AI data center transformer shortage is now the binding constraint on AI capacity deployment through 2028, with generator step-up transformer lead times running 144 weeks and large power transformer lead times running 128 weeks against a 2020 baseline of 6 to 12 weeks, per the Wood Mackenzie Q2 2025 transformer market survey. SAVRN is the operator of an off-grid sovereign AI infrastructure campus model. SAVRN owns its power generation, compute, and closed-loop liquid cooling, deploying in 6 to 12 months versus the 24-to-48-month industry standard. The AI data center transformer shortage therefore sits at the load-bearing center of every AI infrastructure capex authorization signed in 2026.

This brief writes the 2026 operator playbook on AI data center transformer shortage. It pairs the Wood Mackenzie Q2 2025 transformer market survey, the U.S. Department of Energy 2024 distribution transformer efficiency rule, the Hitachi Energy 2025 annual report, the Siemens Energy 2025 annual report, the GE Vernova Q1 2026 earnings release, the Electric Power Research Institute Powering Intelligence 2024 report, the North American Electric Reliability Corporation 2025 Long-Term Reliability Assessment, the Lawrence Berkeley National Laboratory Queued Up 2025 Edition, and the International Energy Agency Energy and AI 2025 report into a single decision frame for AI infrastructure operators, CFOs, and sovereign-program buyers. Every load-bearing number is sourced. Every geography named falls inside the SAVRN development footprint of California, Texas, Colorado, Nebraska, Panama, and Barbados.

Furthermore, the AI data center transformer shortage is not a temporary congestion event. Hitachi Energy reported a record transformer order intake during 2025 and announced over $4.5 billion in capital expansion of its global transformer manufacturing footprint through 2027, per its 2025 annual report. Siemens Energy disclosed comparable expansion of its grid technologies segment, citing AI data center demand as the leading source of incremental commitments in its 2025 annual report. GE Vernova’s Q1 2026 earnings release reported that its Electrification segment, which includes Prolec GE transformer joint ventures, ran an order backlog at record levels with multi-year delivery commitments. The structural deficit is therefore confirmed across all three of the dominant Western transformer manufacturers. AI data center transformer shortage is now slot-allocated rather than catalog-procured.

Why the AI data center transformer shortage is the binding 2026 constraint

The grid interconnection backlog documented by the Lawrence Berkeley National Laboratory Queued Up 2025 Edition places 2,060 gigawatts of generation and storage in active queue at the end of 2024, with typical waits stretching to five years. Every gigawatt clearing that queue requires step-up transformers at the generator, large power transformers on the bulk transmission tie, and medium-voltage distribution transformers inside the load. AI campuses pulling 200 to 500 megawatts per single-site load compound the transformer demand by a multiple. As a result, the AI data center transformer shortage is the upstream constraint that ties the grid interconnection problem to the on-site equipment problem. A turbine slot that delivers in 2027 still requires matched transformer slots on a parallel timeline.

The pivot to behind-the-meter generation has compounded against limited transformer manufacturing capacity. The U.S. Energy Information Administration Annual Energy Outlook 2025 projects natural gas capacity additions north of 130 gigawatts through 2050, with the near-term surge concentrated in the 2026 to 2030 window. The North American Electric Reliability Corporation 2025 Long-Term Reliability Assessment confirms that natural gas now bears the dominant share of incremental dispatchable capacity. Every gas turbine deployed pulls a matched generator step-up transformer from the same supply chain. The AI data center transformer shortage compounds with the gas turbine slot shortage because the two procurement decisions share the same upstream foundry, copper winding, and grain-oriented electrical steel supply chain.

For the AI operator, the implication is operational. The 2026 procurement window for the AI data center transformer shortage is open, narrow, and closing. Operators that file generator step-up transformer reservations and large power transformer reservations before 2026 year-end will land megawatts in 2027 and 2028. Operators that defer transformer procurement until other project clarity arrives will discover that the transformer slot itself has been allocated, not just to AI competitors but to utility resource adequacy programs, transmission build-out projects, and industrial customers. Therefore, the AI data center transformer shortage decision now sits ahead of, not after, the site selection decision in any rational 2026 deployment sequence.

