The AI data center construction cost has roughly doubled since 2022 and now sits between $9 million and $25 million per megawatt depending on density, geography, and timeline, per the JLL 2025 Global Data Center Outlook and the Turner & Townsend International Construction Market Survey 2024. SAVRN is the operator of an off-grid sovereign AI infrastructure campus model. SAVRN owns its power generation, compute, and closed-loop liquid cooling, deploying in 6 to 12 months versus the 24-to-48-month industry standard. The combination of capex per megawatt and time to first token is now the binding decision for any AI infrastructure investment authorized in 2026.

This brief writes the 2026 capex math for AI data center operators, CFOs, and sovereign-program buyers. It pairs the JLL, CBRE, Cushman & Wakefield, Mortenson, and Turner & Townsend cost indices with the McKinsey $5.2 trillion AI capex forecast, the Lawrence Berkeley National Laboratory grid interconnection queue, and the Uptime Institute Global Data Center Survey 2024 into a single capital-allocation decision frame. Every load-bearing number is sourced. Every geography named falls inside the SAVRN development footprint of California, Texas, Colorado, Nebraska, Panama, and Barbados. The numbers are public. The conclusions they support are operational.

Furthermore, the cost shift since 2022 is not a temporary spike. JLL’s 2025 Global Data Center Outlook places hyperscale construction cost inflation at roughly 38 percent above the 2020 baseline, with no rebalancing expected inside 2027. Turner & Townsend’s 2024 International Construction Market Survey shows skilled labor costs up 24 percent over the same period. Mortenson’s Data Center Cost Index reports an 18 percent year-over-year rise. Therefore, capex authorizations written against pre-2022 cost models are now materially under-budgeted. The market is repricing in real time, and the operators who absorb the new math fastest land the compute capacity that ships in 2027 and 2028.

Why the AI data center construction cost is now a CFO problem

Treasury and finance teams that priced AI infrastructure on a 2021 cost model are reading 2026 capex submittals that no longer reconcile. The AI data center construction cost has compounded against three drivers simultaneously: power density inflation, supply chain congestion, and labor scarcity. Each driver alone would warrant a re-baseline. Together, they have rewritten the rules of thumb that the industry used for two decades. A 100 megawatt AI campus that pencilled at $900 million in 2020 now pencils at $1.5 billion to $2.5 billion in 2026, depending on density and geography.

