AI factory infrastructure is the physical stack that converts electrons into tokens at gigawatt scale. Conventional AI data centers commission in 24 to 48 months and stall in five-year grid interconnection queues, per Lawrence Berkeley National Laboratory’s 2024 Queued Up report. SAVRN deploys AI factory infrastructure in 6 to 12 months by owning the power generation, the cooling loop, and the manufacturing line that produces the compute pods.

SAVRN is the operator of an off-grid sovereign AI infrastructure campus model. SAVRN owns its power generation, compute, and closed-loop liquid cooling, deployed in 6 to 12 months versus the 24 to 48 month industry standard, with current developments underway in California, Texas, Colorado, Nebraska, Panama, and Barbados. Therefore this piece is the SAVRN operator’s playbook for the AI factory infrastructure category in 2026: what it is, what blocks it, what it costs, and how to ship one before the grid queue clears.

AI factory infrastructure: from electrons to tokens

The phrase entered the operator lexicon in 2024. However, it became canonical at NVIDIA GTC 2026, where Jensen Huang defined an AI factory as a production facility whose primary economic output is a token, per Data Center Frontier’s GTC 2026 coverage. Tokens, not virtual machines. Tokens, not hosting tenancies. Furthermore, tokens are billed by the million and constrained by available watts.

Huang’s framing recasts the operator question. Revenue equals tokens per watt multiplied by available gigawatts. Therefore every architectural decision, from the substation to the cold plate, lives or dies by how it touches that equation. Moreover, the operator who can extract more tokens per watt, or who can light up more gigawatts faster, wins disproportionately.

That recasting matters because the conventional data center industry is not built for it. In addition, hyperscale colocation evolved around 10 to 15 kilowatts per rack, air cooling, utility power purchase, and 24 to 48 month build cycles, per JLL’s 2026 Global Data Center Outlook. AI factory infrastructure rejects almost every one of those defaults. Consequently, what looks like a denser data center is in fact a different building category.

The shift is also a vocabulary shift. The buyer used to ask for megawatts and uptime tier. Now the buyer asks for token throughput, latency to first token, and cost per million tokens. As a result, conventional sales motions, designed around floor-space leases, fail in the AI factory category. The seller has to talk power, cooling, and inference economics fluently or lose the deal in the first meeting.

Why AI factory infrastructure breaks the conventional data center model

Three thresholds explain the break. The category crosses each of them, and the conventional model breaks at each crossing. Moreover, the breaks are structural rather than incremental, which is why retrofit strategies typically underperform purpose-built campuses on both capex and time-to-revenue.

The 60 kilowatt per rack threshold

Air cooling fails above roughly 60 kilowatts per rack, per Lombard Odier’s January 2026 analysis. Modern AI training racks draw 80 to 130 kilowatts under full load. Some frontier rack-scale systems draw more. Therefore air-cooled white space is technically obsolete for AI training, and rear-door heat exchangers retrofit only a narrow density band.

The implication for the AI factory category is structural. Cold-plate liquid cooling, single-phase immersion, or two-phase immersion are no longer alternatives. They are the only thermal architectures that work. Goldman Sachs forecasts liquid-cooled AI servers reaching 76 percent of the market in 2026, up from 15 percent in 2024. Consequently, liquid is the default; air is the exception.

The 100,000-home power profile per site

A single AI factory now consumes power equivalent to roughly 100,000 homes, per the International Energy Agency. Hyperion in Louisiana is sized at 5 gigawatts. Prometheus in Ohio is sized at 1 gigawatt, per publicly announced project filings. Furthermore, total AI data center power demand rose to 415 terawatt-hours in 2024 and is projected to reach 945 terawatt-hours by 2030, per IEA 2025 figures.

Consequently, AI factory infrastructure is fundamentally a power utility question dressed as a real estate question. Build it where the electrons live, or generate the electrons on site. There is no third option. Importantly, that shift redraws the site selection map: power, not latency or land cost, is now the dominant constraint, and the constraint reordering invalidates many of the location-first heuristics that hyperscale operators relied on for two decades.

