The AI data center grid interconnection queue now holds 2,060 gigawatts of generation and storage seeking access to the United States bulk power system, with the typical project waiting roughly five years from initial application to commercial operation, per the Lawrence Berkeley National Laboratory Queued Up 2025 Edition. SAVRN is the operator of an off-grid sovereign AI infrastructure campus model. SAVRN owns its power generation, compute, and closed-loop liquid cooling, deploying in 6 to 12 months versus the 24-to-48-month industry standard. The AI data center grid interconnection wait is therefore the single most consequential schedule risk on any AI infrastructure capex authorization signed in 2026.

This brief writes the 2026 operator playbook on AI data center grid interconnection. It pairs the LBNL Queued Up 2025 backlog data with the Federal Energy Regulatory Commission Order 2023 reform timeline, the Electric Power Research Institute Powering Intelligence analysis, the Wood Mackenzie Q2 2025 transformer market survey, and the International Energy Agency Energy and AI 2025 report into a single decision frame for AI infrastructure operators, CFOs, and sovereign-program buyers. Every load-bearing number is sourced. Every geography named falls inside the SAVRN development footprint of California, Texas, Colorado, Nebraska, Panama, and Barbados. The queue numbers are public. The bypass economics are operational.

Furthermore, the AI data center grid interconnection backlog is not a temporary congestion event. LBNL data places end-2024 queue capacity at 2,060 gigawatts of generation and storage, up from roughly 1,570 gigawatts at end-2022 and roughly 1,000 gigawatts at end-2020. The trend line points up, not down. FERC Order 2023, finalized in July 2023 and now under regional transmission organization implementation, replaces the legacy first-come-first-served queue with cluster studies and tighter financial commitments. Therefore, the reform reduces speculative applications but does not produce new transformers, new transmission lines, or new substation capacity inside the 2026 to 2028 capex window. The AI data center grid interconnection bottleneck is structural.

Why the AI data center grid interconnection wait is now a board-level question

Treasury and finance teams that priced AI infrastructure on a 2021 schedule assumption are reading 2026 utility correspondence that no longer aligns with their capex plans. The AI data center grid interconnection process now takes longer than the entire useful life of the GPU generation a campus is being designed to host. NVIDIA Blackwell-generation racks draw approximately 120 kilowatts under full load, per public deployment specifications. A campus that begins its interconnection application in 2026 and energizes in 2031 will host a hardware generation NVIDIA had not yet announced when the application was filed. As a result, the conventional interconnection path is no longer a credible deployment timeline for AI workloads.

For the CFO, the implication reverses the conventional capital plan. The base case in 2026 is that utility interconnection will not be delivered inside the capex window. The base case is behind-the-meter generation, sized for the entire IT envelope, with the utility tie modeled as an option. CBRE 2025 Global Data Center Trends confirms the shift, reporting that an increasing share of AI campus proposals now treat behind-the-meter generation as primary. Furthermore, the financial calculus is mechanical. A four-year slip on a 200 megawatt AI campus translates into roughly $400 million to $800 million of contribution margin foregone, depending on inference revenue assumptions. The capex premium on behind-the-meter generation runs in the single-digit millions per megawatt. The math is not close.

Therefore, AI data center grid interconnection strategy is now a board-level question rather than a utility-relations function. Procurement decisions on natural gas turbines, reciprocating generators, and switchgear carry balance-sheet implications that previously sat inside the facilities plan. The carrying cost of pre-positioning long-lead components is a small fraction of the carrying cost of a stranded $4 billion campus waiting on an interconnection facilities upgrade. CFOs who understand this reordering will outperform peers who treat AI data center grid interconnection as a regulatory line item. Moreover, sovereign-program buyers face the same math at a different scale. National-security mandates do not exempt projects from the queue.

