The AI data center supply chain now decides who deploys compute in 2026, who waits until 2028, and who walks away. SAVRN is the operator of an off-grid sovereign AI infrastructure campus model, with on-site power generation, closed-loop liquid cooling, and modular compute pods that ship in 6 to 12 months versus the 24-to-48-month industry standard. Power transformers averaged 128 weeks of lead time and generator step-ups stretched to 144 weeks in Wood Mackenzie’s Q2 2025 transformer survey. Cummins is sold out of high-horsepower gensets through 2028, per the company’s February 2026 capacity announcement. Those two numbers, sitting next to a five-year LBNL grid interconnection queue, define every megawatt scheduled to come online this decade.

Hardware is the new bottleneck. GPUs get the headlines, yet the components stranding billion-dollar campuses are pad-mount transformers, medium-voltage switchgear, gas-fired prime-power gensets, and lithium iron phosphate battery cabinets. McKinsey forecasts a $5.2 trillion capital outlay for AI data centers by 2030, with about $1.6 trillion of that spending landing in the data center infrastructure layer where the supply crunch lives. Meanwhile, the International Energy Agency projects global data center electricity demand to reach roughly 945 terawatt hours by 2030, doubling the 2024 baseline. The buyers chasing that capacity already outnumber the factories that can build it.

The AI Data Center Supply Chain Crisis in 2026

The crisis is structural, not cyclical. Therefore, ride-it-out procurement plans fail by design. Demand for AI compute hit hyperscale growth rates while the upstream factories continued to run on a 1990s replacement-cycle cadence. Consequently, the system snapped under load.

Furthermore, the constraint is not one component. It is the interaction of seven simultaneous constraints, each on its own lead-time curve. Operators who model only the GPU line lose. Operators who model every line wait, sequence, and survive.

What the AI data center supply chain actually includes

The AI data center supply chain is the network of factories, foundries, and contract assemblers that produce the goods needed to energize a megawatt of compute. It spans seven layers: GPUs, server chassis, switchgear, transformers, generators, battery energy storage systems, and interconnection equipment. In addition, the chain includes the trained labor required to install, commission, and operate the gear.

Each layer feeds the next. As a result, a 24-month switchgear queue can strand an otherwise complete campus. Likewise, a fully built campus can sit idle for years waiting on the utility transformer that ties it to the grid. By contrast, sovereign campus models compress those dependencies onto a single owner’s balance sheet.

Why 2026 is the inflection year for AI infrastructure procurement

Three forces converged on the calendar this year. First, the IEA documented data center demand growing 12 percent annually for five straight years, with the load doubling by 2030. Second, NVIDIA locked in $95.2 billion of supply commitments through calendar 2027, removing slack from the foundry layer. Third, transformer makers entered 2026 with order books filled into 2028 and 2029, per the National Electrical Manufacturers Association.

Consequently, every operator booking a new project in 2026 is competing for a fixed pool of components. The pool will not grow at the pace demand requires. Therefore, who sequences first wins.