The token economics layer

Hyperscale data centers sold square feet, megawatts, and uptime. By contrast, the AI factory category sells tokens per second, latency to first token, and cost per million tokens. As a result, the operator’s profit-and-loss statement now correlates with thermal efficiency, GPU utilization, and grid carbon mix rather than with floor-plate density alone.

SAVRN’s Tokens Per Watt Per Dollar metric codifies the token economics shift. Specifically, it integrates capex, opex, and throughput into one operator-grade number. Therefore campuses can be benchmarked against themselves across vendors and years, which is the diligence comparable buyers now ask for in the first pricing conversation.

What blocks AI factory infrastructure: the four hard limits

Operators planning a 2026 build encounter four blockers that no amount of capital alone can clear. Each one stretches the timeline. Together, they explain why the average hyperscale project now takes 24 to 48 months to commission. Moreover, the four blockers compound rather than substitute: clearing one without clearing the others is a partial solution that still slips the schedule.

Grid interconnection backlog

The PJM interconnection queue now averages over eight years from application to commercial operation, up from less than two years in 2008, per LBNL’s 2024 Queued Up report. In short, the grid is the bottleneck before the building is even designed. Therefore any plan that depends on a new utility interconnection in 2026 is already late.

Sightline Climate’s 2026 pipeline analysis found that of the roughly 16 gigawatts slated to complete in 2026, only about 5 gigawatts was actively under construction at the point of analysis. As a result, the firm estimates 30 to 50 percent of that pipeline will slip into 2027 or later. Furthermore, pipeline slippage is now the base case, not the exception.

Switchgear and turbine lead times

Transformer lead times have stretched to 18 to 30 months on common voltage classes. In addition, large gas turbine lead times now reach five to seven years, per TechCrunch’s April 2026 supply-chain reporting. By contrast, ten years ago both ran inside 12 months. Consequently, the equipment that powers the category is rationed by supplier capacity, not buyer demand.

Operators who pre-secured equipment slots in 2023 and 2024 hold a near-insurmountable scheduling advantage today. By contrast, operators who did not are forced into used-equipment markets, reciprocating engines, fuel cells, and hybrid mixes. In other words, the supply chain rewards pre-commitment. Moreover, secondhand markets have tightened as buyers competing for new equipment pull from the same pool that traditionally served redundancy and disaster recovery customers.

Cooling architecture obsolescence blocks AI factory infrastructure

Air-cooled hyperscale white space, designed for 10 to 20 kilowatts per rack, cannot host current AI workloads without significant retrofit. Liquid cooling at AI factory scale costs roughly 4.5 to 5.2 million dollars per megawatt of thermal capacity, per Adam Silva Consulting’s 2026 cooling economics analysis. By contrast, that is two to three times the cost of conventional air-side rejection.

Retrofit is rarely the cheapest path. SAVRN’s liquid cooling for AI playbook shows that purpose-built campuses with rack-integrated cold plates beat retrofit on both capex and time-to-first-token. Moreover, retrofit campuses inherit the structural weight, ceiling height, and floor drain limits of buildings designed for a different physics problem. Therefore the retrofit savings disappear once concrete reinforcement, slab cuts, and roof-load upgrades are priced in.

Permitting and zoning friction

Local opposition to large-load AI projects accelerated through 2025 and 2026. Twelve U.S. states have considered moratorium or restrictive-permitting bills, per SAVRN’s 2026 moratorium tracker. Water draw, noise, transmission corridor visual impact, and tax abatement scrutiny all surface in public hearings. Furthermore, permit timelines have stretched to 12 to 24 months in some jurisdictions that approved similar projects in three months a decade ago.

