AI campus colocation is the deployment model that emerges when traditional colocation can no longer carry AI workloads. Rack-rental colo was designed for 5 to 10 kilowatt cabinets, grid-tied utility power, and air-cooled halls. The 2026 AI compute stack ships in 130 to 250 kilowatt liquid-cooled racks that the conventional colo floor cannot accept. The integrated model replaces that floor with one operator and one roof, where power, cooling, compute, and manufacturing sit together as a single system.

About SAVRN. SAVRN is the operator of an off-grid sovereign AI infrastructure campus model — owned power generation, owned compute, closed-loop liquid cooling — deployed in 6 to 12 months versus the 24-to-48-month industry standard, with active developments in California, Texas, Colorado, Nebraska, Panama, and Barbados.

This piece defines the category, walks the engineering that distinguishes it, and names the buyers who are migrating to it. It compares the integrated stack to traditional colo and to private cloud across the dimensions that matter at procurement. It also lays out the seven-criterion checklist a buyer should run before signing, and the four-layer architecture that makes the integrated stack possible at AI rack densities.

The takeaway up front. This category is not a smaller hyperscale data center, and it is not traditional colo with a liquid-cooling retrofit. It is an integrated systems architecture where on-site generation, closed-loop cooling, and factory-built compute pods all match AI density from day one. An enterprise team scaling beyond cloud, a sovereign buyer rejecting grid dependency, or a defense prime requiring isolation all reach the same conclusion: this is the only deployment path that keeps pace with how fast AI hardware now ships.

What AI campus colocation actually means

The term sounds like a marketing relabel, but in fact it describes a real category break. Traditional colocation rents floor space and rack power inside a multi-tenant data center. Specifically, the provider supplies the building, the cooling, and the utility connection. The tenant, in turn, brings the servers. By contrast, the integrated category collapses that boundary entirely. As a result, the operator owns the power generation, the cooling system, the building shell, the rack hardware, and frequently the integration manufacturing line that produces the rack itself.

AI campus colocation versus traditional rack rental

Traditional colo’s economics depend on aggregating diverse workloads behind one utility connection. The provider sells slack capacity. The integrated site, by contrast, targets a single workload class, with rack densities, power architecture, and cooling that the operator dimensions end-to-end for AI training and inference. As a result, the integrated site does not need to compromise. Each component matches the AI rack, not an averaged blend of legacy enterprise gear.

For the buyer, this changes the contract surface. A traditional colo agreement specifies kilowatts per cabinet, cooling capacity, and a service-level uptime target. An integrated agreement specifies tokens per dollar, deployment timeline, hardware refresh cadence, and on-site power generation reliability. Consequently, the negotiation moves from rented space to delivered compute economics, and the operator carries the integration risk that the tenant used to absorb in-house.