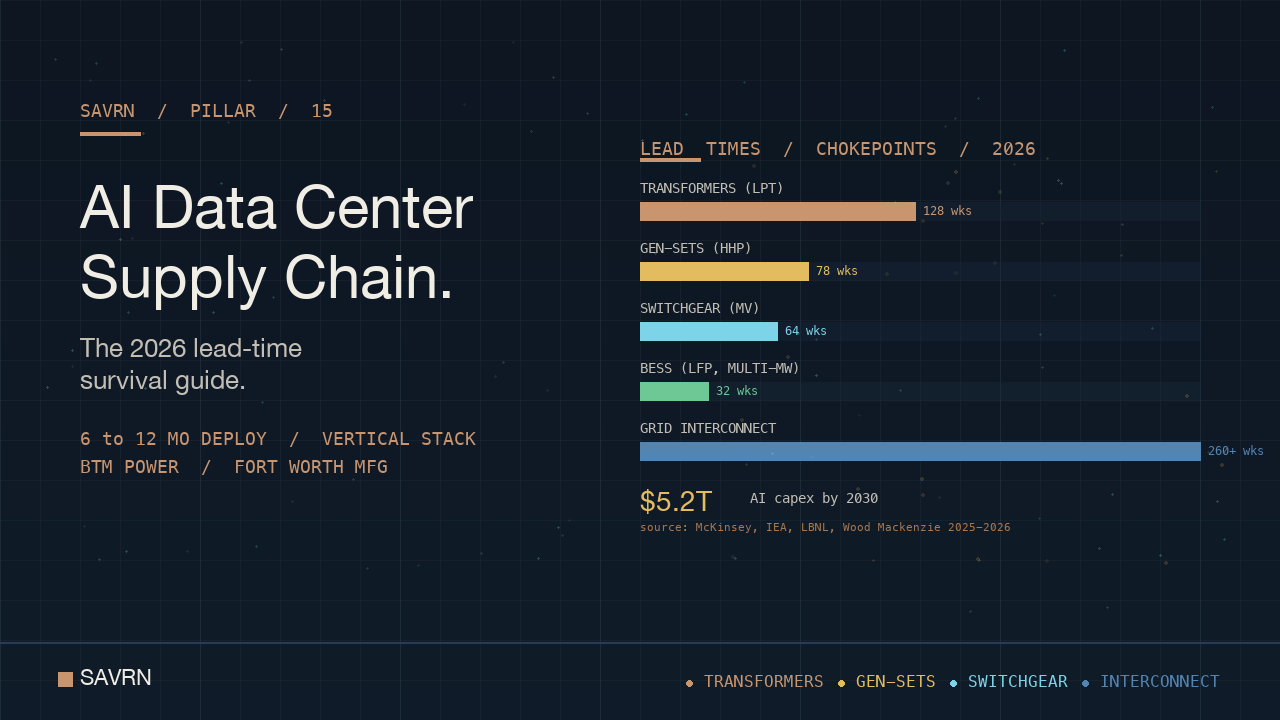

The five chokepoints that gate every megawatt

Five chokepoints decide whether a project lands. They are: large power transformers, prime-power gensets, medium-voltage switchgear, lithium iron phosphate battery systems, and the utility interconnection itself. Notably, GPUs sit downstream of all five. A campus without energization can hold its GPU allocation for only so long before the allocation gets reassigned.

Transformer Lead Times Rewrite Every AI Data Center Supply Chain

Transformers are the most under-discussed bottleneck in the AI data center supply chain. They convert utility voltage to the medium and low voltages that data center equipment requires. Without them, no electrons flow. Moreover, the United States manufactures only a fraction of the large units it consumes.

Five years ago, a transformer ordered today shipped in four to six weeks, according to National Electrical Manufacturers Association statements to Utility Dive. The same order placed in 2026 ships in 80 to 210 weeks. As a result, every utility interconnection queue and every behind-the-meter project on the continent now revolves around a single shortage.

From 4 weeks to 128 weeks: a five-year transformer collapse

The cleanest data set is the Wood Mackenzie 2025 transformer market survey. Power transformer lead times averaged 128 weeks in their Q2 2025 update, with generator step-up units at 144 weeks. By contrast, the 2019 baseline was 30 weeks. The slide was not gradual. It accelerated sharply in 2022 and again in 2024.

In addition, NEMA Director of Government Relations Peter Ferrell stated that delivery of a transformer ordered today could take up to three years. That public number sets the planning horizon. Furthermore, specialized orders in the 765 kV class now exceed four years, per the May 2026 PV Magazine USA market analysis.

Pad-mount transformer scarcity at the AI data center supply chain edge

The pad-mount three-phase transformer is the workhorse at the campus boundary. Each megawatt of IT load typically requires two to four pad-mount units. Wood Mackenzie’s 2026 outlook flagged a supply deficit on this class driven by AI data centers, manufacturing reshoring, and electric vehicle charging build-out.