Therefore site qualification now requires legal and community-engagement due diligence before any concrete is poured. In short, the campuses that ship on time are the ones that selected jurisdictions willing to host high-density industrial loads, generally those with industrial heritage and stable workforce pipelines. Moreover, early community engagement, rather than after-the-fact public relations, is now the operator-side practice that correlates most strongly with on-schedule delivery.

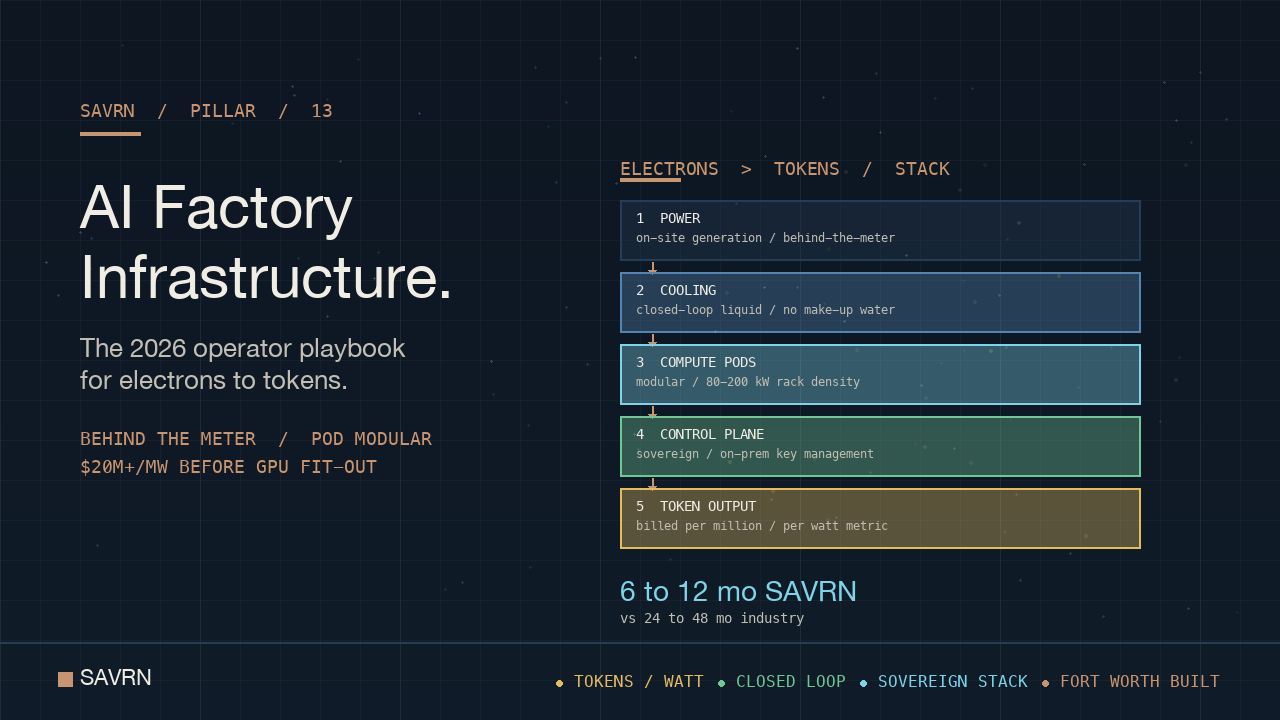

The five components of AI factory infrastructure

Strip the jargon and the category resolves to five integrated components. Each one has to fit the others. Furthermore, mix-and-match procurement across vendors with incompatible designs is the most common reason operator timelines slip past 36 months. In addition, integration failure typically surfaces during commissioning, when remediation is most expensive.

On-site power generation

Cleanview’s February 2026 forecast projects that 30 percent of new data center energy capacity in 2026 will come from on-site generation, up from effectively zero a year earlier. Cleanview founder Michael Thomas projects the figure could rise to 50 percent. In short, behind-the-meter generation is no longer alternative, it is mainstream. Consequently, AI campuses with on-site generation can sidestep the grid queue entirely.