The integrated systems definition

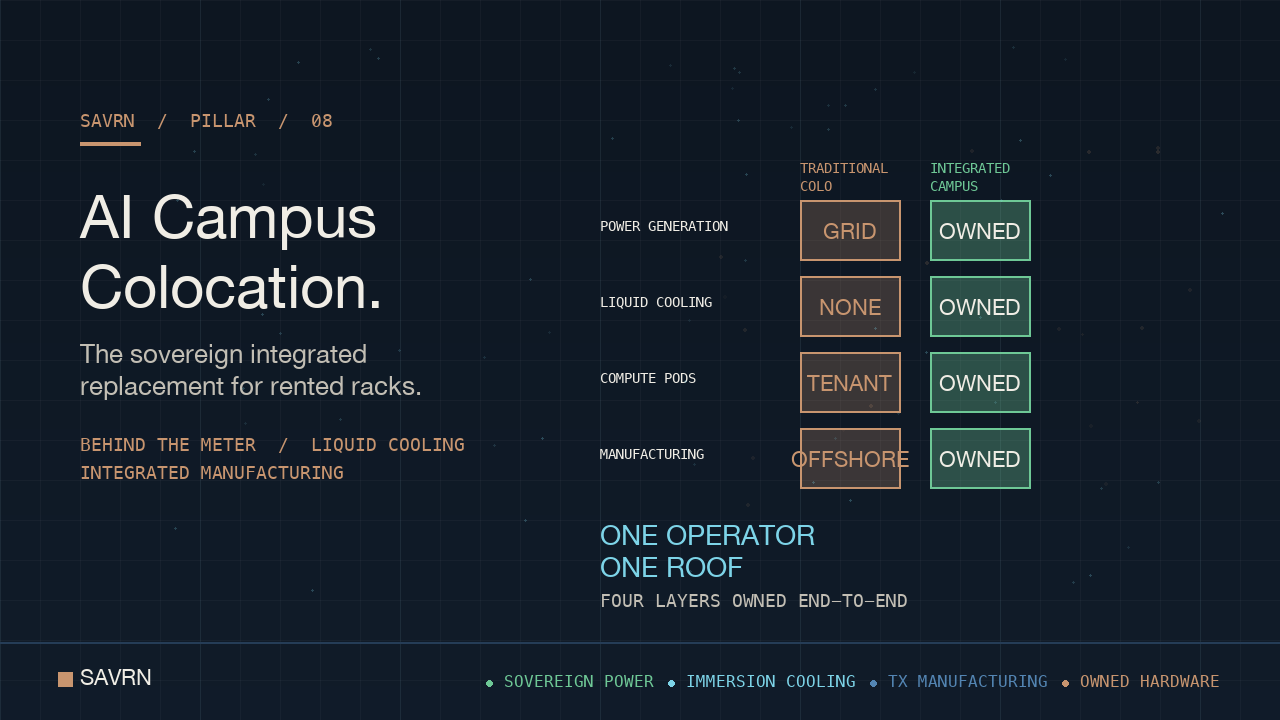

The integrated definition is what separates this category from a fashionable retrofit. Specifically, the site combines four layers into one operating system. First, power generation sits behind the meter. Second, liquid cooling reaches the pad before the racks arrive. Third, compute pods arrive factory-integrated. Finally, manufacturing of the integration step itself sits inside the operator’s footprint. Notably, the operator owns all four layers, and none piggybacks onto the slab after the fact.

This integration is what allows the site to ship in 6 to 12 months instead of the 24 to 48 months grid-tied stick-built campuses require. Each layer is sequenced concurrently rather than sequentially. In addition, the operator avoids the multi-vendor coordination tax that drags conventional builds into year three and frequently into year four.

Why the category was needed in 2026

Three structural shifts forced the category into existence. First, the U.S. interconnection backlog crossed 2,500 gigawatts of waiting capacity, with median wait times approaching five years per the Lawrence Berkeley National Laboratory queued capacity tracker. Second, AI rack densities passed the practical limit of air-cooled design between 2024 and 2026. Third, NVIDIA’s enterprise AI factory roadmap telegraphed continued density growth, meaning every retrofit attempt sets a new ceiling within twelve months.

Buyers who tried to absorb AI inside legacy colo halls in 2024 and 2025 hit each constraint in sequence. Therefore, the market began asking for a different building. The integrated category answered that ask by starting with the AI rack and designing the campus outward. By contrast, the colo retrofit started with the building and tried to wedge the rack inside it. One approach scales with the hardware roadmap. The other fights it.

Why traditional colocation cannot carry AI workloads

The case for the new category rests on a simple proposition. Specifically, the conventional colo floor was engineered for an era of compute density that ended somewhere around 2022. As a result, every assumption it carries about power per cabinet, airflow, and grid posture breaks at AI rack densities. Furthermore, refreshing the floor does not work in practice. Instead, the constraints compound across the stack.

The 5 to 10 kW rack ceiling

Most legacy colocation floors deliver between 5 and 10 kilowatts per cabinet. Notably, the Uptime Institute Global Data Center Survey still places the industry-average rack density below 12 kilowatts. AI training racks, by contrast, ship today at 130 kilowatts, with platforms NVIDIA has telegraphed pushing toward 235 to 600 kilowatts at the rack level. As a result, the gap between what the floor delivers and what the rack consumes is roughly twenty-fold.

That gap is not closeable through marginal upgrades. For example, a colo provider that doubles its rack power still sits at one-tenth the AI requirement. Consequently, the buyer either accepts under-provisioned racks running at fractional performance or, alternatively, migrates the workload to a site engineered for the actual density.

Air cooling fails above 30 kW per rack

Air cooling becomes economically punitive between 20 and 30 kilowatts per rack and physically impractical above that range. In particular, U.S. Department of Energy studies on data center cooling place the air-to-liquid crossover squarely inside that band. Above 30 kilowatts, however, the airflow required to remove heat from a single cabinet exceeds what a raised floor or hot-aisle containment can move without driving fan power past 30 percent of total facility load.