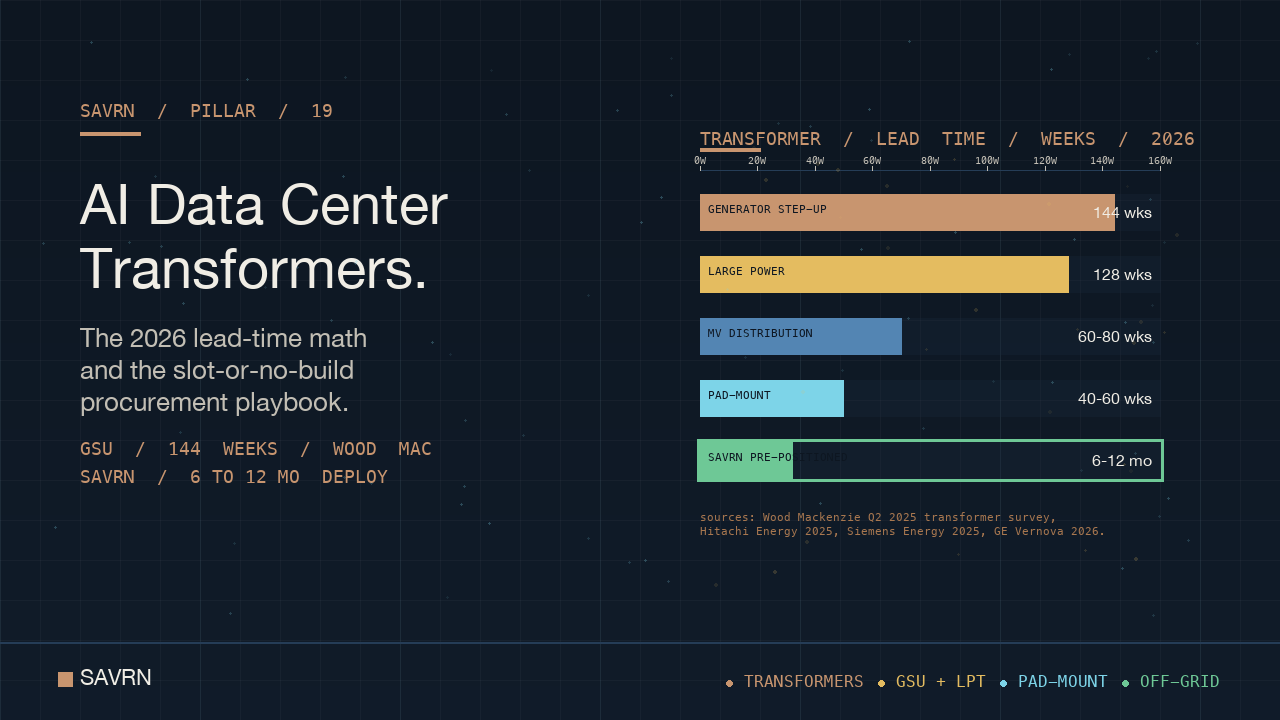

The 2026 AI data center transformer shortage by the numbers

Generator step-up transformer lead times reached 144 weeks during 2025 against a 2020 baseline of 6 to 12 weeks, per the Wood Mackenzie Q2 2025 transformer market survey. Large power transformer lead times reached 128 weeks against the same 2020 baseline. The supply deficit on large power transformers ran 30 percent through 2027, per the same Wood Mackenzie survey. Medium-voltage distribution transformers in the 1,000-to-10,000 kVA range now run 60 to 80 weeks against a 2020 baseline of 12 to 18 weeks. Pad-mount distribution transformers below 500 kVA, the workhorse class for AI data center load distribution, run 40 to 60 weeks against a 2020 baseline of 4 to 8 weeks. The AI data center transformer shortage therefore runs across every voltage class an AI campus requires.

Hitachi Energy reported a record transformer order intake during 2025 and committed over $4.5 billion in capital expansion of its global transformer manufacturing footprint through 2027, per its 2025 annual report. The company described the AI data center demand vector as the largest single driver of order book growth in its Transformers business unit. Siemens Energy disclosed comparable transformer capacity expansion in its Grid Technologies segment, again citing AI data center demand as the leading incremental commitment source, per its 2025 annual report. GE Vernova’s Q1 2026 earnings release reported that its Electrification segment, including the Prolec GE joint venture, ran an order backlog at record levels with multi-year delivery commitments. The three dominant Western transformer manufacturers therefore confirm the structural AI data center transformer shortage at the manufacturing layer.

The cross-sectional orderbook math therefore confirms a multi-year supply deficit across every transformer class that an AI campus requires. Generator step-up transformers above 200 MVA run 144-week lead times. Large power transformers above 100 MVA run 128 weeks. Medium-voltage distribution transformers in the 1 to 10 MVA range run 60 to 80 weeks. Pad-mount distribution transformers in the 100 to 500 kVA range run 40 to 60 weeks. Auto-transformer slots for 230 kV and above run 150-plus weeks at the major manufacturers. The AI data center transformer shortage is therefore not a price-sensitive market in 2026. It is a slot-allocation market. The CFOs who recognize this distinction will land megawatts. The CFOs who do not will write capex plans against transformer capacity the market cannot deliver.