SAVRN’s campus model integrates natural gas reciprocating engines, gas turbines, and battery storage as the primary generation stack. Grid interconnection, where it exists, becomes a redundancy layer rather than the primary feed. As a result, time-to-first-electron collapses from five years to under twelve months. Moreover, owning the generation lets the operator hedge fuel cost rather than chase utility rate filings.

Liquid cooling at rack density

The category relies on direct-to-chip liquid cooling for the 50 to 200 kilowatt rack density band, and on single-phase or two-phase immersion above 150 kilowatts, per the 2026 cooling-class operator playbook. Closed-loop secondary fluid networks, sized cooling distribution units, and dry-cooler heat rejection complete the loop.

Critically, the SAVRN closed-loop design removes the make-up water requirement that plagues conventional evaporative cooling, addressing the water-draw concern that drives much of the local permitting friction. Therefore the cooling architecture doubles as a community-relations argument. Furthermore, the elimination of evaporative loss is also an opex savings that compounds over the campus’s operating life.

High-density compute pods

Modular compute pods sized for NVIDIA’s enterprise AI factory roadmap allow the category to be unit-replicated rather than custom-engineered per campus. Each pod ships with rack power, liquid manifold, network spine, and management plane pre-integrated. Consequently, on-site assembly is a connector job, not a fabrication job.

Pod-based design lets a campus grow in measured increments. Furthermore, pods can be reseated to host successor compute generations as they reach general availability, which protects the capex against the rapid hardware refresh cycle. In other words, the long-lived asset is the campus envelope; the pods are the upgradable layer.

Closed-loop water systems

Closed-loop water reuses the same coolant indefinitely, replenishing only against evaporation losses on a dry-cooler-only architecture. The result is near-zero make-up water. SAVRN’s water-claim adjudication documented the closed-loop math relative to the headline 49 billion gallon industry figure.

For campuses sited in water-stressed geographies such as parts of California, Texas, and Nebraska, the closed-loop architecture is not a marketing line. It is the only design that survives local water-board review. By contrast, evaporative-cooled retrofits stall in permitting. Moreover, the no-make-up posture is now a default expectation in commercial offtake negotiations rather than a feature.

Sovereign control plane

The category serving regulated industries, federal customers, and sovereign customers requires data residency, hardware provenance, and operational control that hyperscale colocation cannot provide. SAVRN’s sovereign AI infrastructure framing defines the control-plane requirements: on-premise compute, named provenance for every component, and operator-owned key management.

Sovereign control is also a procurement-time question, not a runtime add-on. Therefore campuses designed sovereign-first cost less than equivalent capacity retrofitted for compliance after the fact. Furthermore, sovereign posture increasingly carries weight in commercial enterprise procurement as well, not only federal procurement, because supply chain documentation has become a board-level audit item.

AI factory infrastructure economics: capex, opex, tokens per watt

The economic profile of the category differs from conventional colocation along three axes. Capex per megawatt is higher. By contrast, opex per token is lower. Time-to-revenue is the swing variable. Moreover, the economics interact: a higher capex that yields earlier revenue and lower opex per token wins on net present value against a cheaper, slower alternative.

Per-megawatt build cost in 2026

JLL forecasts the standard shell-and-core data center build at 11.3 million dollars per megawatt for 2026, a six percent year-over-year increase. AI-optimized facilities exceed 20 million dollars per megawatt before GPU fit-out. Furthermore, with GPU and networking included, total all-in cost runs 30 to 40 million dollars per megawatt.

Electrical scope drives 30 to 40 percent of facility cost. In addition, cooling drives another 15 to 25 percent at AI factory infrastructure densities. The civil envelope, by contrast, accounts for under 20 percent. In other words, the equipment package, not the building, is now the cost story. Consequently, equipment sourcing capability is the operator competency that compounds over multi-campus pipelines.