Consequently, pad-mount lead times have tripled in five years. Moreover, the deficit math matters because pad-mounts cannot be substituted with larger units. They sit inside specific size envelopes the rest of the design depends on.

Why Wood Mackenzie’s deficit math matters for sovereign compute

Wood Mackenzie projected a 30 percent supply deficit on large power transformers and a 10 percent deficit on distribution transformers heading into 2025. Both deficits widen through 2027 in their model. Therefore, any AI campus depending on utility-supplied transformation is competing not just with other data centers, but with every utility upgrade in the country.

By contrast, the SAVRN sovereign AI infrastructure model owns its transformation. SAVRN procures and pre-positions long-lead electrical equipment on the operator’s balance sheet rather than the utility’s queue. In short, sovereignty is procurement strategy, not just policy.

Gen-Sets and the New Behind-the-Meter AI Data Center Supply Chain

Behind-the-meter generation is the fastest path to compute, but the gensets that make it possible are themselves rationed. Cummins, Caterpillar, and Rolls-Royce dominate the high-horsepower category data centers require. In 2026, all three are oversubscribed. Consequently, the gen-set layer of the AI data center supply chain now operates like a foundry, not a catalog.

Cummins is sold out through 2028

Cummins announced a $150 million expansion of its Fridley, Minnesota high-horsepower facility in February 2026 to increase QSK95 output by 30 percent. The expansion exists because lead times on the QSK95 platform hit 18 months and the order book filled into 2028. In short, even with the expansion, Cummins cannot quote a new prime-power slot inside the planning horizon of most 2026 projects.

Caterpillar’s $63 billion backlog

Caterpillar reported a $63 billion order backlog in Q1 2026, a figure that includes its energy and transportation segment where data center gensets sit. Industry-wide lead times for major OEM gensets stretch to 107 weeks, per the Power Magazine 2026 generator market report. As a result, the buyer who locks slots in 2026 receives equipment in 2028.

Natural gas turbines and the prime-power pivot

Reciprocating gensets are not the only behind-the-meter path. Mid-sized gas turbines in the 30 to 70 megawatt range now ship into AI campuses for prime-power duty rather than emergency standby. However, the lead time for new aeroderivative turbines stretches into 2028 as well. Moreover, GE Vernova and Siemens Energy have both signaled selective order acceptance through 2027.

Consequently, the operators who win prime-power generation are those who reserved capacity in 2024 or earlier. By contrast, those entering the queue today plan for 2027 first-fire dates at minimum. The SAVRN behind-the-meter AI power doctrine treats generation as a procurement asset, not a utility request.

Switchgear, BESS, and the Hidden AI Data Center Supply Chain Chokepoints

Switchgear is the least glamorous and most frequently misforecast line item in the AI data center supply chain. It controls electron flow through the campus and protects every other asset. As a result, switchgear failure stops everything. Therefore, switchgear delivery sets the energization date for the campus.

80-week switchgear queues

Medium-voltage switchgear lead times now run 26 to 32 weeks for standard configurations and 50 to 80 weeks for custom AI-campus configurations. By contrast, pre-pandemic lead times were 12 to 16 weeks. In addition, high-voltage gear has stretched to 36 to 48 months in some categories, according to data center capital equipment analyses published in early 2026.

Eaton’s Q1 2026 earnings disclosed total backlog above $19 billion, with the Electrical Americas backlog growing to roughly $10 billion and data center orders up 240 percent year-over-year. Furthermore, Eaton committed $1.5 billion of incremental capacity investment, with most new lines online no earlier than late 2026.

BESS supply moves from steady to constrained

Lithium iron phosphate batteries dominate data center BESS, accounting for roughly 90 percent of new deployments. Installed costs have dropped to $380 to $520 per kilowatt-hour in 2026 from $550 to $700 in 2022. However, the lead time direction has reversed. Furthermore, multi-megawatt BESS orders with integrated PCS and switchgear now carry 20 to 35 week lead times because the upstream transformer and semiconductor constraints flow through.

