission niche on tight air-quality sites. Small modular reactors arrive late decade. As a result, most sovereign campuses now run hybrid setups that blend gas, renewables, and fuel cells inside the same envelope.

How does behind the meter AI power affect AI deployment timelines?

The grid-tied path runs 24 to 48 months end to end, with the multi-year interconnection queue acting as the binding constraint. On-site power skips the queue entirely. Therefore, the campus build collapses to 12 to 24 months under standard execution, and to 6 to 12 months under SAVRN’s integrated model. As a result, owners reach first token roughly three years sooner. The compounding revenue impact often exceeds the entire generation capex.

Which hyperscalers signed the largest behind-the-meter deals so far?

Microsoft signed a 20-year PPA with Constellation in September 2024 to restart Three Mile Island Unit 1, roughly 835 MW, per Reuters. Amazon Web Services purchased the Talen Cumulus campus in March 2024 for $650 million, anchored by 960 MW of Susquehanna nuclear capacity. Google signed a small modular reactor agreement with Kairos Power in October 2024. Meta has flagged exploratory nuclear sourcing. Therefore, every major U.S. hyperscaler is now publicly committed to BTM or campus-adjacent generation.

Is behind the meter AI power suitable for defense or sovereign workloads?

Yes. Sovereignty requirements push directly toward operator-owned campuses. Defense primes, regulated AI workloads, and sovereign nation buyers all need supply chain disclosure, physical isolation, and grid-independence options. Therefore, BTM architectures combined with domestic manufacturing of compute pods address each requirement at once. SAVRN’s Intelliflex Fort Worth manufacturing footprint and sovereign campus model fit this buyer profile directly. SAVRN’s defense AI infrastructure pillar walks through the alignment with DoD compute mandates.

What permits does behind the meter AI power generation require?

The permit stack varies by technology and state. Federal NEPA review applies whenever a federal nexus exists. EPA New Source Review covers air emissions thresholds. State Title V permits add 9 to 18 months for major sources. EPA program guidance sets the clock. Also, state-level agencies (TCEQ in Texas, CARB in California, APCD in Colorado) handle minor source thresholds. As a result, multi-state operators must run parallel permit tracks rather than reusing a single template.

How does behind the meter AI power interact with FERC and wholesale markets?

Island-mode operation falls under state retail jurisdiction and avoids FERC oversight. Parallel operation triggers FERC review, especially for co-located large-load setups. The November 2024 FERC order rejected the Amazon-Talen amended ISA. The ruling reset the playbook for any campus with a parallel tie. So, SAVRN defaults to island-capable design. Optional parallel tie-ins are added when the value justifies the regulatory load. In short, the architecture is FERC-aware by design.

Does behind the meter AI power solve the AI water question?

BTM generation does not directly solve the water question. Closed-loop liquid cooling does. So, a sovereign campus pairs on-site power with closed-loop liquid cooling. The setup removes both the grid dependency and the make-up water draw. SAVRN’s verified water analysis shows the bottoms-up math for Texas builds. As a result, the integrated SAVRN architecture sidesteps the two most reliable opposition vectors against new AI campuses.

When is grid power still the right choice over behind the meter AI power?

Grid power still wins for short-horizon, sub-50 MW builds. The buyer needs a utility territory with capacity and a 24-month tie-in window. Also, regulated industries that need a state-utility relationship for compliance reasons may prefer grid anchoring. As a result, the grid path remains the right choice for a meaningful share of mid-sized enterprise builds. However, that share shrinks every year as AI workloads scale and queues lengthen.

Continue exploring SAVRN doctrine on behind the meter AI power

The on-site power thesis sits inside the larger SAVRN doctrine. Each linked piece below extends one dimension of the same operating model. Therefore, the body of work reads as a connected playbook for sovereign AI campus development, not a series of isolated essays. Also, every piece carries the same primary-source citation discipline. The reader can audit each claim independently.

- SAVRN sovereign AI infrastructure — the full stack guide to off-grid, owned AI compute, with the seven architectural decisions that flow from the BTM anchor.

- AI infrastructure deployment timeline — phase-by-phase week-numbered breakdown of the 6 to 12 month sovereign campus build.

- Build vs buy AI infrastructure — the case for sovereign campus ownership versus cloud GPU rental and traditional colocation.

- Tokens per watt per dollar — the unified 2026 metric that fuses throughput, energy, and capital, with on-site generation as the watt-term lever.

- The 49 billion gallon mirage — verified bottoms-up water model for AI data centers, with the closed-loop architecture that removes the water question.

- SAVRN About Us — the team, the doctrine, and the sovereign AI utility thesis that anchors every campus.

Submit a site evaluation request through SAVRN’s stack assessment form if your organization controls land or load that fits the on-site power profile. The assessment process screens for power proximity, fiber, zoning, and air-quality classification inside 48 hours. Also, a full site assessment runs two to four weeks. As a result, qualified sites move to a rollout proposal inside the same quarter as the initial inquiry.

Sources & Citations

Every quantitative claim in this piece traces to a named, verified primary source. URLs verified at time of publication. The full audit-grade citation record, with claim-by-claim source mapping and “cite this article” snippets, is maintained on the dedicated SAVRN sources page for this piece.

Primary research cited in this behind the meter ai power brief

- LBNL — Queued Up 2024 interconnection report. Lawrence Berkeley National Laboratory ‘Queued Up’ 2024 interconnection report — 2,600+ GW in U.S. queues, 5-year median wait that drives the behind-the-meter case.

- RMI — Queued Up 2024 Edition analysis. RMI 2024 interconnection queue analysis — independent corroboration of LBNL queue data plus policy reform framing.

- FERC — November 2024 order on Amazon-Talen co-located load. FERC November 2024 order rejecting amended ISA for Amazon-Talen co-located load — establishes the regulatory precedent governing co-located generation+load arrangements.

- EPA — Title V Operating Permits. EPA Title V Operating Permits program — air-emissions permitting baseline for behind-the-meter natural gas generation.

- NRC — Small Modular Reactor program. Nuclear Regulatory Commission Small Modular Reactor program — federal regulatory framework for the nuclear behind-the-meter path.

- Reuters — Constellation Three Mile Island restart for Microsoft (Sept 2024). Reuters September 2024 reporting on Constellation’s Three Mile Island restart for Microsoft AI data centers.

Supporting frameworks, regulators, and industry data

- Reuters — AWS buys data center campus from Talen Energy (March 2024). Reuters March 2024 reporting on Amazon Web Services’ $650 million purchase of Talen Energy data center campus.

- Google — Kairos Power nuclear energy agreement announcement (Oct 2024). Google’s October 2024 announcement of small modular reactor agreement with Kairos Power.

- Lazard — Levelized Cost of Energy+ 2024. Lazard 2024 Levelized Cost of Energy report — published cost curves used as the BTM-vs-retail benchmark.

- Goldman Sachs Research — AI poised to drive 160% increase in power demand. Goldman Sachs Research projection on AI-driven data center power demand growth.

- IEA — Electricity 2026. IEA Electricity 2026 outlook on power demand from data centers and AI.

- IEEE Spectrum — AI Data Center reporting. IEEE Spectrum 2025 modular data center coverage — independent technical reporting on co-located generation+compute architectures.

- Uptime Institute Global Data Center Survey 2024. Uptime Institute Global Data Center Survey 2024 — operator practice baseline.