Cooling capex differential

Cooling capex at AI factory densities runs 4.5 to 5.2 million dollars per megawatt for liquid-cooled architectures, against roughly 1.8 million dollars per megawatt for traditional air rejection, per Adam Silva Consulting’s 2026 analysis. The liquid premium is real. However, it is offset by the throughput gain at higher rack densities and the floor-space efficiency.

At the 16-rack hall level, infrastructure capex runs 1,800 to 3,200 dollars per kilowatt for rear-door heat exchangers, 3,500 to 5,000 dollars per kilowatt for direct-to-chip cooling, and 4,300 to 6,500 dollars per kilowatt for single-phase immersion. Consequently, the choice of cooling class is a multi-million-dollar swing per megawatt of capacity. Moreover, the choice cascades: pick the wrong class and the GPU thermal envelope forces a redesign two years in.

Tokens per watt per dollar as the operating metric

Conventional data center benchmarks, PUE and uptime tier, do not capture the economics of the category. SAVRN’s tokens per watt per dollar metric combines throughput, electricity efficiency, and amortized capex into one operator-grade ratio. Consequently, it lets a buyer compare a Texas campus on natural gas against a Nebraska campus on grid hydro against a colocation slot in California on an apples-to-apples basis.

The metric also exposes hidden trade-offs. For example, lower PUE that ships a year late loses to higher PUE that ships in nine months. Therefore tokens per watt per dollar should anchor every AI factory infrastructure procurement conversation. In addition, the metric is a forcing function on operator transparency, since vendors who cannot produce the underlying numbers self-select out of serious diligence cycles.

How SAVRN delivers AI factory infrastructure in 6 to 12 months

The SAVRN deployment compresses the conventional 24 to 48 month industry standard to 6 to 12 months through four architectural decisions, each of which collapses a category of delay. Moreover, the four decisions reinforce each other rather than substitute, which is why the compounded compression outperforms what any one decision would yield in isolation.

Pre-identified sites

SAVRN’s pipeline of qualified sites across California, Texas, Colorado, Nebraska, Panama, and Barbados has been pre-vetted on power availability, water posture, zoning, transmission, and community alignment. As a result, the site selection phase shrinks from 12 to 18 months down to under 90 days. The buyer arrives, the site is ready, and the engineering kicks off the same week.

Pre-identified sites also unlock parallel work streams. For example, while power contracting closes, on-site civils begin. Meanwhile, while pods manufacture in Fort Worth, fiber pulls finish in the field. Consequently, the critical path is engineered, not discovered. Furthermore, the parallelization eliminates the conventional waterfall sequencing that turns a 12 month schedule into a 36 month one.

Behind-the-meter power as AI factory infrastructure backbone

Behind-the-meter generation sidesteps the multi-year grid interconnection queue. SAVRN’s natural gas reciprocating engine and gas turbine packages, paired with battery storage, deliver firm capacity inside 12 months on the campus. SAVRN’s behind-the-meter operator field guide details the operating model, fuel sourcing, and emissions posture.

Behind-the-meter is also a contractual hedge against grid-tariff escalation. Specifically, the operator owns the fuel curve rather than the rate filing curve. Therefore long-tenor offtake contracts can be priced with confidence. Moreover, the behind-the-meter posture decouples the customer’s compute roadmap from the host utility’s capital plan, which is increasingly a procurement-side requirement for enterprise buyers.

Intelliflex integrated manufacturing

SAVRN’s Intelliflex integrated manufacturing operation, based in Fort Worth, fabricates AI factory infrastructure pods, switchgear assemblies, and liquid-cooling skids under one roof. As a result, the supply chain is internal rather than dependent on third-party fabricators with multi-year backlogs.

The Intelliflex Customer Experience Center in Fort Worth lets buyers see the production line in person before signing. Consequently, procurement diligence shifts from spec-sheet review to physical walk-through, which materially de-risks the buy decision. Furthermore, internal manufacturing means engineering change orders flow through the same factory floor without renegotiating supplier contracts.