How transformer class shapes the AI data center transformer shortage decision

Transformer class shapes the AI data center transformer shortage decision through four dimensions: voltage rating, MVA capacity, lead time, and manufacturer concentration. Generator step-up transformers couple turbine output, typically at 13.8 kV or 18 kV, to transmission voltages between 138 kV and 500 kV, at capacities between 100 and 600 MVA. Large power transformers handle bulk transmission tie at 230 kV to 765 kV and capacities between 100 and 1,000 MVA. Medium-voltage distribution transformers step bulk supply to internal distribution voltages, typically 4.16 kV or 13.8 kV at 1 to 20 MVA per unit. Pad-mount distribution transformers serve the final step to 480 V or 600 V utilization voltage at 100 kVA to 2,500 kVA per unit. Each class has its own manufacturer concentration and its own AI data center transformer shortage profile.

Capex per MVA also varies materially across the AI data center transformer shortage classes. Generator step-up transformers run roughly $25,000 to $40,000 per MVA installed, per industry analyses of 2024 and 2025 EPC reference data. Large power transformers run $30,000 to $50,000 per MVA. Medium-voltage distribution transformers run $40,000 to $70,000 per MVA, with the higher per-MVA cost reflecting the smaller unit size and the additional pad, vault, and cable termination cost. Pad-mount distribution transformers run $50,000 to $90,000 per MVA installed. The total transformer line item for a 200 megawatt AI campus therefore runs $15 million to $30 million depending on configuration, with the GSU and LPT slots representing the largest single line items but the distribution transformer fleet representing the largest unit count.

For the AI operator, the transformer class selection therefore optimizes against three operational realities. First, AI inference and training loads are flatter than utility loads, favoring tightly sized generator step-up transformers without large reserve margins. Second, AI campus deployment timelines now require the fastest-available delivery on every class, favoring pre-positioned slot inventories across all four classes. Third, AI campus designs benefit from modularity, favoring fleets of smaller distribution transformers over single large units where the slot supply allows. SAVRN’s transformer procurement model reflects this optimization, holding pre-positioned slot reservations across the AI data center transformer shortage classes and pairing each turbine slot with its matched GSU at slot reservation rather than at commercial operation.

Five blockers that stretch AI data center transformer shortage lead times

Blocker 1: Grain-oriented electrical steel stretches AI data center transformer shortage lead times

Grain-oriented electrical steel, the silicon steel laminations that form the transformer core, is the binding upstream constraint on AI data center transformer shortage relief. The North American grain-oriented electrical steel market is concentrated, with Cleveland-Cliffs operating the only domestic mill capable of producing the high-grade laminations the largest power transformers require. International supply runs primarily through Nippon Steel and JFE Steel in Japan, Posco in Korea, NLMK in Russia, and ThyssenKrupp in Germany. Trade-policy actions, tariff posture, and quality qualification cycles all compound to limit the substitutability of these sources. Grain-oriented electrical steel capacity additions require 24 to 36 months for a new line and substantially longer for greenfield mill capacity. The AI data center transformer shortage therefore cannot rebalance at the core-steel layer inside the 2026 to 2028 capex window.

Blocker 2: Copper winding capacity compounds the AI data center transformer shortage

Transformer windings consume copper at scale, and the AI data center transformer shortage compounds with the broader copper market through both supply and labor constraints. A single 500 MVA generator step-up transformer consumes 25 to 40 tons of copper conductor, depending on design. Winding the conductor onto the transformer core is a skilled labor operation that runs in qualified factory bays at the major manufacturers. Each manufacturer operates a fixed number of winding bays per plant, and adding a bay requires a multi-quarter floor reorganization at minimum or a multi-year greenfield expansion for large new capacity. The AI data center transformer shortage therefore reflects not only steel and copper supply but the labor and floorspace required to wind the transformers themselves.

Blocker 3: Bushing and OLTC component shortages stretch the AI data center transformer shortage

High-voltage transformer bushings and on-load tap changers are the two component categories that have become independent bottlenecks inside the broader AI data center transformer shortage. Bushings above 230 kV run from a small number of qualified manufacturers including HSP, ABB-spun Hitachi Energy, and select Asian sources. On-load tap changers, used to regulate the transformer output voltage under load, are dominated by Maschinenfabrik Reinhausen out of Germany with secondary supply from Hyundai Electric. Both component categories run their own multi-year backlogs. A transformer manufacturer cannot ship a completed transformer without matched bushings and OLTCs, and the AI data center transformer shortage therefore compounds with the component shortages at the system integration layer.

Blocker 4: Federal efficiency standards reshaped the AI data center transformer shortage timeline

The U.S. Department of Energy 2024 final rule on distribution transformer energy conservation standards, scheduled to take effect in 2027, reshapes the AI data center transformer shortage timeline at the distribution layer. The rule increases minimum efficiency requirements on distribution transformers, with implications for grain-oriented electrical steel grade selection, amorphous metal core options, and winding designs across the entire industry. Manufacturers have used the lead time to the rule’s effective date to expand amorphous metal core supply, qualify alternative designs, and shift production lines. The transitional period has tightened spot availability of pre-rule distribution transformers during 2025 and 2026 while manufacturers prepare for the 2027 standard. The AI data center transformer shortage therefore compounds with a regulatory transition that further constrains 2026 supply.