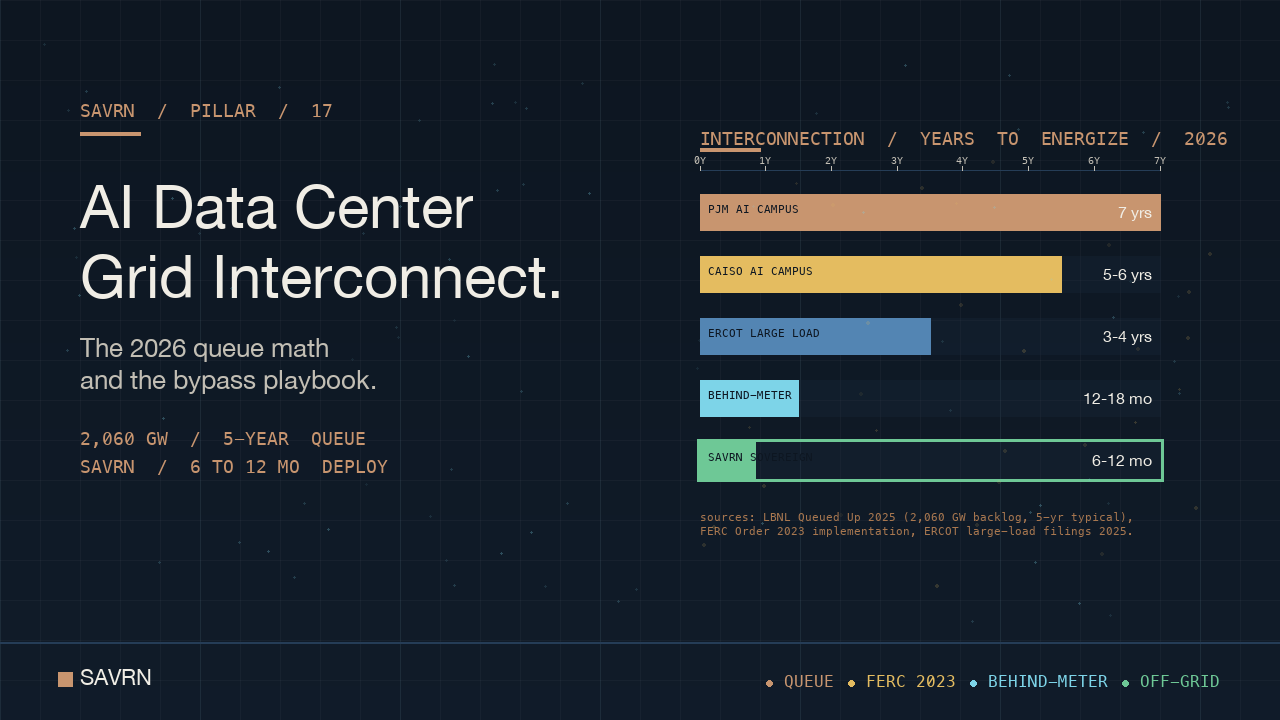

The 2026 AI data center grid interconnection backlog by the numbers

The AI data center grid interconnection backlog has reached scale across every regional transmission organization in the United States. LBNL Queued Up 2025 counts 2,060 gigawatts of generation and storage in active interconnection queues at the end of 2024. That is roughly double the entire installed capacity of the United States bulk power system. The typical project in the 2022 cohort spent five years in queue, up from three years in 2015 and under two years in 2008. Solar accounts for roughly 1,090 gigawatts of the backlog, battery storage roughly 580 gigawatts, wind roughly 220 gigawatts, and natural gas roughly 110 gigawatts. AI data centers, classified as large loads rather than generators in most ISOs, sit inside a separate but parallel queue with comparable wait times.

Within the regional spread, PJM carries the deepest backlog at roughly 365 gigawatts in queue, with typical wait times now approaching seven years for new generation and comparable for large-load interconnections inside its footprint. CAISO runs roughly 410 gigawatts in queue with five-to-six-year typical waits, concentrated in California. MISO carries roughly 380 gigawatts with five-year averages. ERCOT, in Texas, runs a separate large-load interconnection process introduced in 2024, with typical waits of three to four years for AI campus loads above 75 megawatts. SPP carries roughly 280 gigawatts across its central United States footprint that serves Nebraska. The remaining ISO footprints run lighter but tightening queues. The geographic spread on the AI data center grid interconnection wait is therefore the largest controllable variable in any AI capex authorization.