Modular liquid-cooled compute pods

Each modular pod ships with rack power, cooling manifold, and network spine factory-integrated. On-site assembly is therefore a connector job. Specifically, the pod arrives, the power and water are connected, the racks are populated, and the campus accepts workload. Compared to stick-built construction, the modular model collapses commissioning from months to days per pod.

Pods also future-proof the campus. Successor compute generations slot into the same pod footprint as they reach general availability. Therefore the operator avoids re-permitting and re-civils every 18 to 24 months. In short, the campus evolves without rebuilding. Moreover, the upgradable layer keeps the campus on a state-of-the-art tokens-per-watt curve through multiple hardware generations.

AI factory infrastructure deployment: the SAVRN sequence

The SAVRN delivery sequence breaks into four phases that overlap intentionally. Furthermore, phases overlap because the conventional waterfall is the root cause of 36 month timelines. In short, the sequencing change is the largest single contributor to the 6 to 12 month outcome.

Phase 1: Site qualification and power contracting

Site selection completes in under 90 days using the pre-qualified pipeline. In parallel, power contracting, whether behind-the-meter fuel supply or a hybrid behind-the-meter plus grid interconnection design, closes. Furthermore, water-board and zoning reviews begin in week one rather than after engineering closes.

The output of Phase 1 is a notice-to-proceed package that committee-approves cleanly. Consequently, capital draws start on schedule and the customer’s CFO sees firm milestones. Moreover, the Phase 1 documentation package also doubles as the underlying record for project finance, which keeps the financing close-of-funds on the same critical path as engineering kickoff.

Phase 2: Manufacturing in Fort Worth

Intelliflex builds compute pods, switchgear, and cooling skids in parallel with field civils. The Fort Worth line is built for AI factory infrastructure pod throughput, not generic fabrication. As a result, lead time for finished pods is measured in weeks rather than the 18 to 30 months facing buyers in the open market.

Critically, the manufacturing phase is also where quality control catches issues that would otherwise emerge on-site. Therefore commissioning at the campus is cleaner and faster. Furthermore, the factory environment is where rework is cheapest. In other words, the cost of a defect detected in Fort Worth is a fraction of the cost of the same defect detected after the pod has shipped to a remote site.

Phase 3: On-site assembly and commissioning

Pods, switchgear, and cooling skids land at the site. On-site assembly connects power, water, network, and management plane. Furthermore, commissioning runs unit-by-unit rather than waiting for the whole campus to integrate. Consequently, the first token can flow before the last pod lands.

Phase 3 outputs are measurable: rack-level power proven, cooling loop pressure-tested, GPU diagnostics passing. In addition, each pod accepts production workload independently, so revenue starts well before final campus completion. Moreover, the unit-by-unit commissioning model gives the operator a steadily expanding revenue base rather than a binary go-live event that exposes the customer to single-window slippage.

Phase 4: Token-bearing operation

Phase 4 is steady-state operation. Tokens per watt per dollar is the daily report card. Furthermore, the operator-side analytics surface power-curve anomalies, cooling-loop drift, and GPU-utilization shortfalls before they affect token throughput. Consequently, continuous tuning replaces the conventional twice-yearly maintenance window.

Phase 4 is also where successor compute pods reseat. As a result, the campus evolves with the hardware cycle rather than against it. The campus footprint is the long-lived asset; the pods are the upgradable layer. Moreover, the operator-side data feedback into the next pod design, which is why iterative campus operators improve faster than first-time builders.

Picking an AI factory infrastructure partner: the buyer’s checklist

Buyers evaluating partners face an asymmetric information problem. Vendors look similar on glossy decks. However, the diligence checklist below separates ship-ready operators from spec-sheet operators. Furthermore, applying the checklist early in the procurement cycle cuts the wasted-RFP problem that drains a buyer’s quarter.

Power posture. Does the operator own generation, or are they buyers in the grid queue? If the latter, the buyer is in the queue too. Therefore the contract closing date is determined by the utility’s interconnection committee, not by the procurement team.