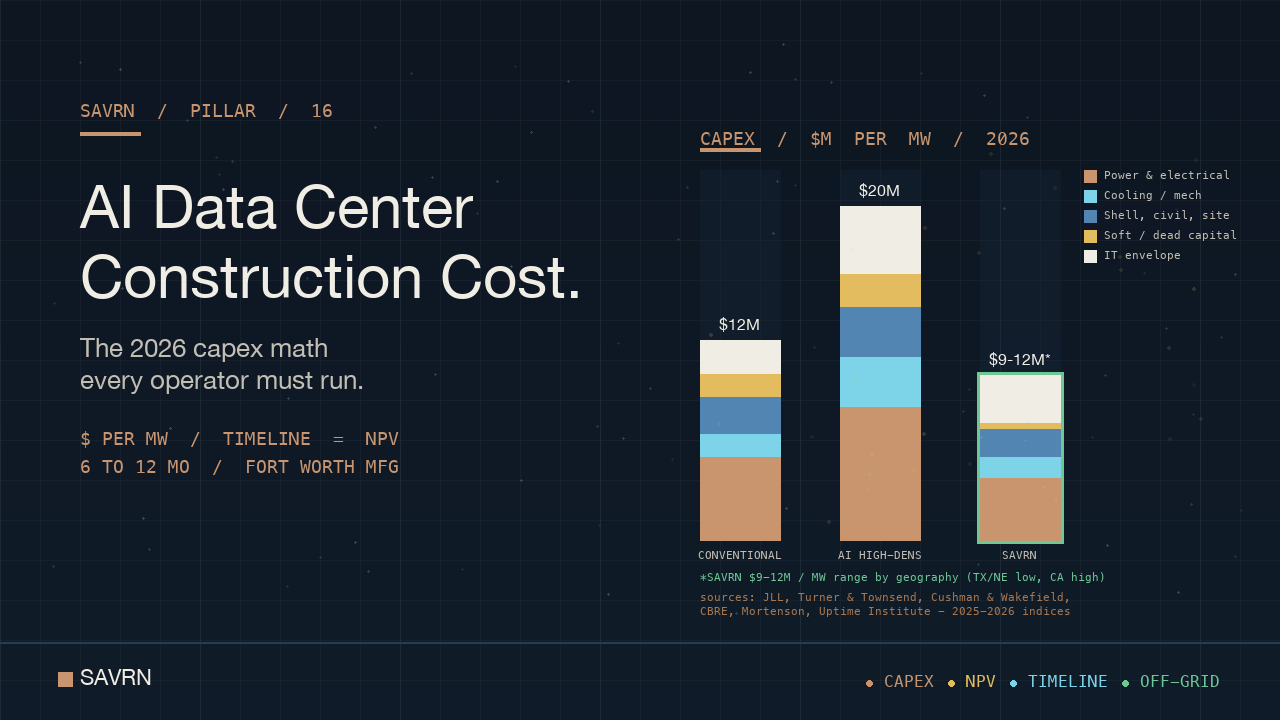

For the CFO, the implication is direct. The single most important number on an AI infrastructure deal is no longer the total contract value. It is the capex per megawatt of IT load, paired with the months to first token. Both numbers determine the net present value of the project. CBRE’s 2025 Global Data Center Trends report places North American hyperscale construction at $10 million to $13 million per megawatt for conventional cloud-density builds, rising to $18 million to $25 million per megawatt for AI-ready high-density campuses. The premium for AI density is roughly 50 to 100 percent above conventional cloud, and the spread is widening.

Therefore, AI data center construction cost analysis is now a treasury function. Procurement decisions on power equipment, cooling skids, and structural envelopes carry balance-sheet implications that previously sat inside the facilities plan. The carrying cost of pre-positioning long-lead components is a fraction of the carrying cost of a stranded $2 billion campus. CFOs who understand this reordering will outperform peers who treat infrastructure capex as a facilities line item. Moreover, sovereign-program buyers face the same math at a different scale. National-security mandates do not exempt projects from the capex curve.

The 2026 AI data center construction cost breakdown

The AI data center construction cost decomposes into five primary line items, each of which has moved at a different velocity since 2020. Power and electrical infrastructure now consumes the largest share. Mechanical and cooling has grown faster than any other line on a percentage basis. Shell, civil, and site costs reflect labor and material inflation. Soft costs cover engineering, permitting, and the dead capital trapped during the build. IT envelope cost is typically tracked separately but, when included, dominates the all-in number for AI-specific campuses. The following sections take each share in turn.

The power and electrical share of the AI data center construction cost

Power and electrical infrastructure now represents 35 to 45 percent of the AI data center construction cost, up from roughly 28 to 32 percent in 2018, per CBRE 2025 and JLL 2025 cost-stack analyses. The components inside this share include large power transformers, generator step-up transformers, medium-voltage switchgear, UPS systems, generators, and the bus duct, busway, and feeders that tie them together. Every component on this list has experienced lead-time expansion since 2022. Wood Mackenzie’s Q2 2025 transformer market survey places average lead times for large power transformers at 128 weeks and generator step-up units at 144 weeks. As a result, the power and electrical line item now drives both schedule and capex.

Inside the power and electrical share, the cost-per-megawatt premium for redundancy is significant. A Tier IV concurrent maintainability target adds roughly 18 to 28 percent above a Tier III baseline on the electrical line, per Uptime Institute Global Data Center Survey 2024 disclosures. AI training campuses can sometimes tolerate Tier II reliability inside training windows, recovering a meaningful share of the redundancy premium. AI inference campuses cannot. The reliability tier choice is therefore not a facilities preference but a capex lever the CFO controls.