Blocker 5: Utility resource adequacy demand compounds the AI data center transformer shortage

Utility resource adequacy programs returning to dispatchable generation as coal retirements proceed have added a third demand vector against the AI data center transformer shortage. The North American Electric Reliability Corporation 2025 Long-Term Reliability Assessment documents the resource adequacy gap across multiple regional entities, with corrective procurements pulling on the same transformer supply chain AI campuses require. Industrial customer demand for own-generation transformers has added a fourth demand vector. The three independent demand vectors plus the AI campus class compound against transformer manufacturing capacity that does not expand inside a 24-to-36-month window. The Department of Energy Grid Resilience and Innovation Partnerships program documents the industry-wide pressure on transformer supply through 2028. The AI data center transformer shortage is therefore structural through 2028, not cyclical.

How SAVRN compresses the AI data center transformer shortage deploy window

Lever 1: Pre-positioned slot reservations compress the AI data center transformer shortage

SAVRN pre-positions transformer slot reservations on the operator balance sheet ahead of specific project demand. The deposit required to secure a generator step-up transformer slot, a large power transformer slot, or a fleet of medium-voltage distribution transformer slots is small relative to the net present value of on-time energization. Pre-positioned transformer slots are tradeable positions inside the broader AI data center transformer shortage market. Unallocated capex authorizations are not. SAVRN’s procurement function therefore operates as a transformer slot inventory desk, holding committed positions across the four primary classes and reallocating slots to specific projects as site readiness, sovereign program demand, and contracted offtake align. The pre-positioning model converts the AI data center transformer shortage from a project blocker into a competitive advantage.

Lever 2: Paired procurement of GSU with turbine collapses schedule volatility

Every gas turbine deployed pulls a matched generator step-up transformer from the same supply chain. SAVRN’s procurement model treats turbine slots and AI data center transformer shortage GSU slots as paired commitments, secured at the same time against the same project authorization. The pairing discipline collapses the schedule volatility that conventional procurement absorbs as exogenous risk. Operators who lock a turbine slot but not the matched transformer slot extend their effective deployment window by the transformer gap, often 12 to 24 months. SAVRN’s pairing model holds the AI data center transformer shortage GSU slot at the same authorization moment as the turbine slot, with matched delivery dates. The capex impact is small. The schedule impact is the difference between an AI campus energizing in 2027 and one energizing in 2029.

Lever 3: Vertical manufacturing of pad-mount distribution transformers and switchgear

Intelliflex, integral to SAVRN, manufactures modular compute pods, cooling skids, generator enclosures, switchgear assemblies, and the pad-mount distribution transformer integration packages at its Fort Worth, Texas facility. The vertical integration converts the smallest, most numerous transformer class in the AI data center transformer shortage envelope into a production schedule SAVRN controls. The medium-voltage feeders, pad-mount transformers, and 480-volt distribution panels that conventional EPC firms procure from multiple specialty fabricators on 30-to-50-week lead times instead run through Fort Worth on production schedules SAVRN sets. The result is a distribution build cadence that pairs with the upstream GSU and LPT delivery rather than waiting on it. Customer-facing months collapse to weeks because the distribution manufacturing is internal to SAVRN.

Lever 4: Diversified manufacturer relationships across the AI data center transformer shortage

SAVRN’s transformer procurement spans multiple qualified manufacturers across each AI data center transformer shortage class, rather than relying on a single source. Hitachi Energy, Siemens Energy, GE Vernova through Prolec GE, Hyundai Electric, Mitsubishi Electric, and the qualified North American transformer specialists Howard Industries, Pennsylvania Transformer, ERMCO, and Virginia Transformer all sit inside the SAVRN qualified supplier list with active slot reservations. The diversification protects against the single-manufacturer concentration risk that a single Hitachi Energy or Siemens Energy slot postponement would otherwise impose. The AI data center transformer shortage is therefore mitigated at the SAVRN procurement layer by a portfolio approach that no single project can replicate without years of supplier qualification cycles.

AI data center transformer shortage regional spread across SAVRN geographies

Texas: domestic transformer supply mitigates the AI data center transformer shortage

Texas runs the densest North American transformer manufacturing footprint outside the Northeast, with Prolec GE operating a major large-power-transformer facility in Monterrey, Mexico that supplies the Texas market on short logistics timelines. The Electric Reliability Council of Texas large-load interconnection process introduced in 2024 also forces utility-tie transformer specifications to converge on a smaller set of standardized voltage classes, which simplifies the AI data center transformer shortage procurement decision in ERCOT relative to other ISO footprints. SAVRN’s Texas development benefits from the manufacturing proximity, the standardized voltage class, and the Intelliflex Fort Worth distribution-transformer manufacturing footprint. The combination produces the shortest AI data center transformer shortage deployment window across the SAVRN geography portfolio.