Why a $40M switchgear order can strand a $2B campus

Switchgear, transformers, and BESS together represent under 10 percent of total campus construction spend. However, without them the other 90 percent cannot energize. Consequently, a $2 billion AI campus can sit idle waiting on a $40 million switchgear lineup. This asymmetry is the defining feature of the 2026 AI data center supply chain.

In short, the cheapest line item carries the highest schedule risk. Therefore, the operators who invest in pre-positioning and vertical integration capture an oversized share of deployed capacity.

GPUs Are the Visible Tip of the AI Data Center Supply Chain

GPUs occupy more headlines than any other component, yet they sit downstream of every other constraint. The AI data center supply chain delivers GPUs to operators who can already power and cool them. Consequently, an operator who locks GPU allocation but loses the energization race forfeits both.

NVIDIA Blackwell allocation through mid-2026

NVIDIA reported $95.2 billion of supply-related purchase commitments through fiscal 2027 in its Q3 fiscal 2026 earnings release, almost double the prior quarter’s $50.3 billion figure. Blackwell-generation platforms are effectively allocated through mid-2026. Moreover, NVIDIA secured roughly 70 percent of TSMC’s CoWoS-L packaging capacity for 2026 and 2027 production, per SemiAnalysis market briefings.

As a result, the GPU layer of the AI data center supply chain is rationed at the manufacturer level. Allocation decisions are negotiated, not transacted. In short, the operators who secured 2026 and 2027 commitments did so through multi-quarter pre-buy relationships, not catalog orders.

CoWoS-L packaging and the HBM3e ceiling

The deeper bottleneck below GPUs is TSMC’s chip-on-wafer-on-substrate advanced packaging line, designated CoWoS-L for the largest accelerator dies. Micron, SK Hynix, and Samsung supply the high-bandwidth memory stacks that ride on the package. Furthermore, HBM3e capacity remains tight through 2026 and HBM4 ramps in 2027.

Consequently, the upstream silicon supply chain is the gating layer behind the GPU layer. An operator securing GPU allocation is in effect securing CoWoS packaging slots and HBM memory stacks bundled with the die.

Why GPU lead time is the easiest constraint, not the hardest

Counterintuitively, GPUs are the most negotiable component in the 2026 AI data center supply chain. Allocation can be moved between projects within an operator’s footprint. By contrast, a transformer or genset positioned at site A cannot easily redeploy to site B without re-permitting and reshipping. As a result, the operators winning compute capacity treat GPUs as the last lock-in, not the first.

Grid Interconnection: The AI Data Center Supply Chain’s Hardest Wall

The hardest constraint in the AI data center supply chain is not a manufactured component at all. It is the utility interconnection itself. Lawrence Berkeley National Laboratory’s Queued Up 2025 Edition documented 2,060 gigawatts of generation and storage actively seeking grid interconnection across the United States at the end of 2024.

2,060 GW stuck in LBNL’s queue

The Berkeley Lab queue snapshot breaks out 1,400 GW of generation capacity and 890 GW of storage in interconnection studies. Roughly 49 percent of the queued capacity carries a proposed commercial operations date of end-2026 or earlier, yet historic completion rates run far below that. Furthermore, the typical project completed in 2022 spent five years in queue, up from three years in 2015 and under two years in 2008.

Five-year average wait, and the geographic spread

Wait times vary by region. ERCOT moves projects faster than the eastern ISOs because Texas operates as an islanded grid with its own queue. By contrast, PJM, MISO, and SPP carry the longest queues. Consequently, the geography of the AI data center supply chain has been reshaped by where interconnection is reachable inside a planning horizon shorter than the GPU obsolescence cycle.

FERC Order 2023 and the partial unlock

FERC Order 2023, issued in 2023 and now under implementation across RTOs, replaces the first-come-first-served queue with cluster studies and stiffer financial commitments. The reform reduces speculative applications but does not produce new transformers or transmission lines. Therefore, FERC Order 2023 narrows the queue without lengthening the supply pipeline that feeds it.