Single-phase immersion and direct-to-chip liquid cooling solve the problem, but neither retrofits cleanly into a building designed for air. Specifically, plumbing, structural floor loading, fluid management, and heat-rejection paths all have to be rebuilt. As a result, attempting the retrofit on an active colo floor often costs more than greenfield construction. By contrast, the integrated category skips that math by designing for liquid from day one.

The grid interconnection backlog

Power, however, is the harder constraint. Specifically, the five-year median grid wait LBNL documents is the reason behind-the-meter generation has moved from a niche choice to a procurement default for AI workloads. For example, of every interconnection request filed between 2000 and 2019, only 13 percent reached commercial operation by the end of 2024. Meanwhile, seventy-seven percent withdrew. Additionally, the remaining 10 percent are still queued.

Those numbers describe historical projects, not the current AI surge. In fact, today the backlog is heavier, the projects are larger, and the queue ranking favors generation over load. Therefore, an AI buyer who plans to wait for grid capacity is implicitly accepting a 2030 or 2031 first-token date. By contrast, behind-the-meter generation removes the queue from the critical path entirely.

Where AI campus colocation breaks the rack-density ceiling

The integrated site sidesteps each constraint by inverting the design sequence. The operator generates power on-site, plumbs liquid cooling first, lands liquid-cooled compute pods second, and treats the building shell as the last component, not the first. As a result, rack densities scale with the equipment NVIDIA ships rather than with the limits of a 2018-era hall. The architecture is forward-compatible by construction, not by retrofit.

The power architecture that defines AI campus colocation

Power architecture is the single decision that most distinguishes the integrated category from every adjacent option. The integrated site is built power-first. Generation, distribution, and load are co-located on the same parcel and operated by the same entity. This is the architectural choice that determines almost every downstream economic and operational property of the site, from time to first token through five-year cost-per-token.

Behind-the-meter generation as the foundation

Behind-the-meter generation routes around the interconnection queue entirely. The site is not waiting for a utility upgrade because it is not asking for one. As a result, the deployment timeline collapses to whatever the equipment lead time is, plus commissioning. For SAVRN’s SAVRN sovereign AI infrastructure stack, that window is 6 to 12 months.

Behind-the-meter sequencing also changes the unit economics. In particular, power becomes a controllable input cost rather than a regulated tariff. In addition, the operator captures the spread between fuel cost and grid retail rates, which in turn improves the cost-per-token math without exotic financial engineering.

Power-first sequencing inside AI campus colocation

Inside the integrated site, commissioning of the power layer happens before the racks land. Conventional builds run permitting, power, and equipment procurement as serial workstreams. The integrated build runs them in parallel, with the power layer leading. Consequently, the moment the first compute pod arrives on the pad, generation, distribution, and cooling already run live and conditioned for full load.

The economics follow from the sequencing. Specifically, a site that energizes power first can run commissioning loads, validate cooling, and complete acceptance testing concurrently with rack delivery. By contrast, a stick-built site that energizes power last spends six to nine months on site before any equipment can run. As a result, the integrated build saves roughly two quarters in calendar time.

Closed-loop circular economy benefits

The on-site generation footprint also unlocks the circular economy layer. Notably, waste heat from compute can be redirected into adjacent loads, including aquaculture, vertical farming, district heating, and bitcoin mining. In each case, the adjacent load converts what would otherwise be a thermal liability into a revenue line. As a result, the site captures value from energy that grid-tied colos simply reject to the atmosphere.

Closed-loop water further extends the model. SAVRN’s verified Texas water analysis documents how a properly designed integrated site eliminates the make-up water requirement entirely. The cooling fluid recirculates. Therefore, the campus footprint avoids the community water-rights conflicts that have stalled several IEA-tracked grid-tied builds across the U.S. southwest.

Cooling and density inside an AI campus colocation site

Cooling is the second architectural decision that separates the integrated category from every retrofit. The integrated site carries liquid plumbing before the slab cures. Every cabinet position, every rack pitch, and every distribution riser fits AI thermal loads, not the legacy enterprise blend that historic colos still serve.