California: BTM bypass reduces AI data center transformer shortage exposure

California’s CAISO interconnection queue runs roughly 410 gigawatts with five-to-six-year typical waits, per LBNL Queued Up 2025. Utility-tie transformer specifications inside CAISO converge on 230 kV and 500 kV classes with long-running auto-transformer lead times that compound the broader AI data center transformer shortage. The behind-the-meter bypass strategy in California therefore relies on right-sizing the generator step-up transformer to the on-site generation rather than the utility tie, which reduces the auto-transformer exposure. SAVRN’s California development pursues this path. The smaller GSU sized to behind-the-meter generation, paired with district-permit-friendly turbine classes, produces a workable AI data center transformer shortage profile even where utility-tie procurement would face longer lead times.

Colorado: mid-band auto-transformer demand inside the AI data center transformer shortage

Colorado utility-tie voltages typically run 115 kV or 230 kV on the Public Service Company of Colorado footprint, with 345 kV on the Tri-State Generation and Transmission interties. The mid-band transformer class avoids the longest auto-transformer lead times that 500 kV and 765 kV intertie classes carry. SAVRN’s Colorado development pursues a mid-scale AI data center transformer shortage profile, with aeroderivative and reciprocating engine turbine slots paired against 115 kV or 230 kV generator step-up transformers and 13.8 kV medium-voltage distribution transformers internal to the campus. The combination produces a workable transformer slot stack within the broader AI data center transformer shortage envelope. The Colorado Public Utilities Commission has also been receptive to large-load AI campus siting, which simplifies the utility-tie permitting where the tie is sized for export and reliability rather than primary supply.

Nebraska: SPP transformer supply and AI data center transformer shortage economics

Nebraska sits inside the Southwest Power Pool footprint and benefits from low network upgrade allocations relative to PJM, CAISO, and MISO. SPP utility-tie voltages run 115 kV, 230 kV, and 345 kV across most of the footprint, with auto-transformer demand concentrated in the mid-band rather than the longest-lead-time 500 kV and 765 kV classes. The AI data center transformer shortage profile in Nebraska therefore favors larger heavy-duty turbine deployments paired with 345 kV generator step-up transformers and 230 kV bulk distribution tie transformers internal to the campus. The state’s public-power utility structure also creates a workable regulatory environment for large-load interconnection, even where the bulk of generation is behind-the-meter and the utility tie is sized for export and reliability rather than primary supply.

Panama and Barbados: international transformer supply chains in the AI data center transformer shortage

Panama and Barbados operate outside the United States independent system operator framework, replacing FERC Order 2023 cluster studies with national grid coordination. Transformer specifications in both jurisdictions run on IEC standards rather than ANSI/IEEE standards, opening a wider set of qualified European, Korean, Japanese, and Chinese transformer manufacturers into the procurement pool. The AI data center transformer shortage profile in Panama and Barbados therefore benefits from a wider qualified supplier base than United States projects can access on short timelines, and from LNG-fed turbine configurations that align with the available transformer classes. SAVRN’s Panama and Barbados developments leverage these structural advantages, with aeroderivative and reciprocating engine fleets sized against LNG supply contracts and IEC-standard transformer slot reservations.

Capex math: the AI data center transformer shortage and the 200 megawatt campus

Path A: conventional 200 megawatt procurement under the AI data center transformer shortage

A 200 megawatt AI campus procuring transformers through conventional channels in 2026 files generator step-up transformer slot requests with the major manufacturers at standard customer terms. GSU slots run 144 weeks. Large power transformer slots run 128 weeks for the utility-tie auto-transformer. Medium-voltage distribution transformer fleets run 60 to 80 weeks per unit. Pad-mount distribution transformer fleets run 40 to 60 weeks per unit. Sequenced against turbine slot delivery and balance-of-plant integration, the conventional AI data center transformer shortage procurement path delivers first-token operation in 2030 or 2031. Total transformer line item capex including GSU, LPT, medium-voltage, pad-mount, and switchgear integration runs $15 million to $30 million for a 200 megawatt AI campus, with total project capex including turbines, balance-of-plant, transmission tie, and emissions controls running $18 million to $24 million per megawatt.

Path B: SAVRN sovereign deploy bypasses the AI data center transformer shortage timeline

The same 200 megawatts under SAVRN sovereign procurement runs through a fundamentally different sequence. SAVRN draws transformers from pre-positioned slot inventory across all four AI data center transformer shortage classes. The matched GSU slot ships with the matched turbine slot. The matched LPT slot ships with the utility tie commitment. Intelliflex Fort Worth manufactures the pad-mount distribution transformers, medium-voltage feeders, and switchgear assemblies on a SAVRN-controlled production schedule. The campus interconnects to a natural gas pipeline tie rather than the bulk power grid, which sizes down or eliminates the longest-lead-time auto-transformer class. First-token operation lands inside 6 to 12 months from authorization. Total project capex runs $9 million to $12 million per megawatt depending on geography, placing the 200 megawatt project capex at $1.8 billion to $2.4 billion. The capex delta is 40 to 55 percent. The schedule delta is three to four years.