As a result, the cleanest path through the interconnection wall is to bypass it. SAVRN doctrine treats interconnection as a strategic option rather than a dependency. Furthermore, off-grid sovereign campuses neither wait in the LBNL queue nor compete for utility transformers.

The grid interconnection wall is the single fact that reorders every other line item. A campus that cannot energize within 30 months of groundbreaking forfeits its GPU allocation. Therefore, operators reading the LBNL queue map plan around it rather than through it. The geographies that remain procurable inside that window are narrow. SAVRN focuses development in California, Texas, Colorado, Nebraska, Panama, and Barbados precisely because each jurisdiction supports a behind-the-meter generation footprint without depending on multi-year transmission upgrades.

How SAVRN Compresses the AI Data Center Supply Chain to 6-12 Months

SAVRN compresses the AI data center supply chain into a single integrated procurement sequence. Power, compute, cooling, and structural envelope are all controlled by one operator with one balance sheet. Consequently, the project plan looks nothing like a hyperscale build. It looks like a sovereign manufacturing campaign.

Vertical integration through Intelliflex

Intelliflex is integral to SAVRN, not a third-party vendor. Intelliflex manufactures modular compute pods, cooling skids, and structural envelopes at its Fort Worth, Texas facility. Therefore, the long-lead enclosure and rack components ship from a manufacturing footprint SAVRN controls. In short, Intelliflex turns 18-month delivery curves into scheduled production runs.

Behind-the-meter generation eliminates the queue

Owning on-site power generation eliminates the utility interconnection dependency. SAVRN’s campus model deploys natural gas turbines and reciprocating engine sets sized to base load the entire IT envelope. Consequently, the LBNL queue does not gate the deployment timeline. Moreover, on-site generation gives the operator a procurement lever inside the gas market and the power market simultaneously.

Modular pods front-load the long-lead components

Modular construction front-loads long-lead components into the factory schedule rather than the construction schedule. As a result, the transformers, switchgear, and BESS that would otherwise gate field assembly arrive at Fort Worth already integrated into compute pods. Furthermore, the field crew at the campus site installs pre-tested assemblies rather than commissioning loose equipment.

The Fort Worth manufacturing footprint

The Intelliflex Customer Experience Center in Fort Worth anchors the manufacturing layer. Customers can inspect, test, and commission pods inside the factory before they ship. Therefore, the field commissioning phase compresses from quarters to weeks. In short, the manufacturing-first sequence is the architectural decision that allows SAVRN to deploy in 6 to 12 months while industry-standard hyperscale builds take 24 to 48 months.

Procurement Playbook for the 2026 AI Data Center Supply Chain

A 2026 procurement plan that does not account for the AI data center supply chain crisis will slip. Therefore, the operator playbook needs three changes from 2022 practice. First, reserve long-lead components 18 to 24 months ahead of need. Second, pre-position capital rather than transact at the spot market. Third, track operator KPIs that surface schedule risk before it lands.

The 18-month minimum hardware reservation schedule

For any project targeting first-token operation in 2027 or later, hardware reservations should be in place by Q3 2026. Transformer slots require the longest lead. Furthermore, BESS, switchgear, and gen-set slots compete for the same procurement window. Consequently, the operator reservation calendar drives the project’s first-token date more than the construction schedule.

Capital pre-positioning vs spot procurement

Spot procurement is dead in 2026. Manufacturers no longer quote retail prices on spot inventory because there is no spot inventory. By contrast, pre-positioned capital deposited against future production runs receives priority allocation. As a result, capital structure becomes a procurement weapon. Moreover, operators with treasury reserves to deposit win the AI data center supply chain in 2026 and 2027.

Operator KPIs to track quarterly

Three KPIs surface AI data center supply chain risk before it lands. First, the percent of project bill-of-materials with confirmed delivery dates. Second, the gap between confirmed delivery dates and the project first-token date. Third, the gen-set, transformer, and switchgear reservation pipeline against 24-month projected demand. Consequently, operators who report these three metrics quarterly outperform peers who report only spend and headcount.