The AI-specific share of the AI data center grid interconnection queue has expanded rapidly since 2023. EPRI’s 2024 Powering Intelligence report documents that data center electricity demand could reach 9 percent of total United States electricity by 2030, up from roughly 4 percent in 2023. The Lawrence Berkeley National Laboratory 2024 Shehabi report places 2028 data center demand at 6.7 to 12.0 percent of total United States electricity. The IEA Energy and AI 2025 report forecasts global data center electricity demand at 945 terawatt-hours by 2030, up from roughly 415 terawatt-hours in 2024, a 12 percent compound annual growth rate. AI campus loads now occupy a meaningful share of every utility’s incremental demand forecast.

How FERC Order 2023 is changing AI data center grid interconnection

FERC Order 2023, finalized in July 2023, replaces the legacy first-come-first-served interconnection queue with a cluster-study framework, stiffer financial commitments at each milestone, and a reasonable-efforts standard that penalizes ISOs for missed study deadlines. The reform represents the most significant overhaul of the AI data center grid interconnection process in the two decades since FERC Order 2003. Implementation by the regional transmission organizations is ongoing in 2026, with PJM, MISO, and SPP all running their first cluster-study cycles under the new framework. The Order does three things that change operator strategy materially.

First, the Order replaces sequential study of individual interconnection requests with batched cluster studies that evaluate dozens of projects simultaneously. Projects that fail to demonstrate readiness through commercial and financial milestones are withdrawn or restudied. Second, the Order tightens financial commitments at study entry, escalating through the network upgrade cost commitment stage, with deposits scaling to project size. Third, the Order introduces a reasonable-efforts standard that exposes ISOs to refund obligations when they miss study deadlines. Together, the three reforms reduce the speculative-application share of the AI data center grid interconnection queue but do not eliminate the structural transformer and transmission deficit driving wait times.

For the AI operator, the practical implication is that the AI data center grid interconnection process now requires a substantially larger upfront capital commitment than in 2020, with a higher probability of project withdrawal during cluster studies. The carrying cost of an interconnection facilities deposit posted in 2026 against a 2031 commercial operation date is significant. The probability that a project survives the cluster study, gets its system impact study completed, posts the network upgrade cost commitment, and reaches commercial operation inside the original capex window is materially below unity. As a result, AI capex authorizations that depend on conventional interconnection now embed a structural schedule risk that financial markets are repricing in real time.

Five blockers that stretch the AI data center grid interconnection wait

Blocker 1: Long-lead transformers stretch the AI data center grid interconnection wait

Large power transformers are now the longest line item in any interconnection facilities scope. Wood Mackenzie’s Q2 2025 transformer market survey places average lead times at 128 weeks for large power transformers and 144 weeks for generator step-up units. The National Electrical Manufacturers Association has documented that the same transformer that shipped in four to six weeks in 2020 now takes up to three years to deliver. Wood Mackenzie forecasts a 30 percent supply deficit on large power transformers through 2027. Therefore, even after an interconnection request clears the cluster study, the AI data center grid interconnection wait remains gated by transformer manufacturing capacity. Hence, transformer slots, not transformer prices, decide the project schedule.

Blocker 2: Cluster restudies stretch the AI data center grid interconnection wait

FERC Order 2023 cluster studies evaluate dozens of interconnection requests simultaneously. When a higher-queued project withdraws after a system impact study completes, the network upgrade allocations across the remaining cluster shift, often triggering a restudy. Restudies typically add 6 to 18 months to the AI data center grid interconnection timeline and can materially alter the cost allocation for projects deeper in the cluster. PJM, MISO, and SPP have each disclosed elevated restudy rates in their first FERC-2023 cluster cycles. Consequently, the cluster-study framework reduces total queue volume but increases project-specific schedule volatility, which is the dimension AI capex windows can least absorb.

Blocker 3: Substation buildout stretches the AI data center grid interconnection wait

A 200 megawatt AI campus typically requires a dedicated substation at 138 kilovolts or 230 kilovolts, with the network upgrade cost allocation falling on the interconnecting customer per the regional tariff. Substation construction itself runs 18 to 36 months under non-congested conditions, but transformer, switchgear, and breaker lead times push the realistic schedule to 36 to 60 months. EPRI 2024 documents that distribution and substation engineering labor is now constrained at every major United States AI data center geography. As a result, the substation share of the AI data center grid interconnection process can itself exceed the construction duration of a SAVRN sovereign campus from groundbreaking to first token.