Liquid cooling above 100 kW per rack

Above 100 kilowatts per rack, liquid is the only option. In short, the thermodynamics are not negotiable. Specifically, direct-to-chip cold plates handle GPU and accelerator silicon. Similarly, single-phase immersion handles the entire chassis. Together, both technologies move heat at densities that air cannot reach without absurd parasitic fan loads.

Liquid also reduces total facility power draw, because pumps move heat far more efficiently than fans. Consequently, the power usage effectiveness ratio drops from the colo industry average toward the rack-level efficiency that AI economics actually require.

Single-phase immersion at AI rack densities

Single-phase immersion submerges the chassis in a non-conductive fluid. Specifically, heat transfers from the silicon to the fluid, then from the fluid to a heat exchanger, and finally from the heat exchanger to a closed-loop dry cooler. As a result, the architecture supports densities well above 100 kilowatts per rack while running at near-ambient outdoor wet-bulb temperatures.

For the buyer, the operational implication is that hot-day derating effectively disappears. Air-cooled facilities lose capacity on the hottest summer afternoons. Immersion-cooled racks do not. As a result, training jobs running at peak demand do not pause during the worst grid stress windows.

How AI campus colocation absorbs next-generation rack density

Density growth is the silent variable that destroys retrofits. NVIDIA’s enterprise AI factory roadmap continues to push rack-level power, and the integrated footprint is the only deployment model that absorbs the increase without rebuilding the building. Liquid distribution, slab loading, and heat-rejection capacity were all sized for the upper bound from the start. Consequently, the next-generation pod drops into the same envelope without re-permitting, re-trenching, or re-pouring concrete.

This forward-compatibility is the structural reason buyers prefer integrated colocation for multi-year capacity plans. The retrofit colo will rebuild at the next density step. The integrated site will not. Over a five-year horizon, that distinction compounds into a meaningful capex and downtime delta that procurement teams notice.

SAVRN’s integrated sovereign model

The category description above is general. By contrast, SAVRN’s specific implementation adds three differentiators that turn a generic integrated site into a sovereign one. First, manufacturing sits inside the operator’s footprint. Second, the supply chain runs through Texas. Finally, the customer-facing surface is a physical destination buyers can walk through before signing.

The Intelliflex manufacturing layer

Intelliflex is the integrated manufacturing arm of SAVRN. Importantly, it is not a third-party vendor stitched into the supply chain. Specifically, Intelliflex builds the immersion-cooled rack systems, integrates the compute pods, and ships them to SAVRN campuses ready to energize. As a result, the operator controls the physical integration step that every other deployment model outsources to a contract manufacturer.

This vertical integration compresses the supply chain. As a result, lead times shrink because the rack does not wait in a queue at a contract manufacturer. Furthermore, quality control is enforced by the operator who will run the equipment in production. In addition, design changes flow back into manufacturing without renegotiating a vendor contract.

Domestic supply chain folded into AI campus colocation

Manufacturing in Fort Worth, Texas anchors the supply chain inside U.S. borders. Domestic manufacturing matters for two distinct reasons. First, it eliminates the cross-border lead time that has dominated AI hardware delivery since 2023. Second, it satisfies the procurement constraints that defense, regulated industry, and sovereign government buyers operate under, including software bill-of-materials and component-origin disclosures.

For the buyer, this means the operator can answer supply-chain provenance questions without subcontracts. Therefore, due diligence collapses into a single conversation rather than a multi-vendor audit.

The Fort Worth Customer Experience Center

The Intelliflex Customer Experience Center in Fort Worth is the physical destination where buyers can see the integrated stack running. Typically, most colocation procurement is done from a slide deck. By contrast, SAVRN’s model is built on letting the buyer touch the equipment, walk the manufacturing line, and see the immersion racks live before signing the contract.

For enterprise procurement teams accustomed to abstract reference architectures, this is unusual. For defense and sovereign buyers, it is decisive. Procurement officers prefer to verify before they trust, and the Customer Experience Center is engineered for verification.

Why integrated AI campus colocation needs domestic manufacturing

Domestic manufacturing is what closes the integration loop. Without it, the operator is still dependent on an offshore supplier whose lead time and quality posture sit outside the integrated control envelope. With it, however, the model is end-to-end. Specifically, from electrons leaving the on-site generator to tokens leaving the rack, every step is owned by one accountable operator. As a result, that accountability is exactly what defense, regulated, and sovereign buyers contract for.