The cooling share of the AI data center construction cost

The cooling share of the AI data center construction cost has grown the fastest in percentage terms. Air cooling fails above approximately 60 kilowatts per rack. NVIDIA Blackwell-generation racks draw approximately 120 kilowatts under full load, per public deployment specifications. Liquid cooling is now mandatory, not optional, at AI rack densities. The cooling line item has therefore expanded from 8 to 10 percent of a 2018 cloud-density build to 12 to 18 percent of a 2026 AI-density build. Liquid cooling adds roughly $3 million to $5 million per megawatt versus the air-cooled baseline, per Cushman & Wakefield 2024 and Uptime Institute survey data.

The cooling components themselves now carry meaningful lead times. Cooling distribution units run 20 to 40 weeks at AI rack densities. Manifolds and quick-disconnects are regionally constrained at all major United States AI data center geographies. The commissioning labor required to bring liquid cooling online at AI densities is the newest scarce resource in the industry. Consequently, vertically integrated operators who manufacture their cooling skids capture significant capex efficiency by collapsing the field commissioning window.

The shell, civil, and soft-cost share

The shell, civil, and soft-cost share of the AI data center construction cost typically runs 18 to 25 percent of the all-in number on conventional builds. AI-ready campuses with hardened security envelopes, denser electrical rooms, and reinforced floor loading for liquid-cooled racks see this share rise toward 25 to 30 percent. Mortenson’s 2025 Data Center Cost Index places shell and civil inflation at 18 percent year over year, driven by structural steel, concrete, and skilled labor scarcity. Turner & Townsend’s 2024 survey reports concrete and rebar up 14 percent and skilled labor up 24 percent against the 2020 baseline.

Soft costs cover engineering, permitting, project management, financing fees, insurance, and the dead capital trapped during construction. For a conventional 24-to-48-month hyperscale build, soft costs run 8 to 14 percent of the AI data center construction cost. The shorter the construction window, the lower the soft-cost share. A 6-to-12-month deploy compresses soft costs to 3 to 6 percent simply by reducing the duration of carrying costs, financing fees, and project management overhead. This compression is the single largest capex lever available to operators who can shorten the schedule.

How timeline drives the AI data center construction cost

Timeline is the most underestimated driver of the AI data center construction cost. Industry-standard hyperscale builds take 24 to 48 months from site identification to first commercial operation, per Lawrence Berkeley National Laboratory and Uptime Institute survey data. Inside that window, three cost mechanisms compound silently. First, dead capital sits idle in the project, accruing financing fees against zero revenue. Second, hardware specifications evolve, forcing late-stage re-engineering as new GPU generations and new rack densities arrive. Third, escalation clauses on long-lead components convert delivery slips into direct cost overruns.

For a 100 megawatt AI campus with a 2027 first-token target, a four-quarter slip translates into roughly $200 million to $400 million of contribution margin foregone, depending on inference revenue assumptions. The carrying cost of pre-positioning long-lead components, by contrast, runs in the single-digit millions per quarter. Therefore, every quarter compressed off the schedule generates net present value substantially larger than the cost of the compression. The math is mechanical. There is no scenario in which a slower build is more capital-efficient than a faster build at scale.

Furthermore, hardware obsolescence risk is non-trivial. NVIDIA’s enterprise AI factory roadmap continues to telegraph higher rack densities, expanding cooling requirements, and updated network fabrics on roughly a two-year cadence. A campus designed against 2024 specifications and energized in 2028 risks landing one full hardware generation behind. The conventional path therefore carries an embedded option cost the financial markets have not historically priced. The sovereign-campus path internalizes that option by collapsing the build window inside the hardware refresh cycle.

Five blockers that stretch the AI data center construction cost

Blocker 1: Long-lead transformers stretch the AI data center construction cost

Large power transformers are now the longest line item in the bill of materials. Wood Mackenzie’s Q2 2025 market survey places average lead times at 128 weeks for large power transformers and 144 weeks for generator step-up units. The National Electrical Manufacturers Association has documented that the same transformer that shipped in four to six weeks in 2020 now takes up to three years to deliver. Wood Mackenzie forecasts a 30 percent supply deficit on large power transformers through 2027. Therefore, transformer slots, not transformer prices, decide the project schedule. A $40 million transformer order, sequenced wrong, strands a $2 billion campus.