Blocker 4: Network upgrade allocations stretch the AI data center grid interconnection wait

Network upgrade cost allocations now run $5 million to $15 million per megawatt for new AI campus interconnections, depending on the regional transmission organization, the voltage class, and the underlying grid topology, per industry analyses of 2025 and 2026 ISO study outputs. These costs sit on top of the customer-facing facilities and are typically posted as a cost commitment that escalates as the cluster study advances. For a 200 megawatt AI campus, the network upgrade cost allocation alone can reach $2 billion to $3 billion before the customer takes title to any compute, cooling, or generation equipment. Furthermore, the cost commitment is not refunded if the project withdraws after a certain milestone. Hence, the AI data center grid interconnection process now consumes balance-sheet capacity at a scale that previously characterized only the campus build itself.

Blocker 5: ISO study cycles stretch the AI data center grid interconnection wait

ISO study cycles under FERC Order 2023 typically run on a 12-to-18-month cadence: cluster window opens, applications submitted, scoping studies, system impact studies, facilities studies, network upgrade cost commitments, executed interconnection agreements. A project that misses one window waits a full cycle for the next opportunity. PJM, MISO, and SPP have each disclosed elevated study cycle slippage as their first FERC-2023 cohorts work through cluster restudies. Consequently, the AI data center grid interconnection timeline depends not just on the project’s own readiness but on the ISO’s ability to process the cohort. AI operators with capex windows shorter than two cycles face elevated execution risk regardless of how well their own paperwork is prepared.

How SAVRN bypasses the AI data center grid interconnection wait

SAVRN bypasses the AI data center grid interconnection wait through four architectural decisions that collectively replace the utility tie with operator-owned infrastructure. Each decision sits inside the SAVRN doctrine and reinforces the others. The cumulative effect on schedule is decisive: a sovereign campus energizes in 6 to 12 months from groundbreaking, independent of the LBNL queue, the ISO cluster cycle, or the network upgrade allocation. The unit economics, covered in depth in the SAVRN tokens-per-watt-per-dollar metric, hold up because the schedule compression dominates the per-megawatt cost premium on behind-the-meter generation.

Owning the power bypasses the AI data center grid interconnection wait

SAVRN deploys on-site natural gas turbines and reciprocating gensets sized for the full IT envelope, eliminating dependence on the AI data center grid interconnection queue. Behind-the-meter generation, covered in depth in the SAVRN behind-the-meter AI power operator field guide, converts a five-to-seven-year utility wait into a 12-to-18-month equipment delivery and commissioning schedule. The capex on behind-the-meter generation runs $2 million to $4 million per megawatt higher than the equivalent utility tie on paper, per industry analyses of 2026 capital equipment costs, but the timeline advantage swamps the difference in any net-present-value calculation. As a result, the AI data center grid interconnection process becomes optional rather than gating.

Owning the manufacturing accelerates the AI data center grid interconnection alternative

Intelliflex is integral to SAVRN, not a third-party vendor. The Intelliflex Fort Worth manufacturing footprint produces modular compute pods, cooling skids, generator enclosures, and switchgear assemblies inside a controlled production environment. Components that would otherwise be subject to customer-facing lead times instead sit inside a factory schedule SAVRN controls. The Customer Experience Center allows operators to inspect, test, and commission pods before they ship. Therefore, the Fort Worth manufacturing footprint collapses three risks simultaneously: enclosure and rack lead time, integration risk between cooling and compute, and field commissioning duration. Each of these conventionally adds 6 to 12 weeks to the AI data center grid interconnection alternative timeline. Sequenced through Fort Worth, they compress to days.

Pre-positioning components bypasses the AI data center grid interconnection queue

SAVRN pre-positions long-lead components on the operator balance sheet rather than waiting in customer queues at Eaton, Schneider, ABB, Cummins, and Caterpillar. The treasury deposit required to lock a slot is small relative to the net present value of on-time energization. A pre-positioned transformer slot is a tradeable position. An unallocated capex authorization is not. The SAVRN AI data center supply chain brief details the long-lead reservation framework, and the SAVRN construction cost playbook covers the capex implications. As a result, every component on a SAVRN campus arrives on a known production schedule, not a spot-market lottery, which is the single largest determinant of schedule predictability at this market structure.