Who buys AI campus colocation in 2026

Three buyer profiles dominate the 2026 pipeline. First, enterprise AI teams scaling beyond cloud hours form the largest segment by count. Second, sovereign and defense buyers form the highest-margin segment. Third, bitcoin miners pivoting to dual-revenue AI form the most operationally sophisticated segment, because they already understand integrated power and cooling at scale and operate to a similar uptime regime.

Enterprise AI teams scaling beyond cloud

The enterprise buyer arrives at the integrated category when cloud GPU bills cross a threshold that cannot be optimized away. Goldman Sachs Research models AI infrastructure capex doubling roughly every eighteen months through the back half of the decade. For an enterprise running sustained training or large-scale inference, the cloud-versus-owned crossover lands somewhere between 60 and 75 percent utilization, and once a workload sits above that line the owned model dominates on absolute dollars.

Above that utilization, owned infrastructure wins on cost-per-token. The enterprise still wants the operational simplicity of colocation. Therefore, the integrated category becomes the procurement answer. The buyer gets owned hardware economics with operator-managed power, cooling, and facilities, and the integration risk transfers from the buyer’s balance sheet to the operator’s.

Sovereign and defense buyers

Sovereign buyers and defense primes select the integrated category for reasons that are largely independent of cost. Specifically, the model offers physical isolation, no public cloud dependency, and a domestic supply chain. Together, these attributes satisfy mission requirements that no public cloud or shared colo can match. Ultimately, cost is a secondary consideration when the workload cannot leave the building.

Geographically, SAVRN’s published footprint spans California, Texas, Colorado, and Nebraska, with international expansion underway in Panama and Barbados. SAVRN picks each location for power generation potential, fiber access, and proximity to the buyer profile that location serves best. As a result, no two campuses share an identical buyer profile.

Bitcoin miners pivoting to dual-revenue AI campus colocation

The third buyer profile is the bitcoin mining operator pivoting toward AI compute. These operators already own integrated power and immersion cooling at scale. Consequently, the architectural distance from a mining campus to a sovereign integrated site is shorter than the distance from a traditional colo. The dual-revenue model lets the same site host AI workloads while ASIC mining runs as a baseload, smoothing utilization economics across the workload mix and hedging the AI demand curve.

How to evaluate an AI campus colocation partner

Procurement around the integrated category is structurally different from a traditional colo evaluation. Its contract surface is broader. Buyers are not renting space, they are contracting for delivered AI compute economics. Seven criteria separate a real integrated operator from a colo provider that has rebranded around the new vocabulary.

The seven-criterion checklist

Before signing, the buyer should verify the operator on seven dimensions. First, on-site power generation, with the fuel source and capacity disclosed. Second, liquid cooling installed before the racks land, with the heat-rejection path documented. Third, owned manufacturing or integration, with the facility location named. Fourth, deployment timeline backed by a phase-by-phase schedule. Fifth, rack-density forward compatibility through at least the next two NVIDIA platform generations. Sixth, domestic supply chain, with country of origin verified. Seventh, financial structure that aligns operator and buyer incentives over the multi-year horizon.

Notably, each criterion takes a yes-or-no answer. In practice, operators that hit yes on all seven are rare. Therefore, the checklist itself becomes a useful filter at the top of the funnel, and it surfaces the gap between marketing language and operational reality.

The deployment-speed test

Deployment speed is the most differentiating single criterion. SAVRN’s documented SAVRN AI infrastructure deployment timeline ranges from 6 to 12 months from contract to first token. The industry-standard hyperscale build runs 24 to 48 months. A retrofit colo with a liquid-cooling addition runs 18 to 30 months while the existing tenants are still in the building.

For the buyer, the difference is not academic. In particular, a 12-month delay on AI capacity is a model generation lost. By contrast, the operator that can ship 18 months earlier delivers the model generation that wins the market window. As a result, deployment speed effectively prices the option value of competitive timing.

Total cost of ownership versus the AI campus colocation alternative

Total cost of ownership reframes the procurement comparison. Cloud GPU hours look cheap until utilization passes the crossover threshold. Traditional colo looks cheap until rack density forces a relocation. The integrated agreement locks in the multi-year cost surface at signing, with power, cooling, and rack hardware all priced inside the operator’s stack and indexed to the operator’s input costs rather than to a regulated tariff.