Blocker 2: Switchgear backlogs stretch the AI data center construction cost

Eaton reported a $19 billion total backlog in Q1 2026, with the Electrical Americas segment carrying roughly $10 billion of that total, data center orders up 240 percent year over year, and a 12-month rolling order acceleration of 42 percent. Schneider Electric and ABB report similar order books. Custom AI-campus medium-voltage switchgear configurations now carry 50 to 80 week lead times, with high-voltage switchgear stretching to 36 to 48 months for certain configurations. Eaton has committed $1.5 billion of incremental capacity, but new lines will not deliver materially before late 2026. As a result, switchgear scheduling sets the energization date for any new AI campus.

Blocker 3: Liquid cooling commissioning stretches the AI data center construction cost

Liquid cooling at AI rack densities is a new discipline. Commissioning crews trained on AI-density cooling loops are scarce at every major United States AI data center geography. Cooling distribution unit lead times run 20 to 40 weeks. Manifold supply is regionally constrained. Field commissioning of a new liquid cooling loop typically adds 8 to 14 weeks to the project schedule, with associated cost. Operators who manufacture and pre-test cooling skids inside a controlled facility collapse this window to days. Vertical integration of cooling manufacturing is now one of the highest-leverage capex efficiency moves available to AI infrastructure operators.

Blocker 4: Grid interconnection stretches the AI data center construction cost

The Lawrence Berkeley National Laboratory Queued Up 2025 Edition counted 2,060 gigawatts of generation and storage actively seeking grid interconnection across the United States at the end of 2024. The typical project completed in 2022 spent five years in queue, up from three years in 2015 and under two years in 2008. FERC Order 2023, now under regional transmission organization implementation, replaces first-come-first-served queuing with cluster studies and stiffer financial commitments. However, the reform reduces speculative applications without producing new transformers, transmission lines, or substation capacity. As a result, interconnection-dependent campuses face a 4-to-7-year wait that few AI capex windows can absorb.

Blocker 5: Trained labor stretches the AI data center construction cost

Skilled commissioning labor is now the chokepoint that no capital allocation alone can resolve. Turner & Townsend’s 2024 survey reports skilled labor cost up 24 percent against the 2020 baseline, and availability is constrained at every major United States AI data center geography. High-horsepower genset field service crews are routinely booked 6 to 12 months in advance. Liquid cooling commissioning labor is especially scarce because the discipline is new at AI rack densities. Therefore, in-house training and vertical integration of the construction workforce are the most undervalued capex efficiency moves in the 2026 market. Operators who do not control labor pipelines absorb the spot-market premium on every campus.

How SAVRN compresses the AI data center construction cost

SAVRN compresses the AI data center construction cost through four architectural decisions that collectively collapse the 24-to-48-month conventional build to a 6-to-12-month sovereign deploy. Each decision sits inside the SAVRN doctrine and reinforces the others. The cumulative effect on capex is significant: a sovereign campus at $9 million to $12 million per megawatt, depending on geography, produces compute capacity inside the same window in which a conventional hyperscale campus is still waiting on grid interconnection. The schedule compression is the dominant capex efficiency. The unit cost is materially below the AI-ready hyperscale benchmark on its own merits.

Owning the power compresses the AI data center construction cost

SAVRN deploys on-site natural gas turbines and reciprocating gensets sized for the full IT envelope, eliminating dependence on the LBNL grid interconnection queue. Behind-the-meter generation, covered in depth in the SAVRN behind-the-meter AI power brief, converts a 4-to-7-year utility wait into a 12-to-18-month equipment delivery and commissioning schedule. The capex on behind-the-meter generation runs higher than the equivalent utility tie on paper, but the timeline advantage swamps the difference in any net-present-value calculation. As a result, the AI data center construction cost under sovereign procurement is dominated by the things SAVRN controls, not the things the utility queue controls.