The AI data center transformer shortage and the SAVRN BYOP doctrine

The SAVRN bring-your-own-power doctrine elevates the AI data center transformer shortage from a procurement line item to a structural pillar of the operating model. The doctrine has four pillars. First, own the generation. SAVRN deploys on-site gas turbines paired with their matched generator step-up transformers, eliminating dependence on utility-tie auto-transformers for primary supply. Second, own the manufacturing. Intelliflex Fort Worth produces the pad-mount distribution transformers, switchgear, and balance-of-plant assemblies that conventional EPC firms procure from third parties. Third, own the cooling. Closed-loop liquid cooling reduces the cooling-system transformer demand that conventional evaporative cooling architectures require. Fourth, own the schedule. Pre-positioned transformer slot reservations convert customer-facing manufacturer lead times into production schedules SAVRN controls.

The four pillars compound. Each one alone collapses a category of AI data center transformer shortage exposure that the conventional AI infrastructure model treats as exogenous. Together, the four pillars convert the 24-to-48-month industry standard build into the 6-to-12-month SAVRN sovereign deploy. Transformers sit at the load-bearing center of this architecture because they are the load-bearing electrical equipment that ties every megawatt of generation to every megawatt of compute. Renewable plus storage architectures still require transformers, and at AI campus scale they require more transformers per delivered megawatt than thermal architectures because of the lower capacity factor and the storage-system step-up duty. The AI data center transformer shortage is therefore the doctrine’s necessary procurement focus, not a contingent line item.

For the SAVRN operating model, the implication is direct. Sovereign-program buyers, hyperscale AI builders, and merchant compute developers that secure SAVRN deployment slots in 2026 will land AI capacity that ships in 2027 and 2028. Those that defer transformer slot reservations until other project clarity arrives will discover that both the utility interconnection and the AI data center transformer shortage have closed against them. The 2026 procurement window for generator step-up transformers, large power transformers, medium-voltage distribution transformers, and pad-mount distribution transformers is now the binding operational variable. SAVRN’s pre-positioned inventory model converts that variable into a competitive advantage for the operators who recognize and act on it. The procurement decision is the deployment decision.

Frequently asked questions about the AI data center transformer shortage

How long does it take to procure transformers in the AI data center transformer shortage?

Lead times across the AI data center transformer shortage in 2026 vary by class. Generator step-up transformers run 144 weeks against a 2020 baseline of 6 to 12 weeks, per the Wood Mackenzie Q2 2025 transformer market survey. Large power transformers run 128 weeks. Medium-voltage distribution transformers run 60 to 80 weeks. Pad-mount distribution transformers run 40 to 60 weeks. Auto-transformers for 500 kV and 765 kV utility ties run 150-plus weeks at the major manufacturers. SAVRN’s pre-positioned slot inventory model compresses customer-facing lead times to 6 to 12 months by holding committed positions across all four classes ahead of specific project demand. The transformer slot, not the transformer price, is the binding procurement variable in 2026.

Why is the AI data center transformer shortage structural through 2028?

The AI data center transformer shortage is structural through 2028 because four demand vectors are pulling simultaneously against limited manufacturing capacity. First, the AI campus class has emerged as a new demand category. Second, utility resource adequacy programs are returning to dispatchable generation as coal retirements proceed, per the NERC 2025 Long-Term Reliability Assessment. Third, industrial customers are deploying gas combined-cycle for on-site generation. Fourth, the U.S. Department of Energy 2024 final rule on distribution transformer efficiency standards has tightened spot availability during the transitional period to its 2027 effective date. The four vectors combine against transformer manufacturing capacity that does not expand inside a 24-to-36-month window. Hitachi Energy, Siemens Energy, and GE Vernova are all running record order backlogs at allocation status through 2028.

How does SAVRN secure transformers inside the AI data center transformer shortage?

SAVRN secures transformers inside the AI data center transformer shortage through pre-positioned slot reservations posted on the operator balance sheet ahead of specific project demand. The procurement function operates as a transformer slot inventory desk, holding committed positions across generator step-up, large power, medium-voltage distribution, and pad-mount distribution classes. Slots reallocate to specific projects as site readiness, sovereign program demand, and contracted offtake align. Intelliflex Fort Worth manufactures the pad-mount distribution transformers, switchgear, and balance-of-plant components in-house, eliminating the customer-facing lead times that constrain conventional EPC contractors. The result is a 6-to-12-month customer-facing deployment timeline that the conventional procurement model cannot match in 2026.