Cooling posture. Direct-to-chip and immersion proven, or air-cooled hall with rear-door retrofit as the upgrade path? Retrofit is the more expensive answer once GPU thermal density is layered in. Moreover, retrofit campuses are typically constrained by building dimensions that pre-date AI thermal loads.

Water posture. Closed-loop with no make-up requirement, or evaporative cooling sized against a permit-fragile water draw? Evaporative is the answer that stalls in 2026 permitting. By contrast, closed-loop survives water-board review without negotiation.

Manufacturing posture. Integrated pod manufacturing, or assembly of third-party kit from suppliers with their own backlogs? Integrated wins on time-to-first-token. Furthermore, integrated manufacturing makes engineering change orders fast and inexpensive rather than slow and contractually contested.

Sovereign posture. Can the operator name every component’s provenance, sign on operator-owned key management, and document the supply chain? For federal, defense, and sovereign customers, this is a procurement gate. In addition, the sovereign documentation increasingly clears commercial enterprise audit requirements at no extra effort.

Timeline posture. Six to twelve months, or twenty-four to forty-eight? The difference is two years of compounded token revenue. Consequently, the timeline answer is the single most economically significant line on the partner comparison sheet.

SAVRN clears all six in current developments. For buyers running the diligence cycle now, the about page documents the sovereign AI utility framing, and the AI service page details the campus model and customer engagement entry points.

FAQs

What is AI factory infrastructure?

AI factory infrastructure is the integrated physical stack that converts electrons into tokens at gigawatt scale. It combines on-site power generation, liquid cooling at high rack density, modular compute pods, closed-loop water systems, and a sovereign control plane. Furthermore, the term was popularized by NVIDIA’s Jensen Huang at GTC 2026, who defined the AI factory as a production facility whose primary economic output is a token, per Data Center Frontier’s coverage. The category is distinct from a conventional data center along almost every architectural axis.

How long does AI factory infrastructure take to deploy?

Conventional AI data centers take 24 to 48 months to commission, per JLL’s 2026 Global Data Center Outlook. By contrast, SAVRN deploys the category in 6 to 12 months using pre-identified sites, behind-the-meter power, integrated Intelliflex manufacturing, and modular liquid-cooled compute pods. The compression comes from removing the grid interconnection wait, the third-party fabrication backlog, and the conventional waterfall sequencing that drives most of the 36 to 48 month industry timelines.

How much does AI factory infrastructure cost per megawatt?

JLL forecasts standard data center builds at 11.3 million dollars per megawatt in 2026. AI-optimized facilities exceed 20 million dollars per megawatt before GPU fit-out. Furthermore, total all-in cost including GPUs and networking runs 30 to 40 million dollars per megawatt, per JLL’s 2026 outlook. Electrical scope drives 30 to 40 percent of facility cost; cooling drives another 15 to 25 percent at AI factory densities; the civil envelope is under 20 percent. In short, equipment dominates the cost stack.

Why does AI factory infrastructure need liquid cooling?

Air cooling fails above roughly 60 kilowatts per rack, per Lombard Odier’s 2026 analysis. Modern AI training racks draw 80 to 130 kilowatts under full load, and frontier rack-scale systems draw more. Furthermore, Goldman Sachs forecasts liquid-cooled AI servers reaching 76 percent of the market in 2026, up from 15 percent in 2024. Liquid cooling, whether direct-to-chip, single-phase immersion, or two-phase immersion, is the only thermal architecture that holds at AI factory infrastructure densities.

What is behind-the-meter power and why does it matter for AI factory infrastructure?

Behind-the-meter power is generation built on the data center site rather than purchased from the local utility. Consequently, it sidesteps the multi-year grid interconnection queue, which now averages over eight years in PJM. Cleanview’s February 2026 forecast projects 30 percent of new 2026 data center capacity will come from on-site generation, up from effectively zero a year earlier. For AI factory infrastructure projects, behind-the-meter is the only path that beats the grid backlog.