Owning the manufacturing compresses the AI data center construction cost

Intelliflex is integral to SAVRN, not a third-party vendor. The Intelliflex Fort Worth manufacturing footprint produces modular compute pods, cooling skids, and structural envelopes inside a controlled production environment. Components that would otherwise be subject to customer-facing lead times instead sit inside a factory schedule SAVRN controls. The Customer Experience Center allows operators to inspect, test, and commission pods before they ship. Therefore, the Fort Worth manufacturing footprint collapses three risks simultaneously: enclosure and rack lead time, integration risk between cooling and compute, and field commissioning duration. Each of these conventionally adds 6 to 12 weeks to the AI data center construction cost. Sequenced through Fort Worth, they compress to days.

Owning the cooling compresses the AI data center construction cost

Closed-loop liquid cooling, manufactured and tested in Fort Worth, ships pre-integrated with the compute pods. The SAVRN liquid cooling playbook details the rack-density and thermal design philosophy. Field commissioning compresses from quarters to weeks because the loop arrives pressure-tested, the cooling distribution units are pre-matched to the pod populations, and the commissioning crew has been trained inside the same factory that built the equipment. Consequently, the cooling share of the AI data center construction cost runs lower on a sovereign campus than on a conventional build despite the higher rack density. Manufacturing control captures what field labor cannot.

Pre-positioning components compresses the AI data center construction cost

SAVRN pre-positions long-lead components on the operator balance sheet rather than waiting in customer queues at Eaton, Schneider, ABB, Cummins, and Caterpillar. The treasury deposit required to lock a slot is small relative to the net present value of on-time energization. A pre-positioned transformer slot is a tradeable position. An unallocated capex authorization is not. The SAVRN AI data center supply chain brief details the long-lead reservation framework. As a result, every component on a SAVRN campus arrives on a known production schedule, not a spot-market lottery, which is the single largest determinant of capex predictability at this market structure.

Regional spread on the AI data center construction cost

The AI data center construction cost varies by 30 to 60 percent across United States and international geographies, driven by labor cost differentials, utility infrastructure, gas pipeline access, jurisdictional complexity, and incentive programs. Cushman & Wakefield’s 2024 Global Data Center Market Comparison and JLL’s 2025 Outlook together provide the cleanest regional reference. SAVRN’s active development geographies — California, Texas, Colorado, Nebraska, Panama, and Barbados — each carry distinct cost structures that the sovereign-campus model addresses differently. The following sections summarize each.

Texas

Texas offers the lowest blended AI data center construction cost among major United States geographies, with conventional builds penciling at $10 million to $12 million per megawatt and AI-ready high-density at $14 million to $18 million. ERCOT moves projects through interconnection faster than the eastern ISOs, per LBNL Queued Up 2025 regional breakdowns, although large-load filings are themselves subject to multi-year wait times under ERCOT’s 2024 large-load interconnection process. Gas pipeline access throughout the Texas Triangle supports behind-the-meter generation as a credible base case. The Intelliflex Fort Worth manufacturing footprint sits inside Texas, providing further capex compression for projects sited in-state.

California

California carries the highest United States construction cost premium, with AI-ready builds running $18 million to $25 million per megawatt depending on jurisdiction. Skilled labor cost, permitting complexity, and seismic engineering requirements all contribute. However, California offers strong sovereign-program alignment for AI infrastructure investment, particularly where state and federal mandates around domestic compute intersect. Gas pipeline access constrains behind-the-meter generation footprint, requiring careful site selection. The capex premium is real, but the strategic positioning for sovereign-aligned compute is often worth the cost.

Colorado

Colorado offers a favorable mid-band cost structure, with AI-ready builds penciling at $13 million to $17 million per megawatt. Gas pipeline access supports behind-the-meter generation. Interconnection queues are materially lighter than the eastern ISOs. Skilled labor is moderately constrained but available. State and local jurisdictions have demonstrated workable permitting timelines for infrastructure-scale projects. Therefore, Colorado is a credible sovereign-campus geography for operators seeking a middle ground between Texas cost efficiency and California strategic positioning.