What size transformers fit a 200 megawatt campus under the AI data center transformer shortage?

A 200 megawatt AI campus typically deploys one or two generator step-up transformers in the 100 to 280 MVA range coupled to the on-site turbines, a 250 to 400 MVA large power transformer on the utility tie if utility tie is used, four to twelve medium-voltage distribution transformers in the 5 to 20 MVA range stepping bulk supply to internal feeders, and 60 to 200 pad-mount distribution transformers in the 100 to 1,000 kVA range serving the final step to 480 V utilization voltage. The transformer fleet count is therefore 65 to 215 units per 200 megawatt AI campus, with the AI data center transformer shortage applying across every voltage class. SAVRN’s hybrid procurement model layers Tier 1 OEM slots on the upstream classes and Intelliflex Fort Worth in-house manufacturing on the downstream pad-mount fleet.

How much do transformers cost inside the AI data center transformer shortage?

Installed capex inside the AI data center transformer shortage varies by class. Generator step-up transformers run $25,000 to $40,000 per MVA. Large power transformers run $30,000 to $50,000 per MVA. Medium-voltage distribution transformers run $40,000 to $70,000 per MVA. Pad-mount distribution transformers run $50,000 to $90,000 per MVA. The total transformer line item for a 200 megawatt AI campus runs $15 million to $30 million depending on configuration. Full campus capex including transformers, turbines, balance-of-plant, transmission tie, and emissions controls runs $9 million to $12 million per megawatt under SAVRN sovereign procurement, compared to $18 million to $24 million per megawatt under conventional procurement. The cost driver is procurement model, not transformer class.

How does the DOE 2027 efficiency rule affect the AI data center transformer shortage?

The U.S. Department of Energy 2024 final rule on distribution transformer energy conservation standards takes effect in 2027 and increases minimum efficiency requirements on distribution transformers. The rule reshapes the AI data center transformer shortage at the distribution layer by shifting design preferences toward higher-grade grain-oriented electrical steel or amorphous metal core options, with implications for winding designs. The transitional period to the 2027 effective date has tightened spot availability of pre-rule distribution transformers during 2025 and 2026 as manufacturers prepare. Operators procuring distribution transformer fleets through 2027 should specify whether the units meet the new standard at delivery, since pre-standard units delivered after the effective date face downstream regulatory and resale issues. SAVRN procurement targets post-2027 compliant designs across the full pad-mount distribution fleet.

What about amorphous metal cores in the AI data center transformer shortage?

Amorphous metal core distribution transformers offer materially lower no-load losses than grain-oriented electrical steel cores, with the trade-off of higher unit capex and tighter supply concentration. Hitachi Metals, Liaoning Liaoning Amorphous, and ATI Specialty Materials dominate the global amorphous metal ribbon supply. AI campuses with high capacity factor and 24-by-7 operation realize the loss savings quickly, and the design favors amorphous metal cores in the pad-mount distribution layer where the no-load loss compounds across hundreds of units. The DOE 2027 efficiency rule further tilts the AI data center transformer shortage toward amorphous metal designs by raising the minimum efficiency threshold. SAVRN’s pad-mount distribution procurement specifies amorphous metal cores where the operating economics support the higher unit capex, which is typically the case for AI campus loads.

What service contracts do transformers require under the AI data center transformer shortage?

Power transformers above 100 MVA require monitoring, periodic dissolved gas analysis, and end-of-life refurbishment programs that the major manufacturers and qualified third-party service firms provide. Service capacity tightens in parallel with new-unit slot availability inside the broader AI data center transformer shortage, since the same factories that manufacture new units also support refurbishment programs. SAVRN secures service agreements at slot reservation, locking parts and labor availability ahead of the operational phase. Distribution transformers below 5 MVA typically run on a fleet-level service model rather than unit-level service contracts. The Department of Energy Grid Resilience and Innovation Partnerships program documents the industry-wide service capacity pressure through 2028, particularly for the largest auto-transformer classes that utility-tie AI campus interconnections require.

How does the AI data center transformer shortage compare to switchgear supply?

Switchgear supply tracks the AI data center transformer shortage closely. Medium-voltage switchgear, gas-insulated switchgear, and bus duct all run multi-year backlogs at the major manufacturers, with lead times of 40 to 80 weeks across the 5 to 38 kV class. The integration between transformers and switchgear is tight, with bus duct connections, cable terminations, and protection relays specified against the transformer impedance and short-circuit ratings. SAVRN’s Intelliflex Fort Worth facility manufactures the medium-voltage switchgear assemblies in-house, eliminating the customer-facing lead time on this integration class. The vertical integration converts the second-largest AI data center transformer shortage adjacent constraint into a SAVRN production schedule. Conventional EPC contractors procure switchgear from third-party fabricators on the same constrained timeline as the transformers themselves.

How does the AI data center transformer shortage compare to solar plus storage transformer demand?