Furthermore, public sovereign-AI procurement should add the same metrics to its reporting frameworks. The SAVRN sovereign AI infrastructure doctrine treats the AI data center supply chain as a public-interest constraint, not a private vendor concern. As a result, the procurement playbook is also a national competitiveness playbook. Compute capacity that lands inside the United States in 2027 and 2028 will be controlled by operators who treated 2026 as the year to act on supply chain risk rather than the year to discover it.

FAQs

What is the AI data center supply chain?

The AI data center supply chain is the network of factories, foundries, and contract assemblers that produce every component an AI campus needs to operate. It spans GPUs, server chassis, switchgear, transformers, prime-power gensets, lithium iron phosphate battery energy storage systems, and interconnection equipment. The chain also includes the trained labor required to install and commission the gear. In 2026, every layer of this chain is supply-constrained.

How long is the transformer lead time for AI data center supply chain projects in 2026?

Large power transformer lead times averaged 128 weeks in Wood Mackenzie’s Q2 2025 survey, with generator step-up units at 144 weeks. NEMA Director of Government Relations Peter Ferrell stated that orders placed today can take up to three years to deliver. Specialized 765 kV class units sometimes stretch to four years. Five years earlier the same orders shipped in four to six weeks, marking a roughly 20-fold lead-time expansion.

Why are gensets sold out through 2028?

Cummins, Caterpillar, and Rolls-Royce all entered 2026 with order books filled into 2028. Cummins announced a $150 million Fridley facility expansion to lift QSK95 high-horsepower output by 30 percent. Caterpillar reported a $63 billion Q1 2026 backlog including data center gensets. Demand from AI campuses pivoting to behind-the-meter prime power amplified existing emergency-standby demand, and the OEMs cannot ramp manufacturing fast enough to absorb the surge.

Is the GPU shortage the worst constraint in the AI data center supply chain?

No. GPUs draw the most headlines but sit downstream of every other component. NVIDIA Blackwell allocation is constrained, yet TSMC and the HBM suppliers are scaling capacity through 2027. By contrast, transformer and genset capacity scales slowly because the manufacturing footprint is decades old. As a result, the harder constraints are upstream of the GPU: transformers, gensets, switchgear, and grid interconnection. Operators winning capacity treat GPUs as the last lock-in, not the first.

How does SAVRN bypass the AI data center supply chain bottlenecks?

SAVRN compresses the AI data center supply chain into a single integrated procurement sequence. Power, compute, and cooling are owned by one operator. Intelliflex manufactures modular pods at Fort Worth so long-lead enclosure and rack components ship on a scheduled production run rather than a customer-facing lead time. On-site generation eliminates the LBNL grid interconnection queue. Consequently, SAVRN deploys in 6 to 12 months versus the 24-to-48-month industry standard.

What is the grid interconnection queue and why does it matter?

The grid interconnection queue is the FERC-regulated process by which new generation or load connects to the transmission system. Lawrence Berkeley National Laboratory’s Queued Up 2025 Edition counted 2,060 gigawatts of generation and storage in active interconnection studies. The typical project completed in 2022 waited five years in queue, up from under two years in 2008. For AI data centers, that wait collides with a 24-month GPU obsolescence cycle, making queue-dependent projects unviable.

How big is the AI data center capital outlay?

McKinsey forecasts global AI data center capital expenditure of $5.2 trillion by 2030, with about $3.3 trillion landing in IT equipment, $1.6 trillion in data center infrastructure, and $300 billion in power generation. An accelerated demand scenario raises the total to $7.9 trillion. The infrastructure layer is where the AI data center supply chain crisis lives because the components in that layer cannot be sourced quickly even with capital available.

How much electricity will AI data centers consume by 2030?

The International Energy Agency projects global data center electricity consumption of approximately 945 terawatt hours by 2030, doubling the 2024 baseline of 415 TWh. AI workloads drive most of the increase. The United States accounts for roughly 240 TWh of that growth. RAND Corporation projects AI data centers in the United States could draw 68 GW of capacity by 2027, comparable to the total installed capacity of California.