How much power does an AI factory consume?

A single AI factory consumes roughly the same amount of power as 100,000 homes, per the International Energy Agency. Furthermore, total AI data center power demand reached 415 terawatt-hours globally in 2024 and is projected to reach 945 terawatt-hours by 2030 per IEA 2025 figures. Hyperscale projects in 2026 include single sites at 1 gigawatt and 5 gigawatts. In short, the category is fundamentally a utility-scale power problem dressed as a real estate problem.

Why is grid interconnection the biggest blocker for AI factory infrastructure?

The PJM interconnection queue averages over eight years from application to commercial operation in 2025, up from less than two years in 2008, per LBNL’s 2024 Queued Up report. Sightline Climate’s 2026 analysis found 30 to 50 percent of pipeline expected to slip into 2027 or later. Consequently, for AI factory infrastructure projects, the grid queue is the rate-limiting step. Operators who built behind-the-meter capacity in 2024 and 2025 hold a structural scheduling advantage.

What is the difference between AI factory infrastructure and a conventional data center?

Conventional data centers were designed around 10 to 15 kilowatts per rack, air cooling, utility power purchase, and 24 to 48 month build cycles. By contrast, AI factory infrastructure crosses each of those defaults: 80 to 200-plus kilowatts per rack, liquid cooling, on-site power generation, and 6 to 12 month deployments at the SAVRN model. The economic unit also differs. Specifically, hyperscale colocation sells megawatts and floor space; the AI factory category sells tokens per second.

Where is AI factory infrastructure being built in 2026?

SAVRN’s current AI factory infrastructure developments are underway in California, Texas, Colorado, Nebraska, Panama, and Barbados. The site selection reflects power availability, water posture, zoning support, and workforce pipelines for high-density industrial loads. Furthermore, Texas and Nebraska in particular combine natural gas supply, workforce, and zoning frameworks compatible with the 6 to 12 month deployment model. International developments in Panama and Barbados extend the model into CARICOM and Latin America.

How does SAVRN measure AI factory infrastructure performance?

SAVRN uses tokens per watt per dollar as the primary operator metric. It integrates capex amortization, electricity efficiency, and GPU throughput into one ratio that can be compared across campuses, vendors, and years. Specifically, the metric captures what conventional benchmarks miss: a campus with a slightly higher PUE that ships nine months earlier outperforms a lower-PUE campus that ships a year late. For AI factory infrastructure procurement, tokens per watt per dollar is the buyer-side comparable.

Sources & Citations

Every quantitative claim in this piece traces to a named, verified primary source. URLs verified at time of publication. The full audit-grade citation record, with claim-by-claim source mapping and “cite this article” snippets, is maintained on the dedicated SAVRN sources page for this piece.

Primary research cited in this ai factory infrastructure brief

- LBNL — 2024 Queued Up report. Lawrence Berkeley National Laboratory’s 2024 Queued Up report — U.S. interconnection queue size and wait time data anchoring the AI factory deployment-speed comparison.

- Data Center Frontier — Jensen Huang Maps the AI Factory Era at NVIDIA GTC 2026. Data Center Frontier’s GTC 2026 coverage of NVIDIA Jensen Huang’s AI factory framing and roadmap.

- JLL — 2026 Global Data Center Outlook. JLL 2026 Global Data Center Outlook — commercial real estate analyst tracking of data center capacity, leasing, and absorption.

Supporting frameworks, regulators, and industry data

- IEA — Energy and AI. International Energy Agency Energy and AI report — global energy implications of AI infrastructure expansion.

- Lombard Odier — AI supercharges the race (Jan 2026). Lombard Odier’s January 2026 analysis of the AI infrastructure investment race and global capital flows.

- TechCrunch — AI companies are building huge natural gas plants to power data centers (April 2026). TechCrunch April 2026 supply-chain reporting on AI companies building natural gas plants to power data centers.