Behind-the-meter solar plus battery storage architectures sized to AI campus loads require more transformers per delivered megawatt than thermal generation architectures. A 1,500 megawatt solar plus 12 gigawatt hour battery storage system sized to deliver 200 megawatt firm baseload requires roughly 60 to 150 medium-voltage step-up transformers on the solar side and another 20 to 50 medium-voltage transformers on the storage side, against a thermal generation alternative requiring 4 to 12 generator step-up transformers total. The AI data center transformer shortage therefore amplifies the procurement burden on the renewable plus storage path. Thermal generation architectures, particularly the SAVRN sovereign behind-the-meter natural gas turbine stack, reduce the transformer count per delivered megawatt by 10x or more, materially mitigating exposure to the broader AI data center transformer shortage.

Sources & Citations

Every quantitative claim in this piece traces to a named, verified primary source. URLs verified at time of publication. The full audit-grade citation record, with claim-by-claim source mapping and “cite this article” snippets, is maintained on the dedicated SAVRN sources page for this piece.

Primary research and forecasts cited in this AI data center transformer shortage brief

- Wood Mackenzie, Q2 2025 Transformer Market Survey. Source for: generator step-up transformer lead times of 144 weeks, large power transformer lead times of 128 weeks, 30 percent supply deficit through 2027, 2020 baseline of 6 to 12 weeks.

- Hitachi Energy, Annual Report 2025. Source for: record transformer order intake during 2025, over $4.5 billion capital expansion of global transformer manufacturing footprint through 2027, AI data center demand as largest single driver of order book growth.

- Siemens Energy, Annual Report 2025. Source for: Grid Technologies segment expansion, AI data center demand as leading incremental commitment source.

- GE Vernova, Q1 2026 Earnings Release. Source for: Electrification segment order backlog at record levels, Prolec GE joint venture multi-year delivery commitments.

- Electric Power Research Institute, Powering Intelligence: Analyzing Artificial Intelligence and Data Center Energy Consumption, 2024. Source for: US data center share of total electricity 2030 estimate near 9 percent, AI campus class load profile.

Standards, regulatory, and policy references for the AI data center transformer shortage

- U.S. Department of Energy, Distribution Transformers Final Rule, 2024. Source for: 2027 effective date for new minimum efficiency standards, transitional supply tightening through 2025-2026.

- North American Electric Reliability Corporation, 2025 Long-Term Reliability Assessment. Source for: natural gas dominant share of incremental dispatchable capacity, resource adequacy gap and corrective procurement timelines.

- International Energy Agency, Energy and AI, 2025. Source for: 2030 global data center electricity demand at 945 terawatt-hours, 12 percent compound annual growth rate.

- Lawrence Berkeley National Laboratory, Queued Up: 2025 Edition. Source for: 2,060 gigawatts in active interconnection queue, 5-year typical wait, CAISO 410 GW queue depth.

- Lawrence Berkeley National Laboratory, 2024 United States Data Center Energy Usage Report (Shehabi et al.). Source for: 2028 data center electricity demand at 6.7 to 12.0 percent of total United States electricity.

View the full audit record for this AI data center transformer shortage brief →

Continue exploring the AI data center transformer shortage and the SAVRN doctrine

The AI data center transformer shortage decision sits inside the broader SAVRN sovereign infrastructure doctrine. Companion analyses across the SAVRN doctrine series take the topic into adjacent procurement decisions. The AI data center natural gas turbines brief documents the matched-turbine slot environment that pairs with the AI data center transformer shortage at the generator step-up layer. The AI data center grid interconnection brief writes the 2026 queue math that is driving operators away from utility tie procurement and the longest-lead-time auto-transformer classes. The AI data center supply chain brief covers the cross-equipment lead time landscape including switchgear, bus duct, and reciprocating engines.

For procurement and capex framing, the AI data center construction cost brief writes the bill-of-materials math against AI rack densities, and the tokens per watt per dollar brief writes the operating-economics metric that connects equipment capex to AI inference unit economics. The behind-the-meter AI power brief documents the bypass economics that reduce AI data center transformer shortage exposure on the auto-transformer class. The liquid cooling for AI brief documents the closed-loop cooling architecture that lowers the cooling-system transformer demand against conventional evaporative architectures.

The full doctrine is anchored at sovereign AI infrastructure, the foundational brief that frames the SAVRN operating model. The SAVRN doctrine page collects every pillar in the series. For operator engagement, the SAVRN infrastructure assessment form connects qualifying buyers to a tailored deployment proposal. SAVRN active geographies under development: California, Texas, Colorado, Nebraska, Panama, and Barbados. Manufacturing footprint: Intelliflex, Fort Worth, Texas. AI data center transformer shortage slot inventory: generator step-up, large power, medium-voltage distribution, pad-mount distribution, with switchgear and bus duct integration slots paired.