For sustained AI workloads above the crossover threshold, the integrated model wins on absolute dollars and on cost-per-token. Notably, McKinsey’s data center capex forecasting places AI infrastructure spending growth in the trillion-dollar range through 2030. As a result, the buyer who locks integrated economics in 2026 captures a meaningful slice of that spend at fixed cost.

The future of AI campus colocation

The category will harden over the next three years. First, integrated operators with manufacturing footprints will pull share from retrofit colos. Second, the buyers who already migrated will refresh inside the integrated model rather than re-shopping. Finally, new geographies will open as power constraints in legacy markets become permanent rather than seasonal.

From rented racks to integrated systems

The largest secular shift is the migration from rented rack space toward integrated systems. Specifically, the rented rack was a software-era abstraction that worked when servers were commodities. By contrast, AI infrastructure is not commodity. Instead, the rack, the cooling, and the power are co-engineered. Consequently, the buying unit becomes the integrated pod, not the cabinet.

CARICOM and Latin American expansion

SAVRN’s expansion roadmap includes Panama and Barbados, with broader CARICOM and Latin American capacity in the planning horizon. These markets share a common attribute. Power constraints in U.S. legacy markets are pushing capacity south, and the integrated model is the only architecture that can establish capacity in regions where the local grid was never sized for AI loads. Behind-the-meter generation lets the campus exist where the grid does not yet reach.

Questions buyers should ask before signing

Before signing any integrated agreement, the buyer should ask three structural questions. Where is the power generated and who owns the generator? Who manufactures the rack and where is the manufacturing line? What is the contractually bound deployment timeline, and what penalties apply if it slips? The answers to those three questions reveal whether the operator is selling integrated systems or a colo retrofit with new vocabulary, and they almost always settle the procurement decision.

AI campus colocation as the dominant 2030 buying model

By the end of the decade, the integrated model will be the dominant buying pattern for sustained AI workloads. The retrofit colo will persist for legacy enterprise loads. The hyperscaler will persist for cloud-vendor compute. AI campus colocation will sit between them, sized for the buyer who needs owned-infrastructure economics with operator-managed facilities. The category exists because that buyer exists, and the buyer is not going away. The arithmetic of behind-the-meter power, liquid cooling, and integrated manufacturing only gets stronger as rack densities rise.

AI campus colocation FAQs

What is AI campus colocation?

Specifically, it is a deployment model where a single operator owns the on-site power generation, the liquid cooling, the compute hardware, and frequently the rack manufacturing line. As a result, it replaces the multi-tenant rack-rental model with an integrated site engineered end-to-end for AI training and inference workloads. Furthermore, the operator delivers compute economics rather than renting floor space, and the buyer signs for tokens-per-dollar rather than kilowatts-per-cabinet.

How does AI campus colocation differ from traditional colocation?

Traditional colocation rents kilowatts and rack space inside a multi-tenant building, with grid-tied utility power and air cooling. By contrast, the integrated category owns the power generation, plumbs liquid cooling before the racks land, and integrates compute pods at the operator’s manufacturing line. Consequently, the contract surface shifts from rented space to delivered tokens-per-dollar economics, with the operator carrying the integration risk that the tenant used to manage.

Why can traditional colocation not handle AI workloads?

Traditional colo floors deliver 5 to 10 kilowatts per cabinet with air cooling and grid-tied power. By contrast, AI training racks ship at 130 kilowatts and trend toward 235 to 600 kilowatts. As a result, the gap is roughly twentyfold and not closeable through marginal upgrades. Furthermore, air cooling fails above 30 kilowatts per rack, and the grid interconnection backlog blocks new utility capacity for five years on the median project.

How fast can an AI campus colocation site be deployed?

SAVRN’s documented timeline runs 6 to 12 months from contract to first token. This compresses the conventional 24 to 48 month hyperscale build by a factor of four to eight. The compression comes from behind-the-meter power, factory-integrated compute pods, parallel commissioning workstreams, and pre-engineered cooling distribution that lands before the racks arrive. Each compression source is structural, not optional.

Who buys AI campus colocation?

Three buyer profiles dominate. First, enterprise AI teams scaling beyond cloud hours form the largest segment by count. Second, sovereign and defense buyers form the highest-margin segment because of physical isolation requirements. Finally, bitcoin miners pivoting toward dual-revenue AI compute form the most operationally sophisticated segment, since they already understand integrated power and immersion cooling at scale.