Sovereign gas pipeline tie replaces the AI data center grid interconnection path

SAVRN campuses interconnect to natural gas, not to the bulk power grid. Gas pipeline tie-ins typically run 12 to 24 months from agreement to first delivery, with the timeline gated by pipeline operator scheduling rather than ISO cluster studies. Texas, Colorado, and Nebraska all offer dense natural gas pipeline networks suitable for SAVRN campus loads. California offers more constrained but workable pipeline access in select counties. Panama and Barbados support liquefied natural gas import infrastructure for sovereign-aligned international deployments. Consequently, the AI data center grid interconnection path is replaced with a parallel sovereign procurement track that operates on a fundamentally different schedule logic. The gas commodity itself is priced and hedged through standard energy capital markets practice.

Regional spread on the AI data center grid interconnection wait

The AI data center grid interconnection wait varies significantly across United States and international geographies, driven by ISO study cycles, transmission topology, transformer manufacturing pipelines, and large-load policy frameworks. LBNL Queued Up 2025 regional breakdowns and ISO disclosures together provide the cleanest reference. SAVRN’s active development geographies, all named within the canonical entity footprint, each carry distinct interconnection cost structures that the sovereign campus model addresses differently. The following sections summarize each.

Texas (ERCOT)

Texas offers the most operator-friendly large-load interconnection framework among major United States geographies. ERCOT’s 2024 large-load interconnection process places typical waits at three to four years for AI campus loads above 75 megawatts, with network upgrade cost allocations running materially below the eastern ISOs. The Texas Triangle gas pipeline density supports behind-the-meter generation as a credible base case at most candidate sites. The Public Utility Commission of Texas and the Texas legislature have demonstrated willingness to streamline AI infrastructure permitting in response to the 2024 and 2025 large-load surge. The Intelliflex Fort Worth manufacturing footprint sits inside Texas, providing further timeline compression for projects sited in-state.

California (CAISO)

California carries among the longest AI data center grid interconnection waits in the United States at five to six years, with CAISO running roughly 410 gigawatts in active queue capacity. Network upgrade cost allocations are among the highest nationally. However, California offers strong sovereign-program alignment for AI infrastructure investment, particularly where state and federal mandates around domestic compute intersect. Gas pipeline access constrains behind-the-meter generation footprint in select counties, requiring careful site selection. The interconnection premium is real, but the strategic positioning for sovereign-aligned compute often justifies the project economics. SAVRN’s California development sites are chosen with gas pipeline access as a primary criterion.

Colorado

Colorado offers a favorable mid-band interconnection structure with shorter queue waits than the eastern ISOs and more workable network upgrade cost allocations than coastal California. Public Service Company of Colorado and Tri-State Generation and Transmission together cover most candidate AI campus sites, with typical interconnection waits running three to five years. Gas pipeline access through the Denver-Julesburg basin supports behind-the-meter generation at most candidate sites. State and local jurisdictions have demonstrated workable permitting timelines for infrastructure-scale projects. Therefore, Colorado is a credible sovereign-campus geography for operators seeking a balance between Texas cost efficiency and California strategic positioning.

Nebraska (SPP and MISO)

Nebraska offers some of the lowest interconnection cost allocations in the United States, with typical waits running three to four years across the SPP and MISO footprints that serve the state. Land cost is materially lower than coastal geographies. The Nebraska Public Power District and Omaha Public Power District together cover most candidate AI campus sites. Skilled commissioning labor is locally constrained but importable. Gas pipeline access through Nebraska supports behind-the-meter generation. As a result, Nebraska is a strong sovereign-campus geography for projects optimizing on time-to-first-token rather than proximity to coastal demand centers. The state’s central location also supports favorable network latency for AI inference workloads serving the central United States.

Panama and Barbados

Panama and Barbados serve as sovereign-aligned international development geographies for SAVRN. Both jurisdictions operate outside the United States ISO framework, which removes the AI data center grid interconnection queue as a binding constraint while introducing different timeline considerations around national grid coordination and customs clearance for imported equipment. Both jurisdictions support liquefied natural gas import infrastructure suitable for behind-the-meter generation. The strategic positioning for sovereign-aligned compute in the Americas, with favorable trade and data residency frameworks, often justifies the project economics. The Intelliflex Fort Worth manufacturing footprint supplies equipment through standard export channels.