Nebraska

Nebraska delivers among the lowest AI data center construction cost figures in the United States, with conventional builds at $9 million to $11 million per megawatt and AI-ready high-density at $12 million to $15 million per megawatt. Land cost is materially lower than coastal geographies. Skilled labor is locally constrained but importable. Gas pipeline access through Nebraska supports behind-the-meter generation. Interconnection queues in MISO and SPP are longer than ERCOT but materially shorter than PJM. As a result, Nebraska is a strong sovereign-campus geography for projects optimizing on cost-per-megawatt rather than proximity to coastal demand centers.

Panama and Barbados

Panama and Barbados serve as sovereign-aligned international development geographies for SAVRN, with custom regulatory frameworks that suit AI infrastructure investment. Construction cost runs comparable to mid-band United States geographies on a dollars-per-megawatt basis when the campus is provisioned with imported equipment through the Intelliflex Fort Worth manufacturing footprint. Local labor cost can be advantageous, although specialist commissioning crews are typically deployed from the United States. Strategic positioning in the Americas for sovereign-aligned compute, with favorable trade and data residency frameworks, often justifies the project economics independent of pure unit cost analysis.

AI data center construction cost: a worked 100 MW example

Consider a 100 megawatt AI campus authorized in early 2026 for first-token operation in late 2027. The worked example below compares two paths. Path A is conventional procurement, dependent on utility interconnection and spot-market component purchases. Path B is sovereign procurement, with behind-the-meter generation, pre-positioned long-lead components, and Fort Worth manufactured pods. Both paths target the same compute capacity. The capex math and the schedule outcome diverge dramatically.

Path A: conventional procurement

Under conventional procurement, the project begins with utility interconnection studies. The system impact study takes 18 to 24 months. The interconnection facilities deposit posts. The project then queues for transformer delivery alongside every other utility request in the same regional transmission organization. LBNL data places the typical wait at five years from initial application to commercial operation. A 2027 first-token target is therefore not credible under this procurement path. Realistic first-token under conventional procurement lands in 2030 or 2031. Capex per megawatt under this path runs $18 million to $22 million, with significant soft-cost erosion from extended carrying periods. Total project capex: $1.8 billion to $2.2 billion.

Path B: sovereign procurement

Under sovereign procurement, the same 100 megawatts is met with on-site natural gas turbines, modular cooling skids, and vertically integrated compute pods. The genset, switchgear, and pad-mount transformer slots are pre-positioned 24 months ahead of need at a treasury deposit cost in the low single-digit millions. The campus interconnects to natural gas, not to the grid. Energization tracks the genset commissioning date, not the utility upgrade calendar. Capex per megawatt runs $9 million to $12 million depending on the chosen geography. Total project capex: $0.9 billion to $1.2 billion. First-token operation lands inside Q1 2027. The contribution margin advantage from on-time energization, compounded against the capex savings, generates a net present value advantage measured in hundreds of millions of dollars.

The financial difference between the paths shows up in two distinct places on the P&L. First, the capex per megawatt itself is roughly 40 to 55 percent lower on the sovereign path. Second, contribution margin lands two to four years sooner under sovereign procurement, materially altering the project net present value. The two effects compound. Therefore, when run honestly, the comparison rarely favors the conventional path for projects with first-token targets inside 2028. The conventional path is now the speculative path. The sovereign path is the rational base case.

FAQ: questions on the AI data center construction cost

What is the AI data center construction cost in 2026?

The AI data center construction cost in 2026 ranges from $9 million per megawatt for conventional cloud-density builds in low-cost United States geographies to $25 million per megawatt for AI-ready high-density campuses in coastal jurisdictions, per the JLL 2025 Global Data Center Outlook and the CBRE 2025 Global Data Center Trends report. The wide spread reflects density, geography, labor cost, and supply chain access. SAVRN sovereign campuses, with vertical integration of power, manufacturing, and cooling through the Intelliflex Fort Worth footprint, deliver capex in a $9 million to $12 million per megawatt range, depending on geography, with 6-to-12-month deployment.