What does behind-the-meter power mean for AI campus colocation?

Specifically, behind-the-meter power means the site generates electricity on-site rather than drawing from the utility grid. As a result, this routes around the five-year median grid interconnection wait, converts power from a regulated tariff into a controllable input cost, and lets the operator capture the spread between fuel cost and grid retail rates. Ultimately, behind-the-meter generation drives the architectural decision that enables the 6 to 12 month deployment timelines defining the integrated category.

Does AI campus colocation use water?

A properly designed integrated site uses closed-loop cooling that eliminates the make-up water requirement entirely. The cooling fluid recirculates between the immersion racks, heat exchangers, and dry coolers without atmospheric evaporation. SAVRN’s verified Texas water analysis documents the closed-loop architecture in detail and walks the bottoms-up math three different ways. This architecture also sidesteps the community water-rights conflicts that have stalled grid-tied builds in water-stressed regions across the U.S. southwest.

How does AI campus colocation handle next-generation rack densities?

The integrated site fits the upper bound of the rack-density roadmap from day one. Specifically, liquid distribution, slab loading, heat rejection capacity, and power feed pathways all carry the densities NVIDIA has telegraphed at the rack level. Consequently, next-generation pods drop into the existing envelope without rebuilding the building. By contrast, retrofit colos cannot match this forward compatibility, and they typically rebuild at the next density step.

Where are SAVRN’s AI campus colocation sites located?

SAVRN’s published footprint spans California, Texas, Colorado, and Nebraska, with international expansion underway in Panama and Barbados. SAVRN picks each location for power generation potential, fiber connectivity, land area, and proximity to the buyer profile the site serves best. Notably, the Intelliflex Customer Experience Center anchors domestic manufacturing in Fort Worth, Texas, where buyers can walk the integration line in person before signing.

How does AI campus colocation compare to private cloud?

Private cloud delivers software-defined infrastructure abstraction but remains grid-dependent and hardware-abstracted. The integrated category delivers full-stack ownership of generation, cooling, and compute, with the operator managing facilities. For sustained AI workloads where data sovereignty, hardware control, and multi-year cost certainty matter, the integrated model wins on every dimension except short-term elastic flexibility, which the buyer typically does not need at sustained-AI scale.

Continue exploring SAVRN coverage

Readers who want a deeper view of the deployment mechanics that compress the build window should see SAVRN’s SAVRN AI infrastructure deployment timeline walkthrough. The modular AI campus pillar compares modular and hyperscale architectures across the eight dimensions that matter at procurement. Anyone interested in the verified water analysis underpinning closed-loop cooling should read the 49 billion gallon mirage essay.

SAVRN’s SAVRN sovereign AI infrastructure overview anchors the integrated systems thesis and is the right entry point if you want the broader category framing. Landowners curious whether their property qualifies as a future site should review the land evaluation guide, which walks the seven criteria SAVRN applies during site triage. The operator’s view on the doctrine that ties power, compute, and integrated manufacturing together lives at about SAVRN. Ultimately, the doctrine is the product, and the integrated category is its physical expression.

Sources & Citations

Every quantitative claim in this piece traces to a named, verified primary source. URLs verified at time of publication. The full audit-grade citation record, with claim-by-claim source mapping and “cite this article” snippets, is maintained on the dedicated SAVRN sources page for this piece.

Primary research cited in this ai campus colocation brief

- Uptime Institute Global Data Center Survey 2024. Uptime Institute Global Data Center Survey 2024 — canonical industry baseline on operator practice, rack density, and PUE for the colocation comparison.

- McKinsey — Technology, Media & Telecommunications practice. McKinsey analysis of data center capex forecasting — used as the projection baseline for AI infrastructure capital deployment.

- Goldman Sachs Research. Goldman Sachs Research on AI-driven data center power demand growth.

Supporting frameworks, regulators, and industry data

- International Energy Agency. International Energy Agency tracking of grid-tied data center builds and global electricity demand from AI.

- LBNL — Queued Up interconnection queue tracker. LBNL queued capacity tracker — U.S. interconnection queue size and wait times that anchor the colocation deployment-speed comparison.

- U.S. Department of Energy. U.S. Department of Energy publications and program data on grid modernization, large-load policy, and data center electricity demand.