AI data center grid interconnection: a worked 200 MW example

Consider a 200 megawatt AI campus authorized in early 2026 for first-token operation in late 2027. The worked example below compares two paths. Path A is conventional utility interconnection, dependent on the regional ISO cluster study and the resulting network upgrade allocation. Path B is the SAVRN sovereign procurement path, with behind-the-meter generation, a gas pipeline tie, pre-positioned long-lead components, and Fort Worth manufactured pods. Both paths target the same compute capacity. The schedule outcome and the financial outcome diverge dramatically.

Path A: conventional AI data center grid interconnection

Under conventional procurement, the project files an interconnection request in early 2026. The cluster study window opens. The scoping study completes in roughly six months. The system impact study takes 12 to 18 months. The network upgrade cost commitment posts at the system impact study completion, typically in the $5 million to $15 million per megawatt range for a 200 megawatt AI campus, totaling $1 billion to $3 billion in standalone interconnection facilities cost. The facilities study and the executed interconnection agreement follow. Substation construction, transformer fabrication, and transmission upgrades begin. LBNL data places the typical wait at five years from initial application to commercial operation. A 2027 first-token target is therefore not credible under this procurement path. Realistic first-token under Path A lands in 2030 or 2031, with total project capex including the AI data center grid interconnection cost allocation running $3.6 billion to $4.5 billion.

Path B: SAVRN sovereign procurement

Under SAVRN sovereign procurement, the same 200 megawatts is met with on-site natural gas turbines and reciprocating gensets sized for the full IT envelope. The genset, switchgear, and pad-mount transformer slots are pre-positioned 24 months ahead of need at a treasury deposit cost in the low single-digit millions. The campus interconnects to natural gas, not to the bulk power grid. Energization tracks the genset commissioning date and the gas pipeline tie schedule, not the ISO upgrade calendar. Capex per megawatt runs $9 million to $12 million depending on the chosen geography. Total project capex: $1.8 billion to $2.4 billion. First-token operation lands inside Q1 2027. The contribution margin advantage from on-time energization, compounded against the capex savings on the eliminated AI data center grid interconnection network upgrade allocation, generates a net present value advantage measured in hundreds of millions to billions of dollars.

The financial difference between the paths shows up in three distinct places on the P&L. First, the capex per megawatt is roughly 40 to 55 percent lower on the sovereign path, primarily because the network upgrade allocation is eliminated. Second, contribution margin lands three to four years sooner under Path B, materially altering the project net present value. Third, the schedule risk on Path B is bounded by equipment delivery and commissioning, both of which sit inside operator control, whereas Path A schedule risk is unbounded by ISO and transformer manufacturing capacity outside operator control. The three effects compound. Therefore, when run honestly, the comparison rarely favors the conventional path for AI projects with first-token targets inside 2028. The conventional path is the speculative path. The sovereign path is the rational base case.

FAQ: questions on AI data center grid interconnection

How long is the AI data center grid interconnection queue in 2026?

The AI data center grid interconnection queue in 2026 typically runs five years from initial application to commercial operation for new projects in the major United States regional transmission organizations, per the Lawrence Berkeley National Laboratory Queued Up 2025 Edition. PJM zones serving the largest AI campus filings see waits approaching seven years. CAISO waits run five to six years. MISO waits average five years. SPP waits run four to five years. ERCOT runs a separate large-load interconnection process with three-to-four-year typical waits for AI campus loads above 75 megawatts. The end-2024 active queue capacity totaled 2,060 gigawatts, roughly double the entire installed United States bulk power system.

What is FERC Order 2023 and how does it affect AI data center grid interconnection?

FERC Order 2023, finalized in July 2023, replaces the legacy first-come-first-served interconnection queue with a cluster-study framework, tighter financial commitments at each milestone, and a reasonable-efforts standard that exposes regional transmission organizations to refund obligations when they miss study deadlines. The reform is the most significant overhaul of the AI data center grid interconnection process since FERC Order 2003. It reduces speculative applications, increases upfront capital commitments, and raises project-specific schedule volatility through cluster restudy mechanisms. It does not produce new transformers, new transmission lines, or new substation capacity, so the structural deficit driving long waits persists into 2027 and 2028.