Can the CHIPS Act and the IRA solve the AI data center supply chain shortage?

Partially. The CHIPS Act authorizes roughly $280 billion in semiconductor manufacturing support and the Inflation Reduction Act adds $369 billion of clean-energy incentives, including the 45X production tax credit relevant to battery and inverter manufacturing. New domestic factories take three to five years to come online. Therefore, neither act materially eases 2026 or 2027 lead times. Both will reshape the 2028 and 2029 supply curves if implementation continues on pace.

What KPIs should operators track on the AI data center supply chain?

Three KPIs surface schedule risk before it lands. First, the percent of project bill-of-materials with confirmed delivery dates. Second, the gap between confirmed delivery dates and the project’s first-token date. Third, the gen-set, transformer, and switchgear reservation pipeline measured against 24-month projected demand. Operators who report these metrics quarterly outperform peers who report only spend and headcount, because the schedule risk is hidden in component delivery dates, not aggregate capex.

Why does the Intelliflex Fort Worth facility matter for the AI data center supply chain?

Intelliflex is the manufacturing layer integral to SAVRN’s sovereign campus model. The Fort Worth facility produces modular compute pods, cooling skids, and structural envelopes that ship pre-integrated to SAVRN sites. As a result, long-lead components are sequenced inside a factory production run rather than a customer-facing lead-time queue. The Intelliflex Customer Experience Center allows customers to inspect, test, and commission pods before they leave the factory, compressing field commissioning from quarters to weeks.

Sources & Citations

Every quantitative claim in this piece traces to a named, verified primary source. URLs verified at time of publication. The full audit-grade citation record, with claim-by-claim source mapping and cite-this-article snippets, is maintained on the dedicated SAVRN sources page for this piece.

Primary research and forecasts cited in this AI data center supply chain brief

- Wood Mackenzie, Power transformers and distribution transformers will face supply deficits of 30% and 10% in 2025. Source for: transformer supply deficits and Q2 2025 lead-time data.

- Lawrence Berkeley National Laboratory, Queued Up: 2025 Edition, Characteristics of Power Plants Seeking Transmission Interconnection. Source for: 2,060 GW of generation and storage in interconnection queues, five-year wait times.

- International Energy Agency, Energy and AI – Energy demand from AI. Source for: 945 TWh global data center demand by 2030, doubling from 2024.

- McKinsey & Company, The cost of compute: a $7 trillion race to scale data centers. Source for: $5.2 trillion AI capex forecast by 2030, infrastructure layer breakdown.

- RAND Corporation, AI’s Power Requirements Under Exponential Growth. Source for: 68 GW projected AI data center capacity by 2027 in the United States.

Operator and manufacturer disclosures cited in this AI data center supply chain brief

- Eaton Corporation, Eaton Reports Record First Quarter 2026 Results. Source for: $19 billion total backlog, Electrical Americas backlog growth, 240 percent data center order increase.

- NVIDIA Corporation, NVIDIA Financial Results for Third Quarter Fiscal 2026. Source for: $95.2 billion of supply-related purchase commitments through fiscal 2027.

- National Electrical Manufacturers Association, statements to Utility Dive on transformer supply. Source for: Director of Government Relations Peter Ferrell quote on three-year delivery times.

View the full audit record ‚Üí

Continue Exploring SAVRN Doctrine

- Behind the Meter AI Power: The 2026 Operator Field Guide – how owning generation neutralizes the interconnection queue.

- AI Infrastructure Deployment Timeline – the 6-month phased schedule SAVRN ships against.

- Liquid Cooling for AI: 2026 Operator’s Density Playbook – the rack-density constraint that drives every cooling skid order.

- Build vs Buy AI Infrastructure – when vertical integration beats colocation procurement.

- Tokens Per Watt Per Dollar – the unit-economics frame that absorbs supply chain risk into operating returns.