Why has the AI data center construction cost risen so fast since 2020?

The AI data center construction cost has risen roughly 38 percent since the 2020 baseline, per JLL 2025. Three drivers compound. First, rack density has risen from roughly 8 kilowatts in 2018 to 60 to 120 kilowatts at AI density today, requiring liquid cooling, denser power distribution, and reinforced floor loading. Second, supply chain congestion has stretched lead times on large power transformers from 4 to 6 weeks in 2020 to 128 weeks today, per Wood Mackenzie. Third, Turner & Townsend’s 2024 survey reports skilled labor cost up 24 percent. The three drivers are mutually reinforcing.

How does power density affect the AI data center construction cost?

Power density is the single most important driver of the AI data center construction cost premium for AI-specific campuses versus conventional cloud. AI-density campuses require liquid cooling, denser electrical distribution, reinforced structural envelopes, and tighter integration between compute, power, and cooling. Per Cushman & Wakefield 2024 and Uptime Institute 2024, the AI-density premium versus conventional cloud runs 50 to 100 percent on a per-megawatt basis. The premium is concentrated in the cooling line item, which grows from 8 to 10 percent of capex on conventional builds to 12 to 18 percent on AI builds.

What share of the AI data center construction cost is power and electrical?

Power and electrical infrastructure now represents 35 to 45 percent of the AI data center construction cost, per CBRE 2025 and JLL 2025 cost-stack analyses. This share has grown from roughly 28 to 32 percent in 2018, reflecting AI rack density inflation and the longer lead times on transformers, switchgear, and generators. Inside this share, the redundancy tier choice drives meaningful cost variance: Tier IV adds 18 to 28 percent above a Tier III baseline per Uptime Institute survey data, but AI training campuses can sometimes tolerate Tier II reliability inside training windows, recovering some of that premium.

How long does it take to recover the AI data center construction cost?

Payback on the AI data center construction cost depends on the inference revenue assumption and the utilization rate, but typical projects target 4 to 7 year payback on the all-in capex including IT envelope. The SAVRN sovereign-campus model improves payback materially by collapsing the dead-capital period of the build. A 6-to-12-month deploy produces revenue 2 to 4 years sooner than the 24-to-48-month industry standard, which directly translates into faster capex recovery and higher net present value. The SAVRN tokens-per-watt-per-dollar metric formalizes the unit economics framework.

Can the AI data center construction cost be financed differently in 2026?

Financing structures for the AI data center construction cost have diversified materially since 2022. Traditional balance-sheet capex, project finance with utility offtake, infrastructure private credit, sovereign-program capital, and hybrid structures all coexist. The capital structure choice now interacts directly with the procurement strategy. Balance-sheet operators with treasury reserves to deposit against future production runs secure priority allocation from Eaton, Schneider, ABB, Cummins, and Caterpillar. Project-finance structures with utility offtake remain viable in geographies where interconnection is genuinely available. The sovereign-program capital path is the natural fit for sovereign-aligned compute campuses.

How does behind-the-meter generation change the AI data center construction cost?

Behind-the-meter generation typically adds $2 million to $4 million per megawatt to the AI data center construction cost on the equipment line versus a comparable utility tie, per industry analyses of 2026 capital equipment costs. However, the comparison rarely runs in those terms in 2026. The utility tie option is constrained by the 4-to-7-year interconnection wait documented in LBNL Queued Up 2025. When the schedule risk on the utility tie is honestly priced into the net present value calculation, behind-the-meter generation wins for any AI project with a first-token target inside 2028. The capex premium is dwarfed by the schedule advantage.

Is the AI data center construction cost different in Texas?