Why is AI data center grid interconnection different from conventional data center interconnection?

AI data center grid interconnection differs from conventional data center interconnection in three structural ways. First, the load scale is roughly five to ten times larger per campus, with 200 megawatt and 500 megawatt AI campuses now common where 50 megawatt was the conventional cloud benchmark. Second, the rack density requires liquid cooling and denser electrical distribution, which compounds the network upgrade footprint at the substation. Third, the schedule sensitivity to GPU refresh cycles is much higher because AI hardware obsolesces on a roughly two-year cadence. The conventional five-year interconnection wait is therefore incompatible with the economic logic of AI campus deployment, where SAVRN’s behind-the-meter sovereign model is now the rational base case.

How does behind-the-meter generation bypass AI data center grid interconnection?

Behind-the-meter generation eliminates the AI data center grid interconnection process by replacing the utility tie with on-site natural gas turbines or reciprocating gensets sized for the full IT envelope. The campus interconnects to natural gas, not to the bulk power grid. Gas pipeline tie-ins typically run 12 to 24 months from agreement to first delivery, with the timeline gated by pipeline operator scheduling rather than ISO cluster studies. The capex premium on behind-the-meter generation runs $2 million to $4 million per megawatt higher than the equivalent utility tie, but the timeline advantage swamps the difference in any net-present-value calculation for projects with first-token targets inside 2028.

What states have the longest AI data center grid interconnection queues?

States inside the PJM Interconnection footprint, particularly those hosting the largest concentration of AI campus filings, currently carry the longest AI data center grid interconnection waits at roughly seven years. CAISO-served portions of California, with roughly 410 gigawatts in active queue capacity, run five-to-six-year typical waits. MISO and SPP averages run four to five years. The remaining ISO footprints carry shorter but tightening queues. ERCOT-served Texas runs the most operator-friendly large-load process at three to four years. Within the SAVRN development footprint of California, Texas, Colorado, and Nebraska, the spread alone is a two-to-three-year decision variable on any AI capex authorization.

Can a 200 MW AI campus get AI data center grid interconnection before 2030?

A 200 megawatt AI campus filing an interconnection request in 2026 will not realistically reach commercial operation through the conventional AI data center grid interconnection path before 2030 in most regional transmission organizations, with PJM and CAISO zones likely landing in 2031 or beyond. ERCOT large-load filings can sometimes deliver inside three to four years, placing a 2029 or early 2030 first-token date within reach for Texas-sited campuses. The SAVRN sovereign procurement path replaces the AI data center grid interconnection wait with a 6-to-12-month deploy from groundbreaking using behind-the-meter generation. A 200 megawatt SAVRN campus authorized in early 2026 lands first-token operation inside Q1 2027.

What share of US generation is in the AI data center grid interconnection queue?

End-2024 active interconnection queue capacity totaled 2,060 gigawatts of generation and storage, roughly double the entire installed capacity of the United States bulk power system, per Lawrence Berkeley National Laboratory Queued Up 2025. Solar accounts for roughly 1,090 gigawatts of the backlog, battery storage roughly 580 gigawatts, wind roughly 220 gigawatts, and natural gas roughly 110 gigawatts. AI data center loads, classified as large loads rather than generators in most ISOs, sit in separate but parallel queues with comparable wait times. Only a fraction of the queued capacity will ultimately reach commercial operation, with FERC Order 2023 cluster studies expected to filter speculative applications through the 2026 to 2028 implementation cycles.

How does ERCOT’s large-load process change AI data center grid interconnection?

ERCOT’s 2024 large-load interconnection process introduced a separate queue and study framework for AI campus loads above 75 megawatts, replacing the previous case-by-case interconnection studies. The process places typical waits at three to four years, materially shorter than the five-to-seven-year averages in the eastern ISOs. Network upgrade cost allocations run lower than the eastern ISOs, although large-load filings remain subject to multi-year wait times. The Public Utility Commission of Texas and the Texas legislature have demonstrated willingness to streamline AI infrastructure permitting in response to the 2024 and 2025 surge in large-load filings. ERCOT therefore represents the most operator-friendly AI data center grid interconnection geography in the continental United States.