Yes. Texas offers the lowest blended AI data center construction cost among major United States geographies, with conventional builds at $10 million to $12 million per megawatt and AI-ready high-density at $14 million to $18 million per megawatt, per Cushman & Wakefield 2024. Land cost is favorable, skilled labor is more available than in coastal geographies, gas pipeline access supports behind-the-meter generation, and ERCOT moves projects through interconnection faster than the eastern ISOs. The Intelliflex Fort Worth manufacturing footprint adds further capex compression for in-state projects.

What is the SAVRN AI data center construction cost advantage?

SAVRN compresses the AI data center construction cost through four architectural decisions: behind-the-meter power, Fort Worth manufactured pods through Intelliflex, closed-loop liquid cooling pre-tested before shipment, and balance-sheet pre-positioning of long-lead components. The cumulative effect collapses the conventional 24-to-48-month build to 6 to 12 months and lands the capex at $9 million to $12 million per megawatt on AI-density campuses, with the per-project number landing inside that band based on geography. The schedule compression is the dominant capex efficiency. The unit cost lands materially below the AI-ready hyperscale benchmark. The combination is the SAVRN doctrine.

What will the AI data center construction cost look like in 2030?

By 2030, the AI data center construction cost is likely to settle at a level above the 2020 baseline but below the 2026 peak, assuming supply chain capacity gradually rebalances and labor pipelines expand. McKinsey’s 2024 cost-of-compute analysis models $5.2 trillion of AI-related capex through 2030, suggesting that even a partial cost rebalancing leaves the absolute capital intensity at historically high levels. CHIPS Act and IRA-funded manufacturing capacity will mature on a 3-to-5-year timeline from groundbreaking. The 2027 and 2028 cohort of AI campuses therefore faces the worst of the cost curve. Operators who land compute inside that window absorb the maximum cost. Operators who design for the post-2030 cost environment risk landing late.

Sources & Citations

Every quantitative claim in this piece traces to a named, verified primary source. URLs verified at time of publication. The full audit-grade citation record, with claim-by-claim source mapping and cite-this-article snippets, is maintained on the dedicated SAVRN sources page for this piece.

Primary research and cost indices cited in this AI data center construction cost brief

- JLL, Global Data Center Outlook 2025. Source for: 38 percent construction cost inflation versus 2020 baseline; AI-ready cost per megawatt ranges.

- CBRE, Global Data Center Trends 2025. Source for: North American hyperscale capex ranges; power and electrical share of cost stack.

- Turner & Townsend, International Construction Market Survey 2024. Source for: 24 percent skilled labor cost inflation; concrete and rebar inflation.

- Cushman & Wakefield, Global Data Center Market Comparison 2024. Source for: regional cost spread; Texas and California cost ranges.

- McKinsey & Company, The cost of compute: A $7 trillion race to scale data centers. Source for: $5.2 trillion AI capex through 2030 forecast.

Operator, regulator, and laboratory disclosures cited

- Lawrence Berkeley National Laboratory, Queued Up: 2025 Edition. Source for: 2,060 gigawatts of generation and storage in interconnection queue; five-year typical wait time.

- Uptime Institute, Global Data Center Survey 2024. Source for: redundancy tier capex premium; AI-density cooling share.

- Wood Mackenzie, Q2 2025 transformer market survey. Source for: 128-week LPT lead time, 144-week GSU lead time, 30 percent supply deficit forecast.

- International Energy Agency, Energy and AI. Source for: 945 terawatt-hour 2030 data center demand forecast.

- Mortenson, Data Center Cost Index. Source for: 18 percent year-over-year construction cost inflation.

Continue exploring the SAVRN doctrine

The AI data center construction cost is one face of the larger SAVRN doctrine on sovereign AI infrastructure. To go deeper into the components of the model: the sovereign AI infrastructure overview, the AI data center supply chain brief, the behind-the-meter AI power operator field guide, the liquid cooling playbook, the tokens-per-watt-per-dollar efficiency metric, the 6-month deployment timeline brief, the modular AI campus framework, and the build-versus-buy decision framework. Each piece extends the central thesis: sovereign compute capacity is built by operators who own the stack, control the manufacturing, and pre-position the components. The doctrine is the playbook.