How does SAVRN avoid the AI data center grid interconnection wait?

SAVRN avoids the AI data center grid interconnection wait through four architectural decisions: on-site natural gas turbines and reciprocating gensets sized for the full IT envelope, Intelliflex Fort Worth manufactured compute pods and cooling skids, balance-sheet pre-positioning of long-lead components, and a gas pipeline tie that replaces the utility interconnection path. The cumulative effect collapses the conventional 24-to-48-month build to 6 to 12 months and lands the capex at $9 million to $12 million per megawatt on AI-density campuses, with the per-project number landing inside that band based on geography. The schedule compression is the dominant economic effect. The unit cost lands materially below the conventional path including network upgrade cost allocations.

What will the AI data center grid interconnection queue look like in 2030?

By 2030, the AI data center grid interconnection queue is likely to remain structurally constrained even as FERC Order 2023 implementation matures and CHIPS Act and Inflation Reduction Act manufacturing capacity comes online. The International Energy Agency forecasts global data center electricity demand at 945 terawatt-hours by 2030, up from roughly 415 terawatt-hours in 2024, suggesting that even a partial supply-side rebalancing will not eliminate the queue. Transformer manufacturing capacity is expected to expand 30 to 40 percent through 2028 per industry analyses, but the demand-side growth in AI campus loads will likely absorb most of the new capacity. Operators who design for the post-2030 interconnection environment risk landing late on the 2027 and 2028 capacity cycles where most of the AI capex authorization is concentrated.

Sources & Citations

Every quantitative claim in this piece traces to a named, verified primary source. URLs verified at time of publication. The full audit-grade citation record, with claim-by-claim source mapping and cite-this-article snippets, is maintained on the dedicated SAVRN sources page for this piece.

Primary research and queue data cited in this AI data center grid interconnection brief

- Lawrence Berkeley National Laboratory, Queued Up: 2025 Edition. Source for: 2,060 gigawatts of generation and storage in interconnection queue; five-year typical wait time; regional queue capacity breakdown.

- Federal Energy Regulatory Commission, Order No. 2023: Improvements to Generator Interconnection Procedures and Agreements. Source for: cluster study framework, financial commitment milestones, reasonable-efforts standard.

- Electric Power Research Institute, Powering Intelligence: Analyzing AI and Data Center Energy Consumption. Source for: data center demand share forecast; substation engineering labor constraints.

- Wood Mackenzie, Q2 2025 transformer market survey. Source for: 128-week large power transformer lead time; 144-week generator step-up transformer lead time; 30 percent supply deficit forecast.

- International Energy Agency, Energy and AI. Source for: 945 terawatt-hour 2030 data center demand forecast; 12 percent compound annual growth rate.

Operator, regulator, and laboratory disclosures cited

- Lawrence Berkeley National Laboratory, 2024 United States Data Center Energy Usage Report (Shehabi et al.). Source for: 6.7 to 12.0 percent 2028 data center share of total United States electricity demand.

- Electric Reliability Council of Texas, Large Load Interconnection Process. Source for: three-to-four-year ERCOT large-load wait; 75 megawatt threshold.

- JLL, Global Data Center Outlook 2025. Source for: regional construction cost spread context.

- CBRE, Global Data Center Trends 2025. Source for: behind-the-meter generation share of AI campus proposals.

- United States Department of Energy, Liftoff: Advanced Nuclear and Industrial Decarbonization. Source for: federal sovereign-capital posture on domestic AI compute infrastructure.

Continue exploring the SAVRN doctrine

The AI data center grid interconnection wait is one face of the larger SAVRN doctrine on sovereign AI infrastructure. To go deeper into the components of the model: the sovereign AI infrastructure overview, the behind-the-meter AI power operator field guide, the AI data center supply chain brief, the construction cost playbook, the liquid cooling playbook, the tokens-per-watt-per-dollar efficiency metric, the 6-month deployment timeline brief, the modular AI campus framework, and the build-versus-buy decision framework. Each piece extends the central thesis: sovereign compute capacity is built by operators who own the stack, control the manufacturing, and pre-position the components. The doctrine is the playbook.